Surprised by a Lump-Sum Social Security Check? Here’s How the Tax Rules Really Work

Receiving a lump-sum Social Security payment often brings relief, especially after months or years of waiting for approval. But that relief is frequently followed by confusion—and sometimes fear—once clients realize taxes may apply.

For the 2026 filing season, the tax rules for lump-sum Social Security benefits remain largely unchanged. However, clearer IRS reporting guidance and ongoing income pressures make understanding these rules more important than ever. With the right approach, a lump-sum payment does not have to result in a tax shock.

What Are Lump-Sum Social Security Benefits?

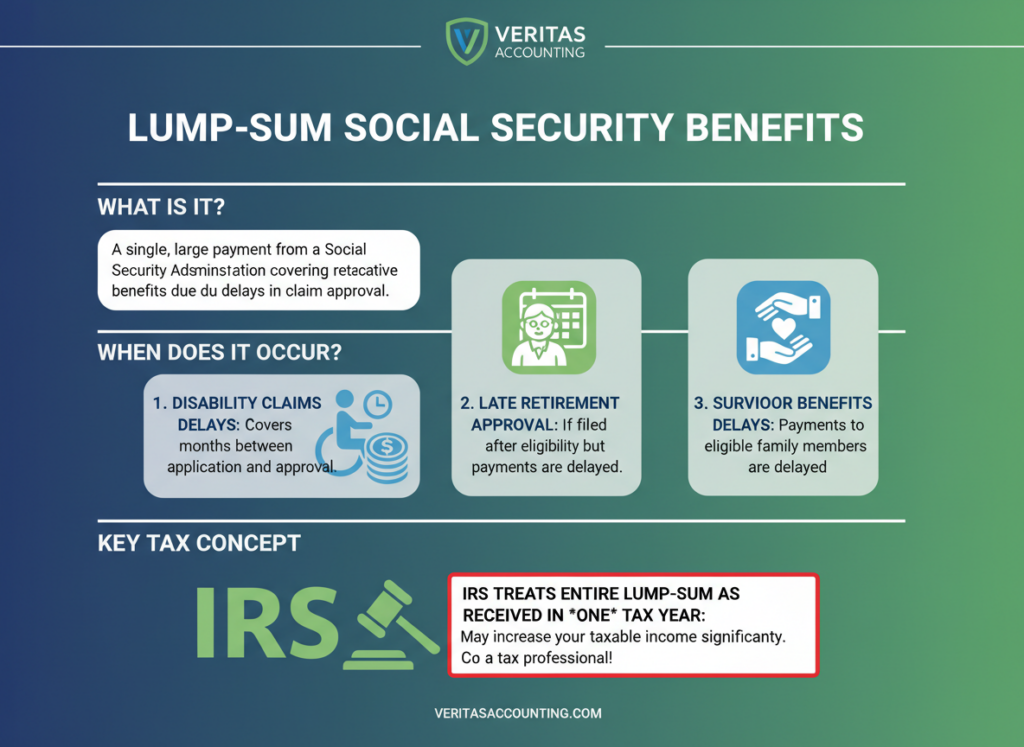

Lump-sum Social Security benefits occur when the Social Security Administration approves benefits retroactively and pays multiple months or years of missed benefits in a single check.

This most often happens with:

- Disability claims delayed by appeals

- Retirement benefits approved late

- Survivor benefits processed after administrative delays

Although the payment covers prior periods, the IRS treats the entire amount as received in one tax year, which is where most confusion begins.

How Lump-Sum Social Security Benefits Are Taxed

The IRS requires taxpayers to report all Social Security benefits in the year they are received, even when those benefits relate to earlier years. This includes lump-sum Social Security benefits paid retroactively.

However, taxpayers are not required to amend prior-year tax returns. Instead, the tax law provides a special calculation designed to prevent unfair tax spikes.

This distinction is critical. Reporting does not automatically mean the entire payment is taxed at once.

