Related-Party Transactions and Transfer Pricing: A helpful Business Owner’s Guide

Table of Contents

- What Is Transfer Pricing?

- Understanding Related-Party Transactions

- Why Tax Authorities Focus on Transfer Pricing

- The Arm’s Length Principle Explained

- Common Types of Related-Party Transactions

- How Transfer Pricing Affects Business Owners

- Transfer Pricing Documentation Requirements

- Common Transfer Pricing Mistakes

- Building a Strong Transfer Pricing Policy

- Frequently Asked Questions

- Conclusion

What Is Transfer Pricing?

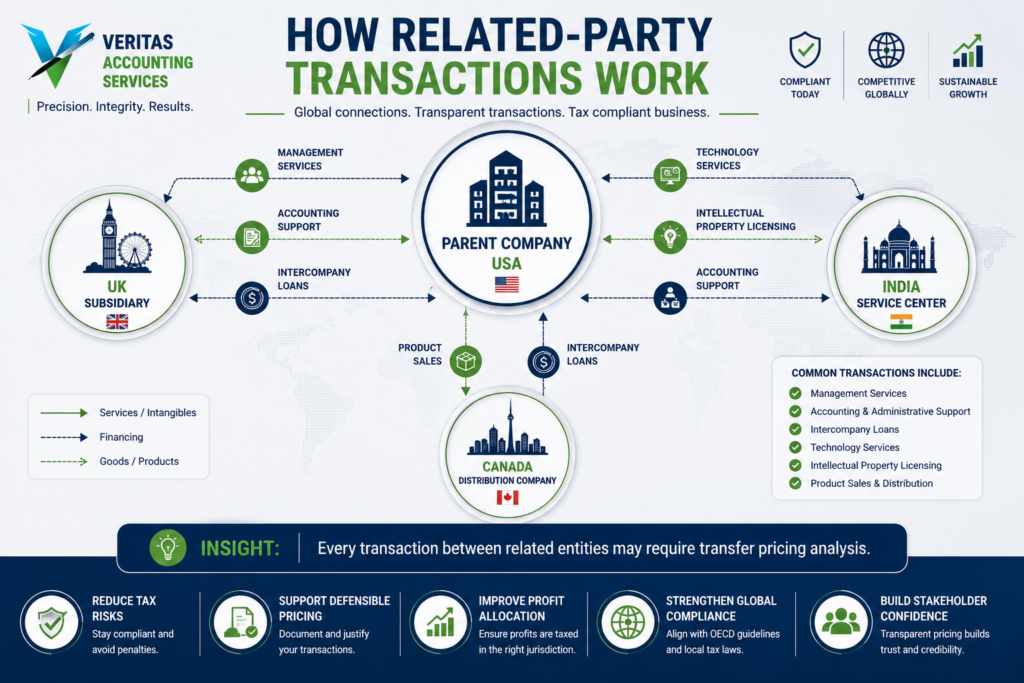

As businesses expand internationally, transactions between related companies become increasingly common.

A U.S. parent company may provide services to its UK subsidiary. An Indian back-office team may support a U.S. business. One group company may license intellectual property to another entity located in a different country.

Whenever related entities transact with each other, transfer pricing becomes important.

Transfer pricing refers to the pricing of goods, services, loans, royalties, or other transactions between companies that are under common ownership or control.

Because these transactions occur between related parties, tax authorities want to ensure the pricing is fair and not designed solely to reduce taxes.

That is why transfer pricing remains one of the most important areas of international tax compliance.

Understanding Related-Party Transactions

Related-party transactions occur when businesses under common ownership conduct transactions with each other.

Examples include:

- Management fees charged between entities

- Shared service arrangements

- Intercompany loans

- Licensing agreements

- Technology support services

- Administrative support

- Product sales between group companies

For example, a UK company may own a U.S. subsidiary.

If the UK company provides accounting, HR, or management support to the U.S. entity, charging for those services creates a related-party transaction.

These transactions are perfectly legal.

The challenge lies in determining the appropriate price.

