3 Costly Tax Residency Mistakes That Can Destroy a Client’s Return

Before a tax professional chooses the correct tax form, determines taxable income, or identifies eligible credits, one critical question must be answered first: what is the taxpayer’s residency status for U.S. tax purposes?

Residency determines nearly everything in an international tax return. It affects which income must be reported, what deductions are available, which credits apply, and whether a taxpayer files Form 1040 or Form 1040-NR.

Getting residency wrong is one of the most common and costly tax residency mistakes practitioners make. When the determination is incorrect, the entire return may need to be corrected or amended.

Understanding how IRS residency rules work—and where mistakes typically occur—helps tax professionals protect their clients and prepare accurate returns.

Below are three costly tax residency mistakes that can derail an otherwise correct tax filing.

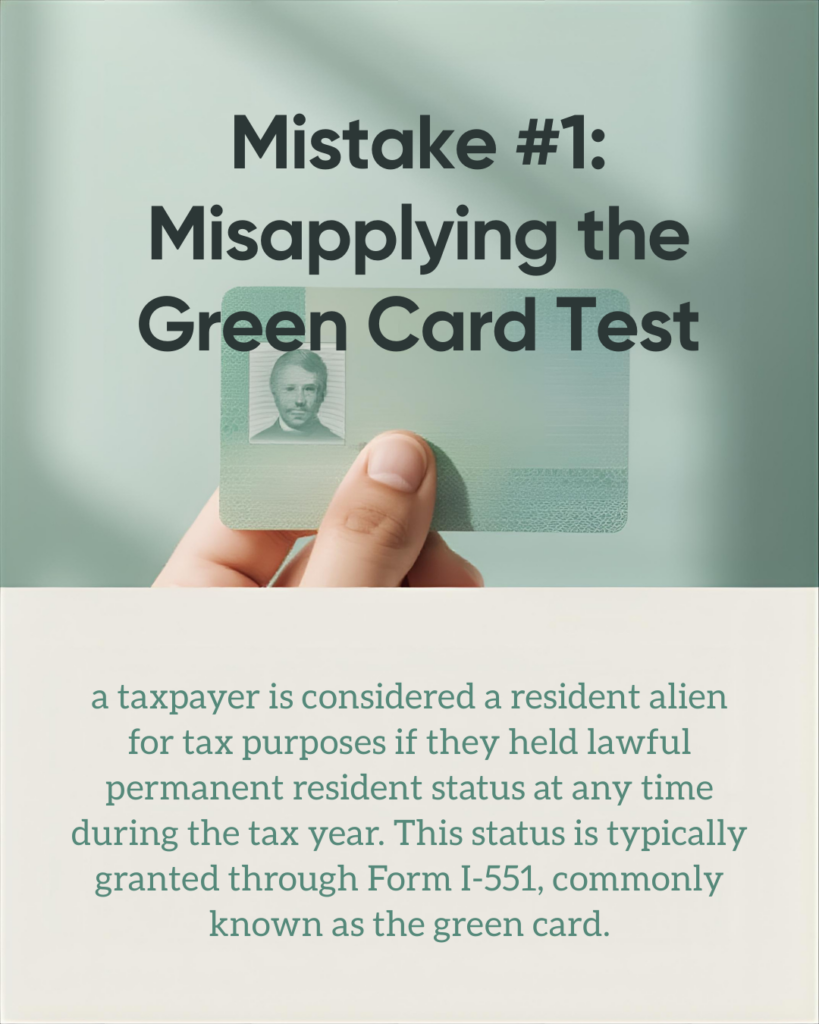

Mistake #1: Misapplying the Green Card Test

The first step in determining residency is applying the green card test. This test is generally straightforward but still frequently misunderstood.

Under IRS rules, a taxpayer is considered a resident alien for tax purposes if they held lawful permanent resident status at any time during the tax year. This status is typically granted through Form I-551, commonly known as the green card.

Once a taxpayer receives lawful permanent resident status, they are treated as a resident for tax purposes unless that status is formally abandoned or rescinded.

The problem arises when immigration timelines do not align perfectly with tax residency periods. For example, a taxpayer may receive green card approval late in the year, which still qualifies them as a resident alien for tax purposes.

Tax professionals must confirm:

- The exact date permanent residency began

- Whether the status was active during the tax year

- Whether any abandonment of residency occurred

Failing to verify these details can result in one of the most damaging tax residency mistakes, because residency status determines the entire reporting framework.

