Living Abroad but Working Online? The UK Tax Residency Rules You Need to Know

Remote work has changed how people live and earn income. Many professionals now work online while living abroad full-time or splitting time between countries.

However, moving overseas does not automatically end UK tax obligations.

Many freelancers, contractors, remote employees, and digital nomads assume they stop being taxable in the UK simply because they relocate abroad. Under HMRC guidance, that is not always correct.

Understanding UK tax residency rules is important because residency determines:

- whether worldwide income becomes taxable in the UK,

- whether Self Assessment filing is required,

- and whether double taxation risks may arise.

For remote workers, misunderstanding UK tax residency rules can lead to unexpected tax bills, penalties, and reporting issues.

What Are UK Tax Residency Rules?

HMRC uses the:

Statutory Residence Test (SRT)

to determine whether a person is resident for tax purposes.

The test mainly considers:

- days spent in the UK,

- work activity,

- family ties,

- accommodation ties,

- and overseas work arrangements.

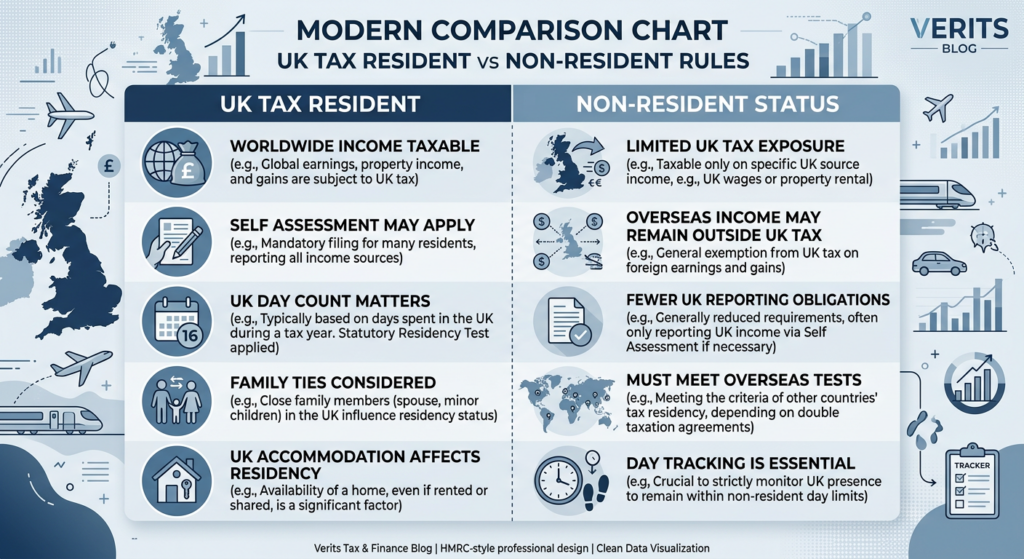

UK tax residency rules are applied separately for each tax year.

The UK tax year runs from:

