How to Manage Overseas Books of Accounts Without Compliance Risks

Managing overseas books of accounts has become a standard requirement for businesses operating across borders. Whether companies expand through foreign subsidiaries, offshore teams, or international branches, maintaining accurate and compliant financial records in multiple jurisdictions is no longer optional—it is critical to sustainable growth.

Unlike domestic accounting, overseas books of accounts bring added layers of complexity, including different accounting standards, currencies, tax laws, and reporting deadlines. Without strong oversight, even small bookkeeping gaps can lead to regulatory penalties, audit delays, and unreliable consolidated financial statements. Understanding where the risks lie is the first step toward managing them effectively.

Why Overseas Books of Accounts Require Stronger Oversight

Domestic bookkeeping already demands discipline, but overseas books of accounts require additional structure and monitoring. Local accounting practices may differ significantly from group-level expectations, and time zone differences often slow communication.

Many businesses assume that outsourcing overseas bookkeeping transfers compliance responsibility. In reality, accountability always rests with the parent company. Errors in overseas records can affect group financials, tax filings, and investor reporting, making proactive oversight essential.

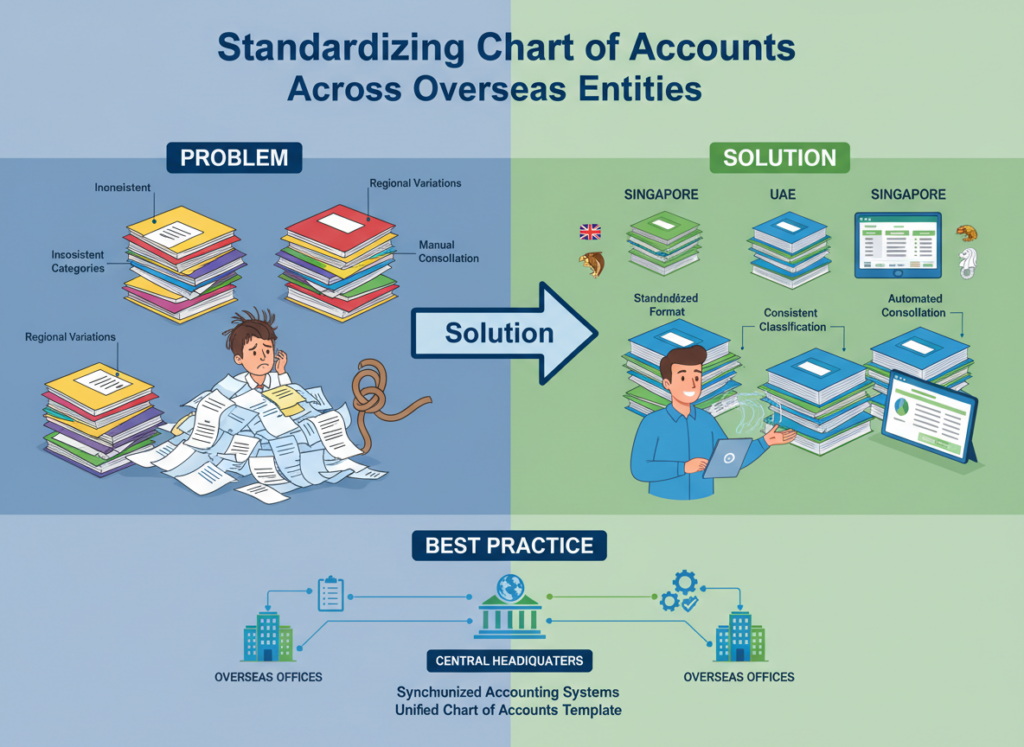

One of the most common issues in overseas books of accounts is inconsistency in chart of accounts design. Local teams may categorize expenses and revenues based on regional norms, which may not align with head-office reporting requirements.

Without standardization, consolidating financials becomes manual and error-prone. Misclassified expenses or inconsistent balance sheet groupings can distort performance analysis.

Best practice:

Implement a standardized chart of accounts across all overseas entities, allowing limited flexibility only where local statutory reporting requires it. This ensures consistency without compromising compliance.

Managing Multi-Currency Transactions Accurately

Currency management is a core challenge when handling overseas books of accounts. Improper application of exchange rates is one of the most frequent causes of financial misstatements.

Key risk areas include:

- Incorrect functional currency selection

- Inconsistent exchange rate usage

- Improper recognition of foreign exchange gains or losses

Even small inconsistencies can materially impact profitability and balance sheet accuracy.

Best practice:

Establish clear policies for exchange rate usage and ensure uniform application across all overseas bookkeeping teams.