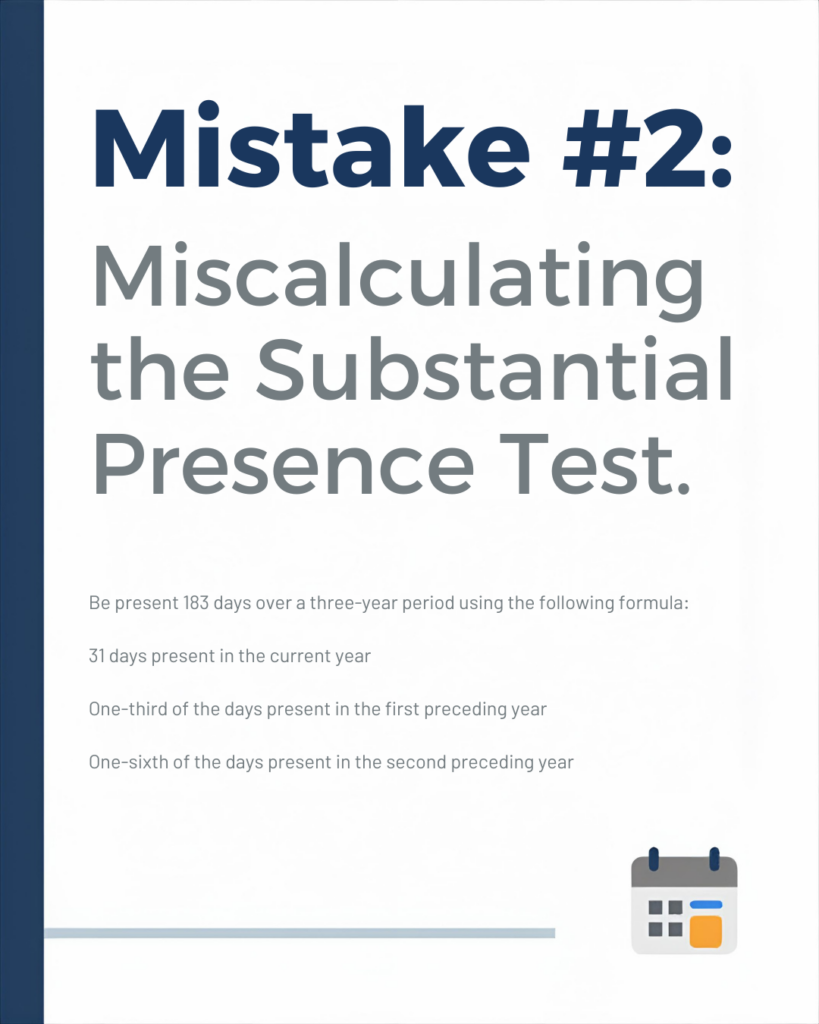

Mistake #2: Miscalculating the Substantial Presence Test

If the taxpayer does not meet the green card test, the next step is applying the substantial presence test.

This is where many practitioners make calculation errors.

To qualify as a resident alien under the substantial presence test, the taxpayer must:

- Be physically present in the United States for at least 31 days during the current year, and

- Be present 183 days over a three-year period using the following formula:

- 31 days present in the current year

- One-third of the days present in the first preceding year

- One-sixth of the days present in the second preceding year

If the total equals or exceeds 183 days, the taxpayer generally meets the residency threshold.

However, simply performing the math is not enough.

Certain individuals are treated as exempt individuals when counting days in the United States. This may include:

- Students on certain visa types

- Teachers and trainees

- Diplomats and foreign government employees

These exemptions mean some days are excluded from the calculation.

Another important consideration is the closer connection exception. If the taxpayer spends fewer than 183 days in the United States during the current year and maintains stronger ties to another country, they may still qualify as a nonresident alien.

However, the closer connection exception is not available if:

- The taxpayer is present in the U.S. 183 days or more during the current year, or

- The taxpayer has applied for permanent residency.

Failing to evaluate these factors is another common tax residency mistake that can dramatically alter how a return should be filed.