6 April to 5 April.

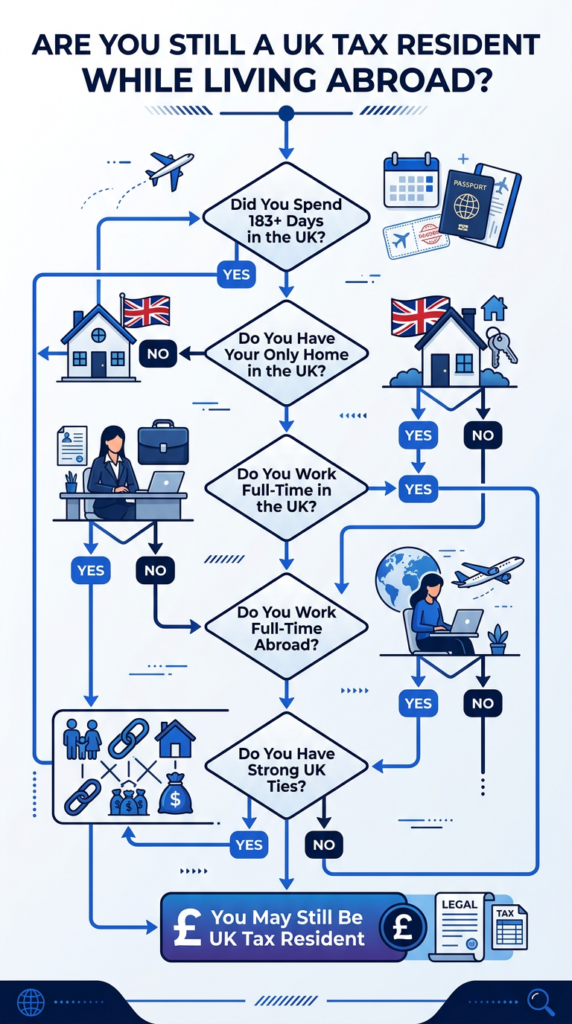

Automatic UK Residence Tests

Under UK tax residency rules, a person automatically becomes UK resident if certain conditions are met.

1. Spending 183 Days or More in the UK

Under UK tax residency rules, you are automatically resident if:

you spend 183 days or more in the UK during the tax year.

This applies even if:

- you work remotely,

- earn foreign income,

- or work for overseas clients.

2. Your Only Home Is in the UK

UK tax residency rules may still treat you as resident if:

- your only available home remains in the UK,

- and you spend at least 30 days there during the tax year.

This commonly affects individuals who move abroad temporarily but continue maintaining a UK property.

3. Full-Time Work in the UK

Under UK tax residency rules, you are generally resident if:

- you work full-time in the UK over a continuous 365-day period.

This may still apply in some hybrid or remote work arrangements.

Automatic Overseas Tests

UK tax residency rules also contain automatic overseas tests that may allow a person to become non-resident.

1. Fewer Than 16 Days in the UK

You are usually non-resident if:

- you spent fewer than 16 days in the UK,

- and you were resident in one or more of the previous 3 tax years.

2. Fewer Than 46 Days in the UK

You are generally non-resident if:

- you spent fewer than 46 days in the UK,

- and you were not resident in all of the previous 3 tax years.

3. Full-Time Work Abroad

Under UK tax residency rules, you may qualify as non-resident if:

- you work full-time abroad,

- spend fewer than 91 days in the UK,

- and work no more than 30 UK workdays.

This is one of the most important parts of UK tax residency rules for remote workers living overseas.

The Sufficient Ties Test

If automatic tests do not determine residency, HMRC applies the:

Sufficient Ties Test.

Under UK tax residency rules, HMRC reviews how strongly connected you remain to the UK.

The more UK ties you have, the fewer days you can spend in the UK before becoming resident.

Family Tie

You may have a family tie if:

- your spouse,

- partner,

- or minor children

are resident in the UK.

Family ties are one of the most important factors under UK tax residency rules.

Accommodation Tie

You may have an accommodation tie if:

- you have a place available to live in the UK for at least 91 days,

- and spend at least 1 night there.

Many remote workers mistakenly assume they become non-resident while continuing to maintain a UK property.

Work Tie

You may have a work tie if:

- you work in the UK for at least 40 days during the tax year.

Under UK tax residency rules:

a UK workday generally means more than 3 hours of work.

90-Day Tie

You may have a 90-day tie if:

- you spent more than 90 days in the UK in either of the previous 2 tax years.

This rule often affects remote workers who frequently travel back to the UK.

Country Tie

A country tie may apply if:

- the UK is the country where you spend the most days during the tax year.

This usually affects individuals leaving the UK.

Why Remote Workers Misunderstand UK Tax Residency Rules

Many people incorrectly believe:

“I moved abroad, so I no longer pay UK tax.”

But UK tax residency rules depend on HMRC tests — not simply physical location.

Common mistakes include:

- keeping a UK home,

- returning frequently,

- working during UK visits,

- ignoring day-count limits,

- and maintaining strong family connections.

Under UK tax residency rules, these factors may still make someone taxable in the UK.

How UK Tax Residency Rules Affect Worldwide Income

If you remain resident for tax purposes, you are generally taxed on:

- employment income,

- freelance earnings,

- overseas business profits,

- foreign rental income,

- investment income,

- and capital gains.

This surprises many freelancers and digital nomads who assume foreign income automatically falls outside UK taxation.