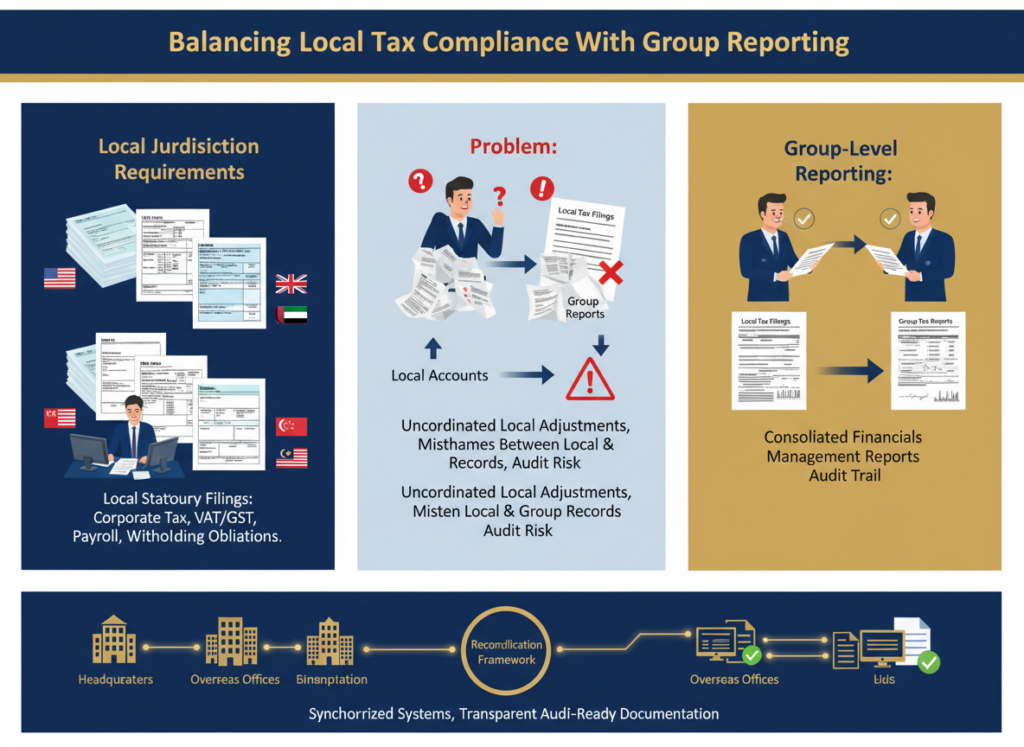

Each jurisdiction imposes its own corporate tax, VAT/GST, payroll, and withholding obligations. Overseas books of accounts must support both local statutory filings and group-level reporting.

Problems often arise when local tax adjustments are booked without informing the parent company. This creates mismatches between local accounts, management reports, and consolidated financials.

Best practice:

Require reconciliations between local tax filings and group financial records, ensuring transparency and audit readiness.

