Tax-Free Investment Income: The Hidden Opportunity Your Portfolio May Be Missing

In the complex world of investment planning, one of the most overlooked strategies is maximizing tax-free investment income. While many investors focus solely on returns, the smartest wealth builders understand that it’s not what you earn—it’s what you keep after taxes that truly matters.

What is Tax-Free Investment Income?

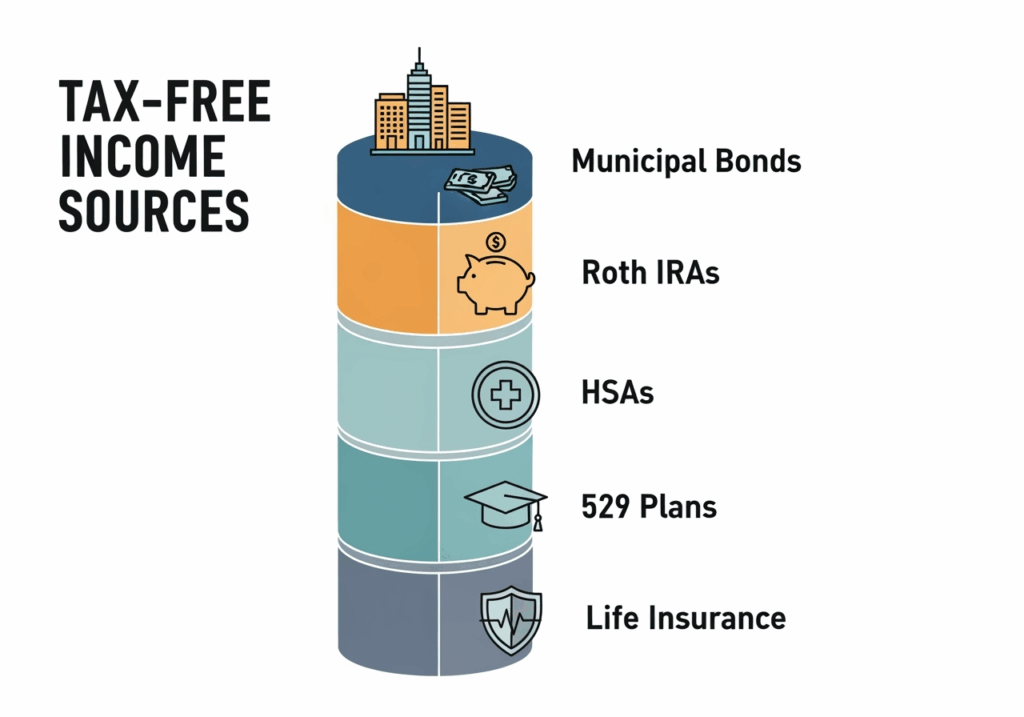

Tax-free investment income refers to earnings from specific investment vehicles that are exempt from federal income taxes, and in some cases, state and local taxes as well. The three primary sources include:

1. Municipal Bonds

Municipal bonds, or “munis,” are debt securities issued by state and local governments to fund public projects. The interest earned from these bonds is typically exempt from federal income tax and may also be exempt from state and local taxes if you live in the issuing state.

Types of Municipal Bonds to Consider:

- General Obligation Bonds: Backed by the full faith and credit of the issuing municipality

- Revenue Bonds: Secured by specific revenue streams from projects like toll roads or utilities

- Private Activity Bonds: May be subject to AMT but offer higher yields

- Build America Bonds: Federally subsidized municipal bonds with taxable interest

2. Roth IRAs

Unlike traditional IRAs, Roth IRA contributions are made with after-tax dollars. However, qualified withdrawals in retirement—including both contributions and earnings—are completely tax-free, making them a powerful long-term wealth-building tool.

Advanced Roth Strategies:

- Roth Ladder Conversions: Systematic conversions over multiple years to manage tax brackets

- Mega Backdoor Roth: For high earners with 401(k) plans allowing after-tax contributions

- Roth IRA Inheritance Planning: Tax-free wealth transfer to beneficiaries

3. Life Insurance Payouts

Certain life insurance policies, particularly permanent life insurance with cash value components, can provide tax-free income through policy loans and withdrawals up to your basis in the policy.

Life Insurance Tax Strategies:

- Modified Endowment Contract (MEC) Avoidance: Structuring policies to maintain tax advantages

- Private Placement Life Insurance (PPLI): For ultra-high-net-worth individuals

- Corporate-Owned Life Insurance (COLI): Business tax planning applications

Additional Tax-Free Income Sources

Health Savings Accounts (HSAs)

Often called the “triple tax advantage” account, HSAs offer:

- Tax-deductible contributions

- Tax-free growth

- Tax-free withdrawals for qualified medical expenses

- After age 65, withdrawals for non-medical purposes are taxed as ordinary income (like a traditional IRA)

529 Education Savings Plans

While contributions aren’t federally deductible, earnings grow tax-free and withdrawals for qualified education expenses are tax-free. Recent expansions allow:

- K-12 tuition payments up to $10,000 annually

- Student loan repayments up to $10,000 lifetime

- Beneficiary changes to family members

Why Tax-Free Investment Income Matters More Than Ever

Protecting Your Overall Tax Picture

Tax-free investment income doesn’t just save you money on taxes—it provides strategic advantages that many investors overlook:

- No impact on taxable income calculations: This income won’t push you into higher tax brackets

- Medicare surcharge protection: High-income earners can avoid additional Medicare premiums triggered by modified adjusted gross income (MAGI)

- Alternative Minimum Tax (AMT) benefits: Tax-free municipal bond interest generally doesn’t trigger AMT calculations

