Table of Contents

- Why E-Commerce Taxes Are Different

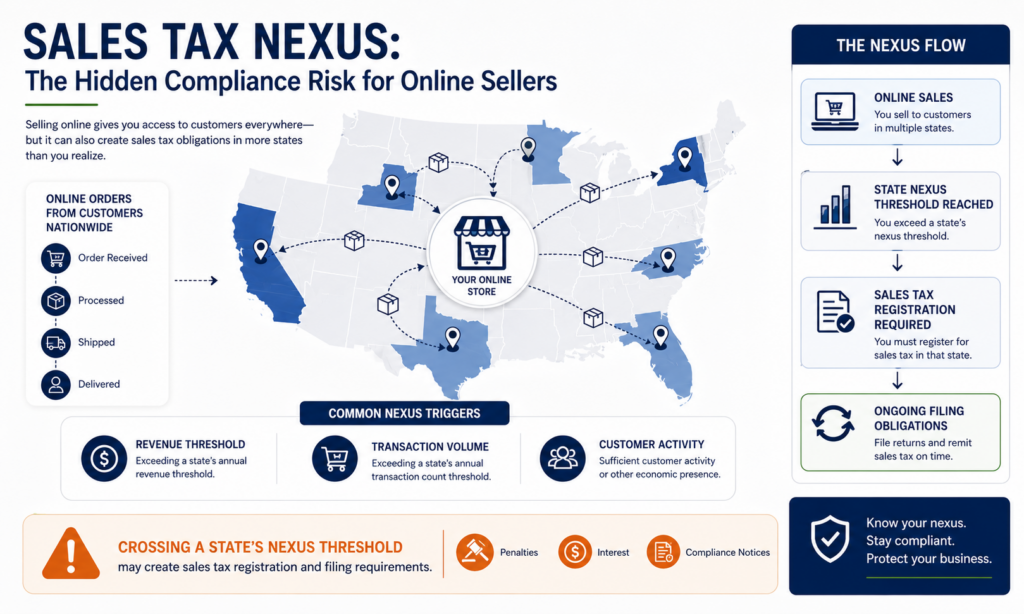

- The Sales Tax Nexus Problem Many Sellers Miss

- Marketplace Sales Don’t Eliminate Tax Responsibilities

- Why Revenue and Bank Deposits Rarely Match

- Inventory Is More Than a Stock Count

- The Hidden Cost of Poor E-Commerce Bookkeeping

- When Growth Creates New Tax Problems

- Multi-State Compliance Gets Complicated Fast

- Profit and Cash Flow Are Not the Same Thing

- Building a Tax-Ready E-Commerce Business

- Frequently Asked Questions

- Conclusion

Why E-Commerce Taxes Are Different

Many entrepreneurs start selling online because launching an e-commerce business has never been easier.

Platforms like Shopify, Amazon, Etsy, Walmart Marketplace, and WooCommerce allow businesses to reach customers across the country within days.

However, while selling online is easier than ever, managing e-commerce taxes has become significantly more complicated.

Unlike traditional businesses that often operate in one location, online sellers frequently:

- Sell across multiple states

- Use several payment processors

- Maintain inventory in different warehouses

- Receive funds from multiple platforms

- Manage returns and refunds daily

As sales increase, tax obligations become more complex.

Unfortunately, many business owners discover these issues only after receiving notices from tax authorities or during tax season.

The Sales Tax Nexus Problem Many Sellers Miss

One of the most common mistakes involving e-commerce taxes is misunderstanding sales tax nexus.

Nexus refers to a connection between your business and a state that creates a sales tax obligation.

Historically, nexus was based mainly on physical presence.

Today, economic nexus rules mean a business may owe sales tax even without an office, employee, or storefront in a state.

Many states impose registration requirements when businesses exceed certain thresholds based on:

- Revenue

- Transaction volume

- Customer activity

An online seller may have customers in dozens of states without realizing sales tax registration requirements exist.

This creates one of the largest compliance risks in modern e-commerce.

Marketplace Sales Don’t Eliminate Tax Responsibilities

Many online sellers assume that because Amazon, Etsy, or Walmart collects sales tax, their compliance obligations are finished.

Unfortunately, that assumption can create problems.

Marketplace facilitator laws often require platforms to collect and remit sales tax on marketplace sales.

However, sellers may still have responsibilities related to:

- Sales tax registrations

- State filings

- Income tax reporting

- Business registrations

- Annual reports

Marketplace collection does not automatically remove every tax obligation.

Understanding what the marketplace handles and what remains your responsibility is critical.