Why Tax Authorities Focus on Transfer Pricing

Tax authorities are concerned because transfer pricing directly affects where profits are reported and taxed.

Consider a simple example.

A company has:

- One entity in a high-tax country

- One entity in a low-tax country

If the company artificially shifts profits to the low-tax country through improper pricing, overall tax liability may decrease significantly.

Governments recognize this risk.

As a result, tax authorities around the world closely examine transfer pricing arrangements.

Many audits involving multinational businesses focus heavily on intercompany transactions and supporting documentation.

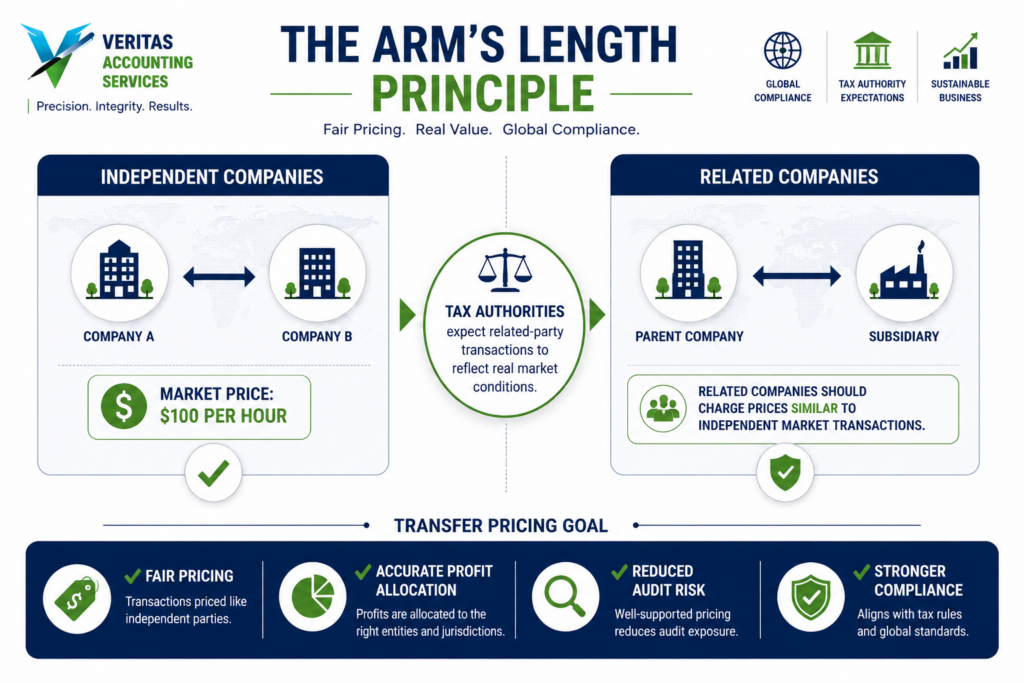

The Arm’s Length Principle Explained

The foundation of transfer pricing is the arm’s length principle.

This principle requires related companies to price transactions as if they were independent parties dealing with each other in the open market.

In simple terms:

Related companies should charge each other the same price that unrelated companies would charge under similar circumstances.

For example:

If a bookkeeping company charges unrelated clients $100 per hour for accounting services, charging a related company $10 per hour may be difficult to justify.

Tax authorities expect businesses to demonstrate that pricing reflects commercial reality.

The arm’s length principle is recognized globally and forms the basis of most transfer pricing rules.

Common Types of Related-Party Transactions

Many business owners believe transfer pricing only applies to large multinational corporations.

In reality, even small and mid-sized businesses may have transfer pricing exposure.

Common transactions include:

Management Services

Parent companies often provide:

- Strategic oversight

- Administrative support

- Executive management

These services frequently require intercompany charges.

Shared Accounting and Bookkeeping Services

One group entity may provide:

- Accounting

- Payroll

- Bookkeeping

- Financial reporting

to other companies within the group.

Intercompany Loans

Loans between related businesses may require:

- Interest charges

- Written agreements

- Transfer pricing analysis

Tax authorities generally expect loan terms to reflect market conditions.