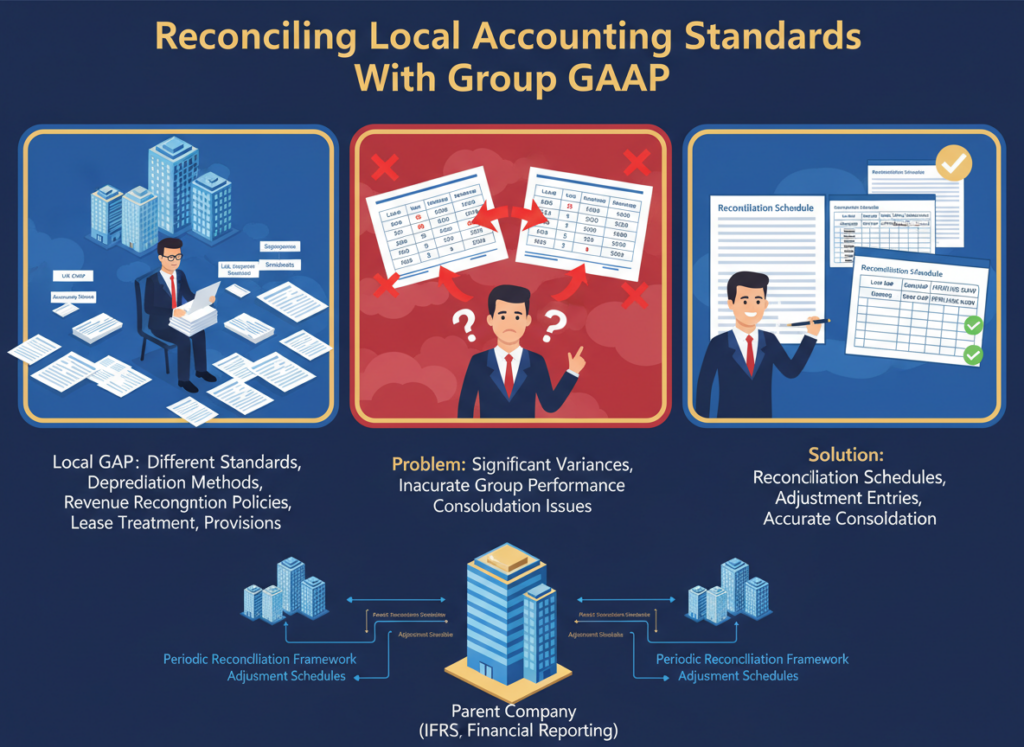

Overseas entities may prepare financials under local GAAP, while the parent company reports under IFRS or US GAAP. Differences in depreciation methods, revenue recognition, leases, or provisions can create significant variances.

If these differences are not adjusted during consolidation, overseas books of accounts may not accurately reflect group performance.

Best practice:

Prepare periodic reconciliation schedules bridging local accounting standards to group reporting frameworks.

Payroll and Employment Compliance Risks

Payroll is one of the highest-risk areas in overseas books of accounts. Each country has unique labor laws, social security requirements, and payroll tax rules.

Common risks include:

- Misclassification of employees and contractors

- Underpayment of social contributions

- Payroll records not matching accounting entries

Payroll errors often attract immediate regulatory scrutiny and penalties.

Best practice:

Reconcile payroll data monthly with general ledger records and review payroll compliance centrally.

Intercompany Transactions and Transfer Pricing Controls

Intercompany transactions are unavoidable in overseas books of accounts. Management fees, royalties, cost allocations, and inventory transfers must be properly documented and priced at arm’s length.

Unreconciled intercompany balances delay month-end close and increase audit risk. Poor documentation can also trigger transfer pricing audits.

Best practice:

Formalize intercompany agreements, apply consistent pricing methodologies, and reconcile balances regularly across entities.

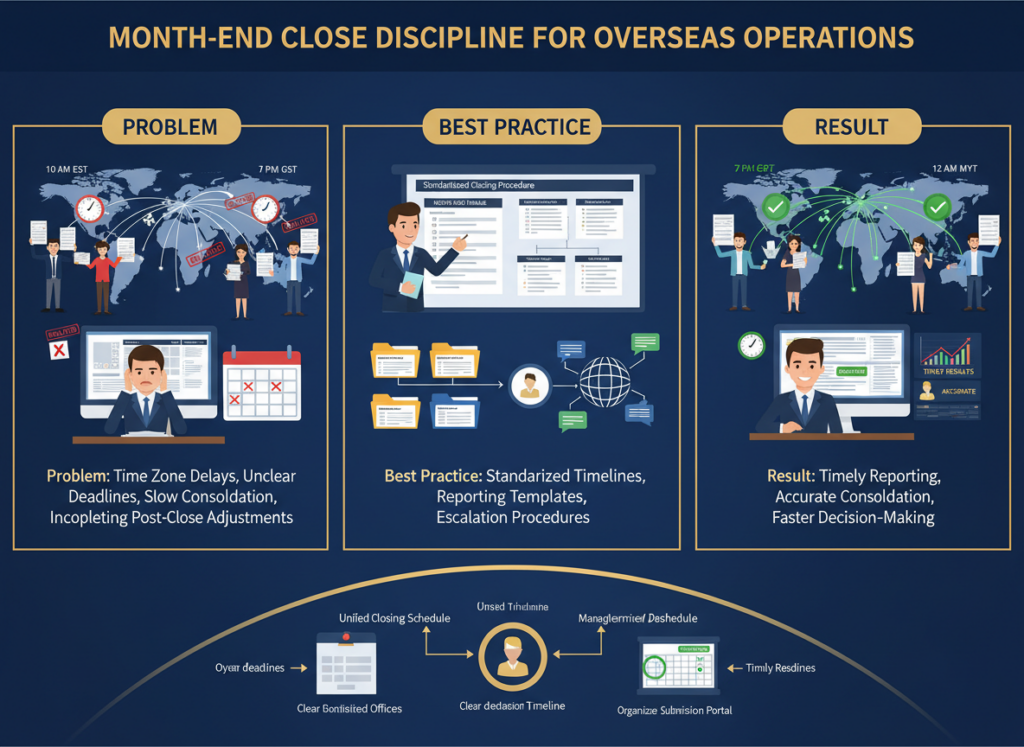

Delayed reporting from overseas teams is a common challenge. Time zone differences and unclear deadlines often slow down consolidation.