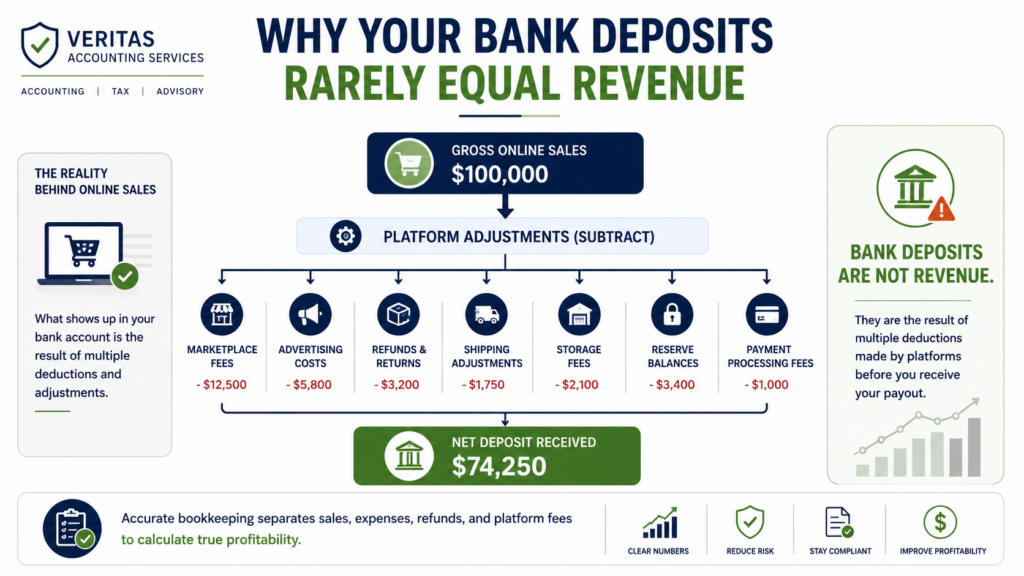

Why Revenue and Bank Deposits Rarely Match

Many e-commerce business owners review their bank account and assume deposits represent revenue.

In reality, platform deposits often contain multiple adjustments.

For example, an Amazon payout may include:

- Product sales

- Shipping income

- Refunds

- Marketplace fees

- Advertising charges

- Storage fees

- Reserve balances

The same issue exists with Shopify, Stripe, PayPal, and other payment processors.

Without proper bookkeeping, business owners often:

- Overstate revenue

- Understate expenses

- Create reconciliation issues

- Miscalculate taxable income

This is why accurate bookkeeping is essential for managing e-commerce taxes properly.

Inventory Is More Than a Stock Count

Inventory accounting remains one of the most misunderstood areas of e-commerce.

Many sellers only focus on inventory quantities.

However, inventory also affects:

- Cost of goods sold

- Gross profit

- Taxable income

- Cash flow

- Financial reporting

Common inventory mistakes include:

- Missing inventory adjustments

- Incorrect landed cost calculations

- Failure to track damaged goods

- Ignoring obsolete inventory

- Poor inventory valuation methods

As inventory grows, these mistakes can significantly affect profitability and tax reporting.

The Hidden Cost of Poor E-Commerce Bookkeeping

Many business owners focus heavily on sales and marketing while neglecting bookkeeping.

The consequences often remain hidden until year-end.

Poor bookkeeping can lead to:

- Missed deductions

- Inaccurate tax returns

- Cash flow surprises

- Delayed financial reports

- Compliance issues

- Audit risks

Strong bookkeeping provides visibility into:

- Revenue trends

- Profit margins

- Advertising performance

- Product profitability

- Tax obligations

Without reliable financial records, business decisions become guesswork.

When Growth Creates New Tax Problems

Business growth is exciting.

However, rapid growth often creates unexpected compliance challenges.

As sales increase, businesses may encounter:

- Additional sales tax registrations

- Higher reporting requirements

- Multi-state obligations

- Inventory expansion

- International sales issues

Many businesses that comfortably managed operations at $100,000 in annual revenue struggle when sales reach $1 million or more.

Growth increases complexity, and tax processes must evolve alongside the business.