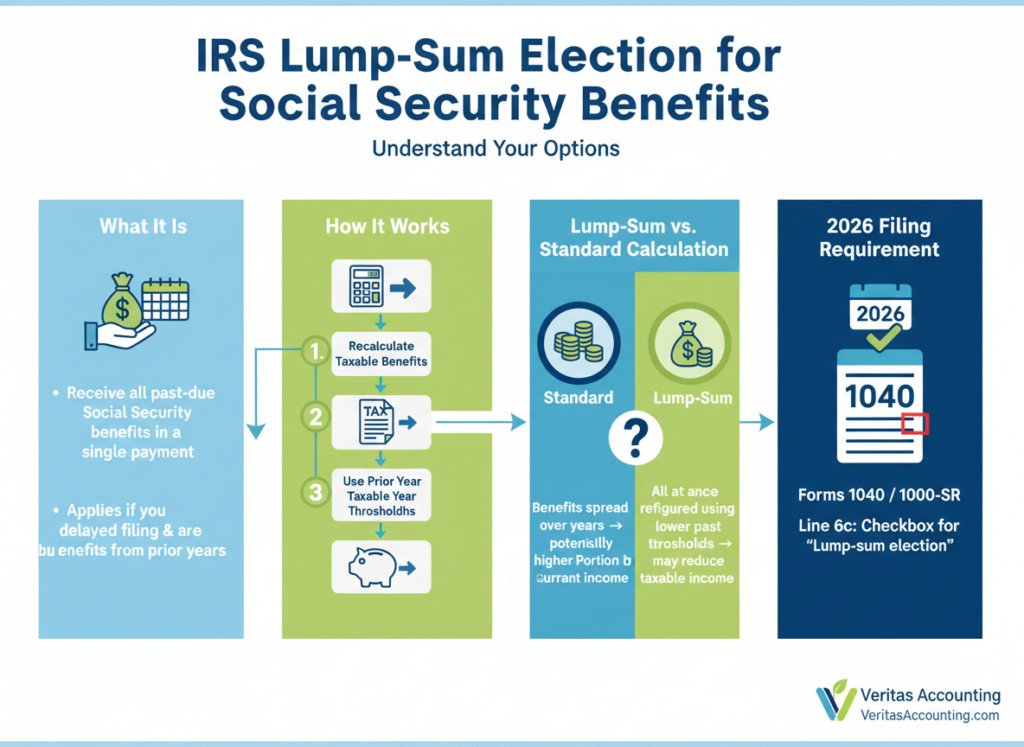

Using the Lump-Sum Election for Social Security Benefits

To address retroactive payments, the IRS allows a special calculation known as the lump-sum election for Social Security benefits.

This method allows taxpayers to:

- Recalculate how much of the benefits would have been taxable in the prior year(s)

- Use the income thresholds that applied in those years

- Carry forward only the taxable portion into the current return

If this method produces a lower taxable amount, the taxpayer may use it. If it does not, the standard calculation applies instead.

For 2026 filings, Forms 1040 and 1040-SR now include a checkbox on Line 6c to indicate that the lump-sum election was used. While no separate form is required, this checkbox helps document the calculation and improves return clarity.

Why Lump-Sum Social Security Benefits Trigger Tax Confusion

Many clients believe Social Security taxation thresholds increase with inflation. They do not.

The thresholds remain frozen at:

- $25,000 and $34,000 for single filers

- $32,000 and $44,000 for married filing jointly

Once combined income exceeds these levels, up to 50% and eventually 85% of Social Security benefits may be taxable. A lump-sum Social Security payment can temporarily push income above these limits, making careful calculation essential.

Multiple Years, Multiple Lump-Sum Calculations

When lump-sum Social Security benefits cover more than one prior year, the special calculation may be applied separately to each year included in the payment.

This is common in disability cases that span multiple years. Accurate prior-year income records and careful review of Form SSA-1099 are critical to applying the rules correctly.