Incomplete or rushed reporting undermines decision-making and increases the risk of post-close adjustments.

Best practice:

Set standardized closing timelines, reporting templates, and escalation procedures for all overseas entities.

Internal Controls and Review Frameworks

Weaker oversight increases the risk of errors or fraud in overseas books of accounts. Limited segregation of duties, poor approval processes, or unrestricted system access can compromise financial integrity.

Best practice:

Implement internal control checklists, approval workflows, and periodic internal reviews to strengthen governance.

Audit Readiness and Documentation Management

Audits involving overseas books of accounts often fail due to missing documentation or inconsistent audit trails. Poor recordkeeping extends audit timelines and increases costs.

Best practice:

Maintain organized digital documentation, including invoices, contracts, bank statements, and tax filings, accessible to both local and central teams.

Technology and System Integration

Using different accounting systems across countries creates silos and increases manual work. Data inconsistencies during consolidation are a common outcome.

Best practice:

Adopt centralized accounting platforms where possible, or standardize data exports and validation processes.

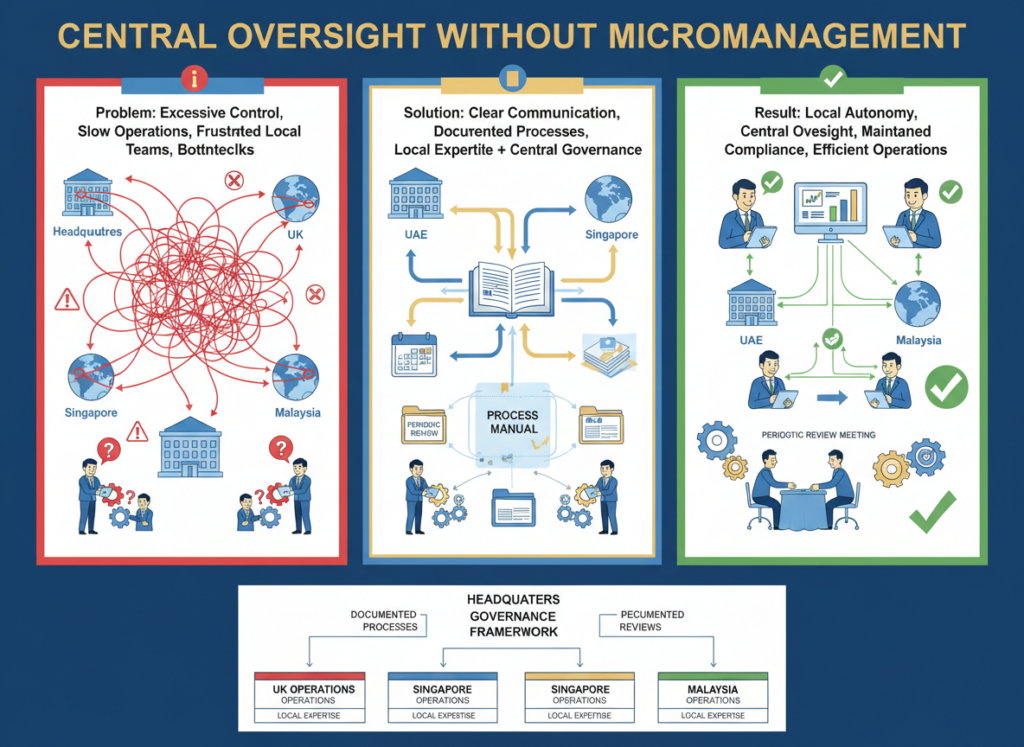

Successful management of overseas books of accounts requires balancing local expertise with central governance. Local teams handle regulatory nuances, while head-office oversight ensures consistency and compliance.

Clear communication, documented processes, and periodic reviews help maintain control without slowing operations.

Final Takeaway

Managing overseas books of accounts is not just a bookkeeping exercise—it is a strategic compliance responsibility. Errors in overseas records can ripple across tax filings, audits, and consolidated reporting.

By focusing on standardization, strong controls, tax alignment, and proactive oversight, businesses can reduce compliance risks and build reliable global financial systems. As international operations grow, disciplined management of overseas books of accounts becomes essential to accuracy, transparency, and long-term success.

GET IN TOUCH

Schedule a FREE Call

Connect on our Socials!