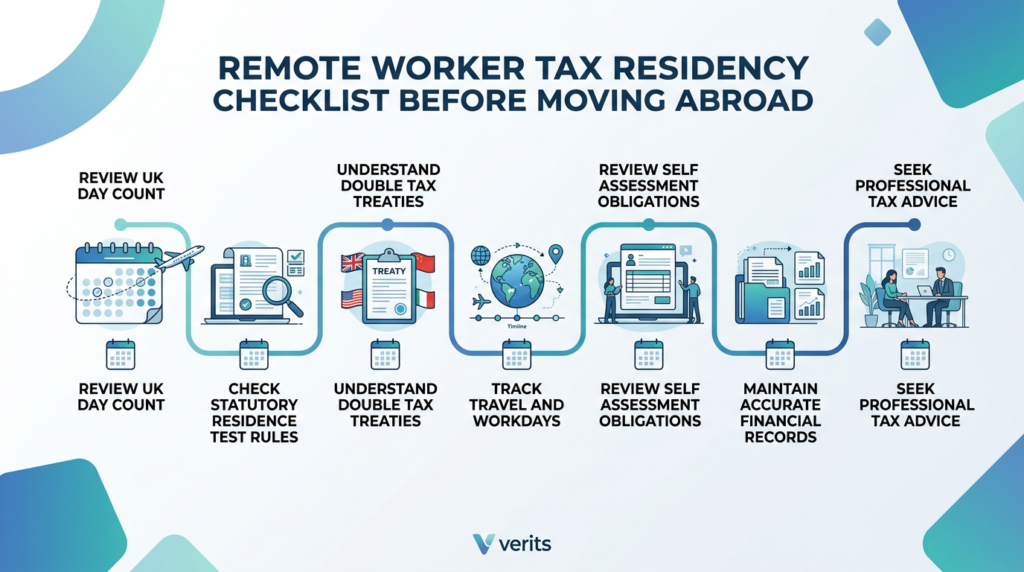

Double Taxation Risks

One of the biggest risks under UK tax residency rules is double taxation.

This happens when:

- the UK treats you as resident,

- and another country also claims residency.

The UK has tax treaties with many countries to help reduce double taxation issues.

These treaties help determine:

- which country has primary taxing rights,

- and where foreign tax credits may apply.

UK Tax Residency Rules for Remote Employees

Remote employees working abroad for UK employers may still face:

- PAYE withholding,

- payroll complications,

- social security obligations,

- and foreign tax exposure.

Employment structure becomes very important under UK tax residency rules.

UK Tax Residency Rules for Freelancers and Digital Nomads

Freelancers and digital nomads often face the most complicated residency situations.

Many:

- move between countries regularly,

- continue using UK banking,

- keep UK ties,

- or fail to establish residency elsewhere.

Under UK tax residency rules, this may still leave them taxable in the UK.

Why Day Tracking Matters

Accurate day counting is critical.

HMRC may review:

- passport activity,

- flight records,

- accommodation records,

- workdays in the UK,

- and travel calendars.

Remote workers should carefully track:

- UK entry dates,

- UK exit dates,

- workdays,

- and overseas work periods.

Poor documentation creates major risks during residency disputes.

Self Assessment Filing Obligations

Even while living abroad, many individuals still need to file:

Self Assessment tax returns.

This may include reporting:

- overseas income,

- freelance earnings,

- investment income,

- and digital platform income.

Incorrect reporting may lead to:

- penalties,

- interest,

- and HMRC compliance checks.

Practical Steps to Manage UK Tax Residency Rules

Remote workers should:

- monitor UK day counts carefully,

- maintain proper bookkeeping,

- separate business and personal finances,

- review residency annually,

- and seek professional advice before relocating abroad.

Planning early is far easier than correcting residency mistakes later.

Final Thoughts on UK Tax Residency Rules

Living abroad does not automatically make someone non-resident for tax purposes.

Under UK tax residency rules, factors such as:

- UK day count,

- accommodation,

- family ties,

- and work activity

can still make a remote worker taxable in the UK.

For freelancers, contractors, remote employees, and digital nomads, understanding UK tax residency rules is essential to avoid:

- unexpected tax bills,

- double taxation,

- and compliance problems.

As remote work continues growing globally, proper tax planning and residency analysis have become increasingly important.

GET IN TOUCH

Schedule a FREE Call

Connect on our Socials!