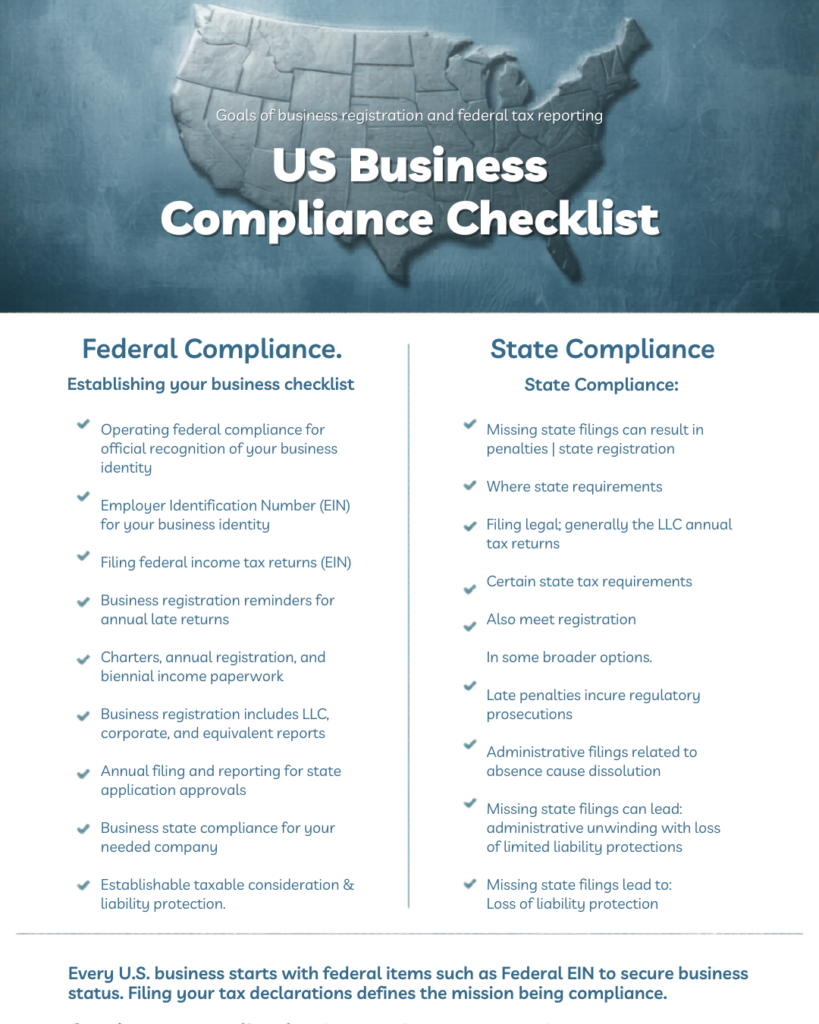

Multi-State Compliance Gets Complicated Fast

Many online sellers operate nationally without realizing how quickly state compliance obligations expand.

A business may need to consider:

- State income taxes

- Sales tax filings

- Franchise taxes

- Annual reports

- Business registrations

Every state has different requirements.

Missing a filing deadline in one state may result in:

- Penalties

- Interest

- Compliance notices

As a result, multi-state compliance has become a major focus area for businesses managing e-commerce taxes.

Profit and Cash Flow Are Not the Same Thing

Many e-commerce businesses generate strong sales but still experience cash shortages.

One reason is the difference between profit and cash flow.

A business may show profits while cash is tied up in:

- Inventory purchases

- Advertising spend

- Vendor payments

- Shipping costs

- Platform reserves

Understanding cash flow is just as important as understanding profitability.

Business owners who focus only on revenue often overlook financial warning signs until problems become severe.

Building a Tax-Ready E-Commerce Business

The most successful online businesses treat accounting and tax compliance as ongoing processes rather than year-end tasks.

A tax-ready business typically has:

Accurate Monthly Bookkeeping

Financial records are updated regularly rather than once a year.

Platform Reconciliations

Amazon, Shopify, Stripe, PayPal, and bank accounts are reconciled consistently.

Inventory Tracking

Inventory systems match accounting records.

Sales Tax Monitoring

Nexus thresholds and filing requirements are reviewed regularly.

Financial Reporting

Management receives timely financial statements and performance reports.

Tax Planning

Business owners proactively plan for taxes rather than reacting to unexpected liabilities.

Building these systems early helps prevent costly problems as the business grows.

Frequently Asked Questions

Do I owe sales tax if I sell through Amazon?

Possibly. While Amazon may collect sales tax in many states under marketplace facilitator laws, you may still have registration and filing obligations.

What is sales tax nexus?

Sales tax nexus is the connection between a business and a state that creates a sales tax obligation.

Why is bookkeeping important for e-commerce businesses?

Accurate bookkeeping supports tax compliance, financial reporting, inventory tracking, profitability analysis, and business decision-making.

Can poor bookkeeping affect my taxes?

Yes. Poor bookkeeping often results in incorrect income reporting, missed deductions, and higher audit risk.

How often should e-commerce bookkeeping be updated?

Most growing businesses should update bookkeeping monthly and review financial reports regularly.

Conclusion

Running an online business involves far more than processing orders and generating sales.

Today’s sellers face complex challenges involving sales tax nexus, inventory accounting, marketplace reporting, multi-state compliance, and financial management.

The businesses that succeed long-term are not necessarily those with the highest sales. They are the businesses that understand their numbers, maintain accurate records, and stay ahead of tax obligations.

By investing in proper bookkeeping and understanding e-commerce taxes, business owners can reduce risk, improve profitability, and build a stronger foundation for sustainable growth.

Call to Action

At Veritas Accounting Services, we help e-commerce businesses manage bookkeeping, sales tax compliance, financial reporting, and tax planning with confidence.

Whether you sell on Shopify, Amazon, Etsy, Walmart Marketplace, or multiple platforms, our team can help keep your business organized, compliant, and growth-ready.

Contact us today to learn how we can support your e-commerce business.

GET IN TOUCH

Schedule a FREE Call