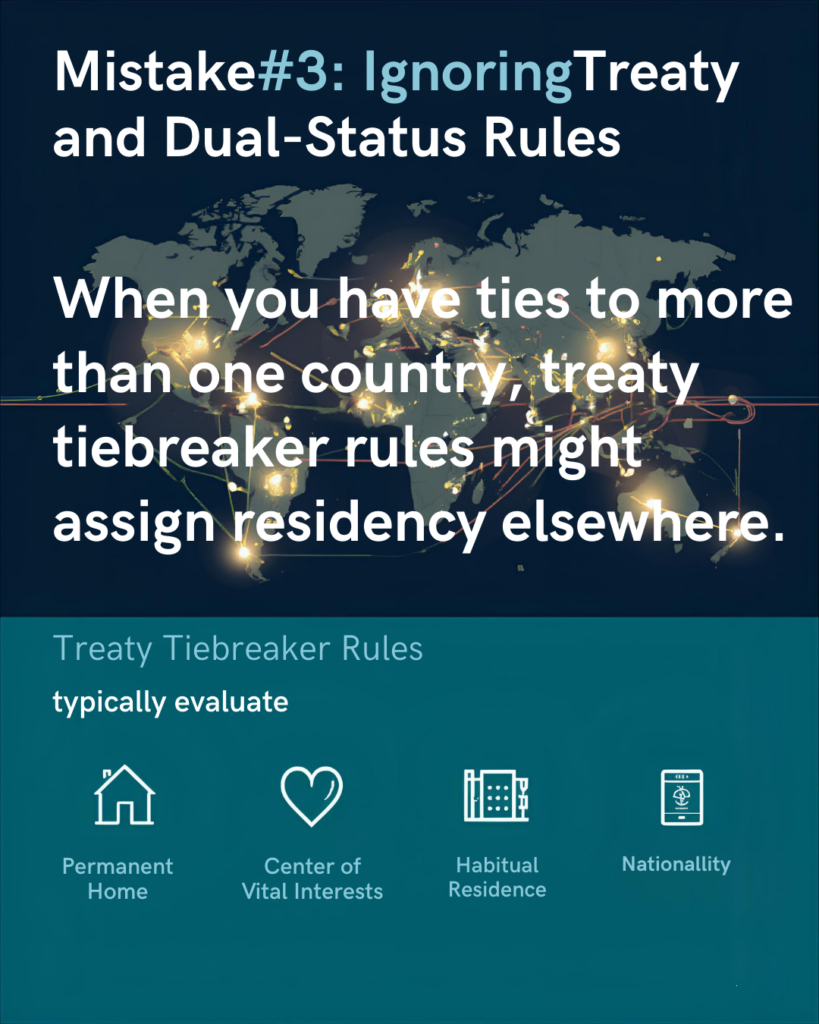

Mistake #3: Ignoring Treaty and Dual-Status Rules

Even when the green card test or substantial presence test indicates residency, the analysis is not always finished.

Income tax treaties can override default residency classifications.

When a taxpayer has ties to more than one country, treaty tiebreaker rules may assign residency to another jurisdiction. These rules typically evaluate:

- Permanent home location

- Center of vital interests

- Habitual place of residence

- Nationality

If the treaty assigns residency to another country, the taxpayer may take a treaty-based position to be treated as a nonresident for certain U.S. tax purposes.

However, this requires careful analysis and proper disclosure on the return.

Another area where tax residency mistakes occur is during dual-status years.

A dual-status year occurs when a taxpayer:

- Arrives in the United States midyear, or

- Leaves the United States during the year

In these cases, the taxpayer is treated as:

- A resident alien for part of the year, and

- A nonresident alien for the remaining period

During the resident portion of the year, the taxpayer is taxed on worldwide income. During the nonresident period, they are taxed only on U.S.-source income or effectively connected income.

Dual-status returns involve special rules that limit certain deductions and credits. Properly allocating income between the two periods requires careful documentation.

Ignoring treaty provisions or dual-status rules is one of the most expensive tax residency mistakes a practitioner can make.