Tax professionals should confirm:

- Which years are included

- Filing status for each year

- Income levels that affect benefit taxation

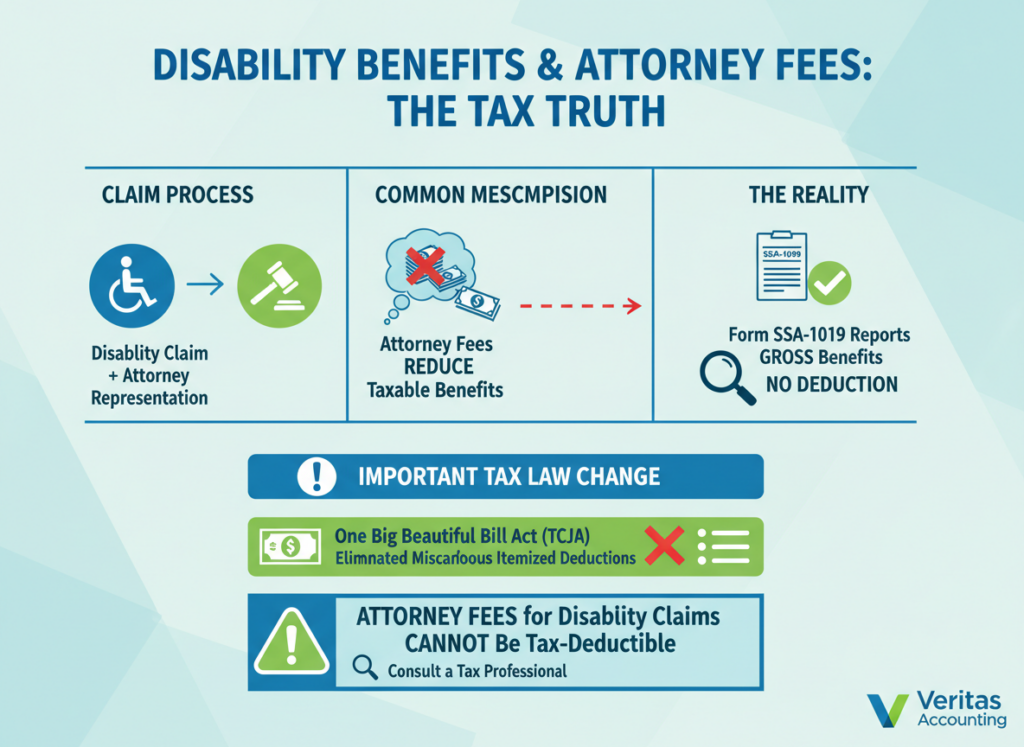

Special Issues With Disability Lump-Sum Social Security Benefits

Disability claims often involve attorney representation. Clients frequently assume attorney fees reduce taxable Social Security benefits. They do not.

Social Security reports gross benefits before attorney fees on Form SSA-1099. Under the One Big Beautiful Bill Act (OBBBA), miscellaneous itemized deductions are permanently suspended, meaning attorney fees no longer reduce taxable income.

Clients should be prepared for this outcome to avoid unpleasant surprises.

What Tax Professionals Should Explain About Lump-Sum Social Security Benefits

Reassurance is essential. A lump-sum Social Security payment does not automatically mean higher taxes.

Clients should understand:

- The IRS provides a special calculation method

- Prior-year returns do not need to be amended

- Proper reporting can significantly reduce taxable benefits

Handled correctly, lump-sum Social Security benefits become a planning opportunity rather than a problem.

Planning Beyond the Lump-Sum Payment

Discussing lump-sum Social Security benefits often leads to broader planning conversations, including:

- Voluntary withholding on Social Security

- Estimated tax payments

- Medicare premium surcharges

- Coordinating Social Security with pensions or retirement accounts

These conversations strengthen long-term client relationships and reinforce the advisor’s role as a trusted planner.

Final Takeaway

Lump-sum Social Security benefits can feel overwhelming, but the tax rules are designed to be fair. With the correct calculations, accurate reporting, and clear communication, most clients can avoid unnecessary tax stress.

For tax professionals, understanding how lump-sum Social Security benefits are taxed is a valuable way to deliver clarity, confidence, and meaningful guidance during an important financial moment.

GET IN TOUCH

Schedule a FREE Call

Connect on our Socials!