Intellectual Property Licensing

Many businesses own:

- Trademarks

- Software

- Proprietary systems

- Brand assets

Licensing these assets between related entities often creates transfer pricing obligations.

Product Sales Between Group Companies

Manufacturing, distribution, and wholesale groups frequently transfer products between related companies.

Pricing methods must be supported and documented.

How Transfer Pricing Affects Business Owners

Many business owners assume transfer pricing only matters during a tax audit.

In reality, transfer pricing affects:

Tax Compliance

Many jurisdictions require transfer pricing disclosures and documentation.

Financial Reporting

Intercompany transactions must be recorded accurately.

Profit Allocation

Pricing decisions determine where profits are reported.

Audit Risk

Weak documentation can increase audit exposure.

Penalties

Pricing adjustments often result in:

- Additional taxes

- Interest

- Penalties

These costs can become substantial.

Transfer Pricing Documentation Requirements

One of the biggest mistakes businesses make is failing to maintain documentation.

Tax authorities generally expect businesses to demonstrate:

- Why transactions occurred

- How pricing was determined

- What methodology was used

- Why the pricing is reasonable

Strong documentation often includes:

- Intercompany agreements

- Functional analysis

- Benchmark studies

- Financial information

- Supporting calculations

Good documentation is often the first line of defense during a tax examination.

Common Transfer Pricing Mistakes

Many businesses create compliance risks without realizing it.

Common mistakes include:

No Written Agreements

Verbal arrangements between related companies rarely provide adequate support.

Arbitrary Pricing

Some businesses simply choose a number without performing any analysis.

Ignoring Intercompany Services

Administrative and management services are often provided without proper documentation.

Failure to Update Pricing

Business conditions change.

Pricing policies should be reviewed periodically.

Poor Recordkeeping

Missing documentation often creates larger problems than the pricing itself.

Building a Strong Transfer Pricing Policy

A practical pricing policy does not need to be overly complicated.

Most businesses should focus on:

Identifying Related-Party Transactions

Create a list of all intercompany activities.

Establishing Clear Agreements

Document responsibilities, pricing methods, and payment terms.

Applying Consistent Methodologies

Use reasonable and supportable pricing methods.

Maintaining Documentation

Keep records organized and updated.

Reviewing Annually

Business structures evolve.

Pricing policies should evolve as well.

Regular reviews help reduce compliance risks.

Why Smaller Businesses Should Pay Attention

Transfer pricing is often associated with large multinational corporations.

However, smaller businesses increasingly operate internationally through:

- Overseas subsidiaries

- Shared service centers

- Offshore accounting teams

- Remote employees

- Global expansion strategies

As businesses become more international, pricing becomes more relevant regardless of company size.

Ignoring it can create unexpected tax exposure later.

Frequently Asked Questions

What is transfer pricing?

Transfer pricing refers to the pricing of transactions between related companies under common ownership or control.

What are related-party transactions?

Related-party transactions are transactions between businesses that have a common owner, parent company, or controlling interest.

Why is pricing important?

Pricing affects tax compliance, profit allocation, financial reporting, and audit risk.

Does pricing only apply to large corporations?

No. Small and mid-sized businesses with related entities in different countries may also have pricing obligations.

What is the arm’s length principle?

The arm’s length principle requires related companies to price transactions as if they were independent parties dealing in an open market.

Conclusion

As businesses expand across borders, related-party transactions become increasingly common.

Whether your company provides management services, bookkeeping support, technology assistance, intellectual property, or financing to related entities, pricing deserves careful attention.

The goal is not simply compliance.

Proper pricing helps businesses maintain accurate financial reporting, reduce audit risk, support international growth, and avoid costly tax adjustments.

Understanding the fundamentals today can help prevent significant problems tomorrow.

Call to Action

Managing international tax compliance can be challenging, especially for growing businesses operating across multiple jurisdictions.

At Veritas Accounting Services, we help businesses navigate related-party transactions, maintain accurate documentation, and strengthen international tax compliance.

Contact our team today to learn how we can support your global growth strategy.

GET IN TOUCH

Schedule a FREE Call