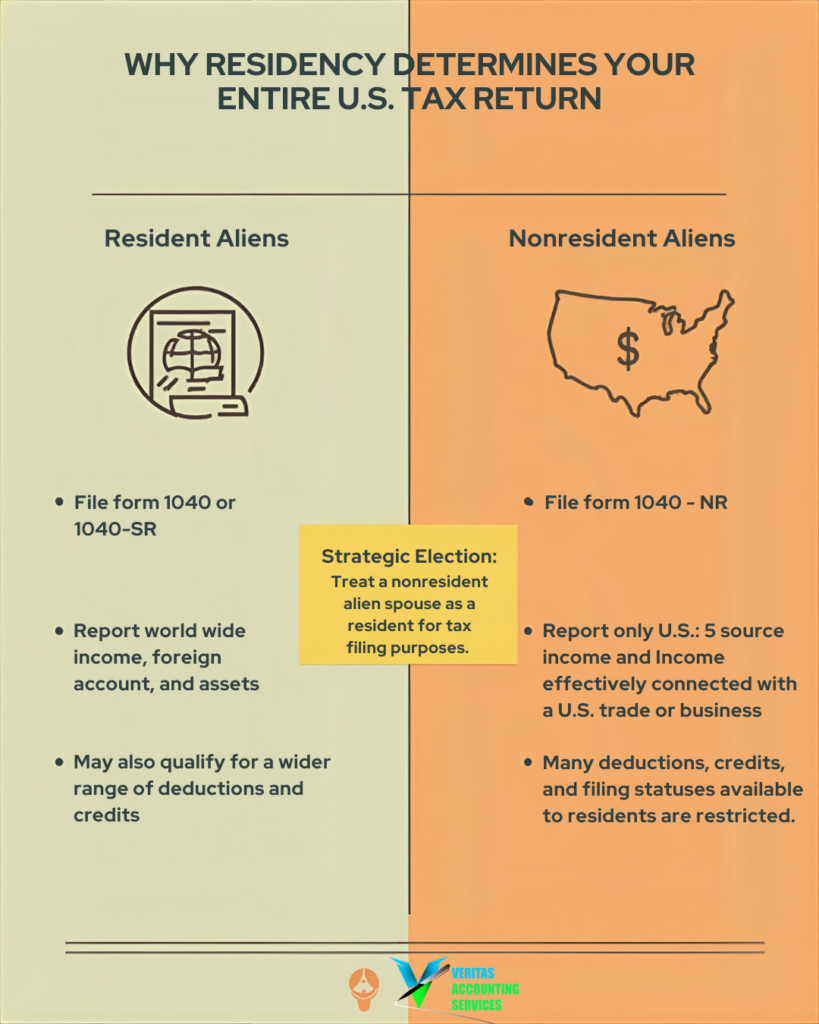

Why Residency Determines the Entire Return

Residency status dictates the correct tax filing path.

Resident Aliens

Resident aliens typically file Form 1040 or Form 1040-SR. They must report:

- Worldwide income

- Foreign accounts

- Foreign assets (when applicable)

They may also qualify for a wider range of deductions and credits.

Nonresident Aliens

Nonresident aliens file Form 1040-NR and generally report only:

- U.S.-source income

- Income effectively connected with a U.S. trade or business

Many deductions, credits, and filing statuses available to residents are restricted.

One strategic election sometimes available is the option to treat a nonresident alien spouse as a resident for tax filing purposes. This allows married couples to file jointly but requires reporting worldwide income for both spouses.

These elections require careful evaluation because they affect future tax years as well and also tax residency mistakes.

Building Confidence in Residency Determinations

For tax professionals working with international clients, determining residency is not a simple label. It is a structured process that requires precision.

Avoiding tax residency mistakes requires careful evaluation of below so that tax residency mistakes can be avoided

- Green card status

- Physical presence calculations

- Visa classifications

- Treaty provisions

- Dual-status rules

Proper documentation and a step-by-step approach ensure that residency is determined correctly before preparing the rest of the return.

When residency is established accurately, the rest of the tax return becomes significantly easier to complete and there is no room for tax residency mistakes.

Final Thoughts

Residency is where the return truly begins.

Misidentifying whether a taxpayer is a resident alien or nonresident alien can unravel an otherwise well-prepared return which leads to tax residency mistakes. Income reporting, deduction eligibility, filing status, and tax treaty benefits all depend on getting this foundational step right.

By understanding the three costly tax residency mistakes outlined above, tax professionals can approach international filings with greater confidence and avoid errors that may expose clients to unnecessary risk.

Precision at the residency stage protects both the taxpayer and the practitioner—and ensures the return starts on the correct footing.

Need Help Navigating Complex Tax Residency Issues?

Determining tax residency correctly is critical when working with international clients, foreign income, or cross-border tax situations.

If you need expert guidance on U.S. tax filings, international tax compliance, residency determinations, or how to resolve tax residency mistakes, our team is here to help.

GET IN TOUCH

Schedule a FREE Call

Connect on our Socials!