- Social Security taxation: Lower taxable income may reduce the taxation of your Social Security benefits

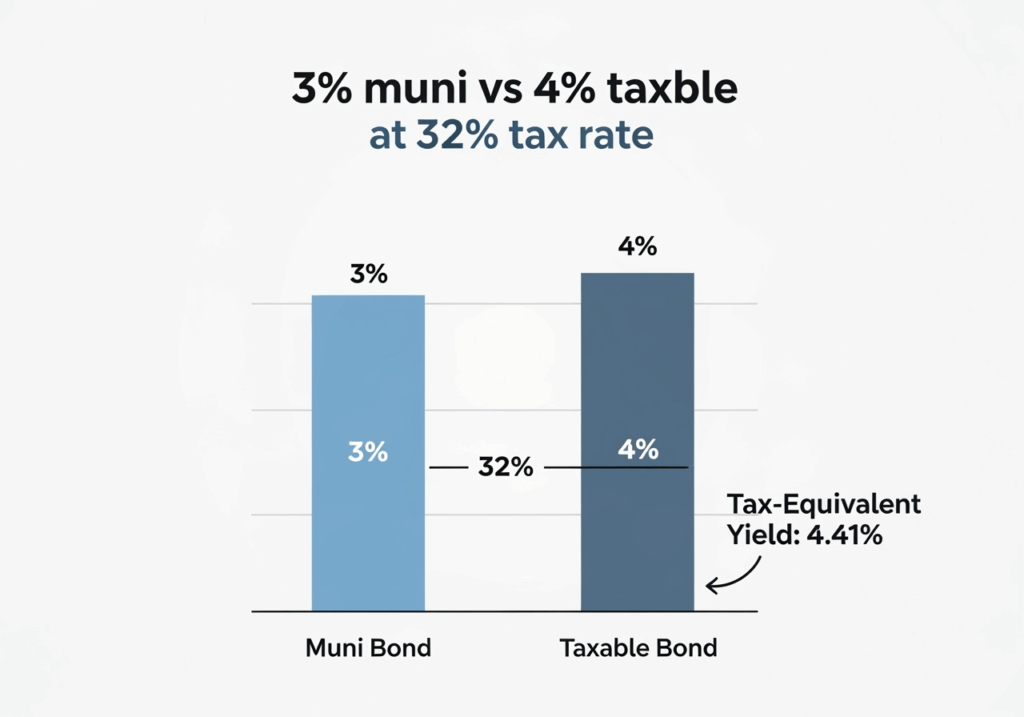

The Compound Effect of Tax Efficiency

Consider this scenario: An investor in the 32% tax bracket earning 4% on taxable bonds nets only 2.72% after taxes. Meanwhile, a municipal bond yielding 3% provides the full 3% return—effectively outperforming the taxable investment while reducing risk.

Tax-Equivalent Yield Formula: Tax-Free Yield ÷ (1 – Tax Rate) = Tax-Equivalent Yield

For a 3% municipal bond and 32% tax bracket: 3% ÷ (1 – 0.32) = 4.41% tax-equivalent yield

Current Market Dynamics

In today’s rising interest rate environment, tax-free investments offer additional benefits:

- Interest rate sensitivity: Shorter-duration municipal bonds provide protection against rate increases

- Credit quality improvements: Many municipalities have strengthened their financial positions post-pandemic

- Supply and demand imbalances: Limited municipal bond issuance has created attractive opportunities

The Missed Opportunity: Why Many Portfolios Aren’t Optimized

Common Portfolio Oversights

Many investors and their advisors focus primarily on gross returns without considering the tax implications. This oversight becomes particularly costly for:

- High-income earners in top tax brackets

- Retirees managing required minimum distributions

- Business owners with fluctuating income levels

- Investors in high-tax states

- Dual-income households approaching higher tax thresholds

The Cost of Inaction

Without proper tax-efficient investment planning, investors may:

- Pay unnecessary taxes on investment income

- Trigger Medicare surcharges

- Face higher Social Security taxation

- Miss opportunities for tax-free wealth accumulation

- Fail to optimize asset location strategies

Behavioral Barriers to Tax-Efficient Investing

Common psychological obstacles include:

- Yield chasing: Focusing on nominal returns rather than after-tax returns

- Complexity avoidance: Avoiding strategies that seem complicated

- Status quo bias: Maintaining existing allocations without optimization

- Tax procrastination: Delaying tax planning until year-end

The Cost of Inaction

Without proper tax-efficient investment planning, investors may:

- Pay unnecessary taxes on investment income

- Trigger Medicare surcharges

- Face higher Social Security taxation

- Miss opportunities for tax-free wealth accumulation

GET IN TOUCH

Schedule a FREE Consultation

Strategic Implementation: Making Tax-Free Income Work for You

1. Portfolio Assessment and Rebalancing

The first step is conducting a comprehensive analysis of your current investment allocation. This involves:

- Evaluating your current tax burden from investments

- Identifying opportunities to shift from taxable to tax-advantaged accounts

- Analyzing the after-tax returns of your current holdings

2. Municipal Bond Strategy

For investors in higher tax brackets, municipal bonds can be particularly attractive:

- General obligation bonds backed by the full faith and credit of the issuer

- Revenue bonds supported by specific project income

- Tax-exempt bond funds for diversification and professional management

3. Maximizing Roth IRA Benefits

Strategic Roth IRA planning includes:

- Roth conversions during lower-income years

- Backdoor Roth strategies for high-income earners

- Long-term planning to maximize tax-free growth

4. Advanced Tax-Free Strategies

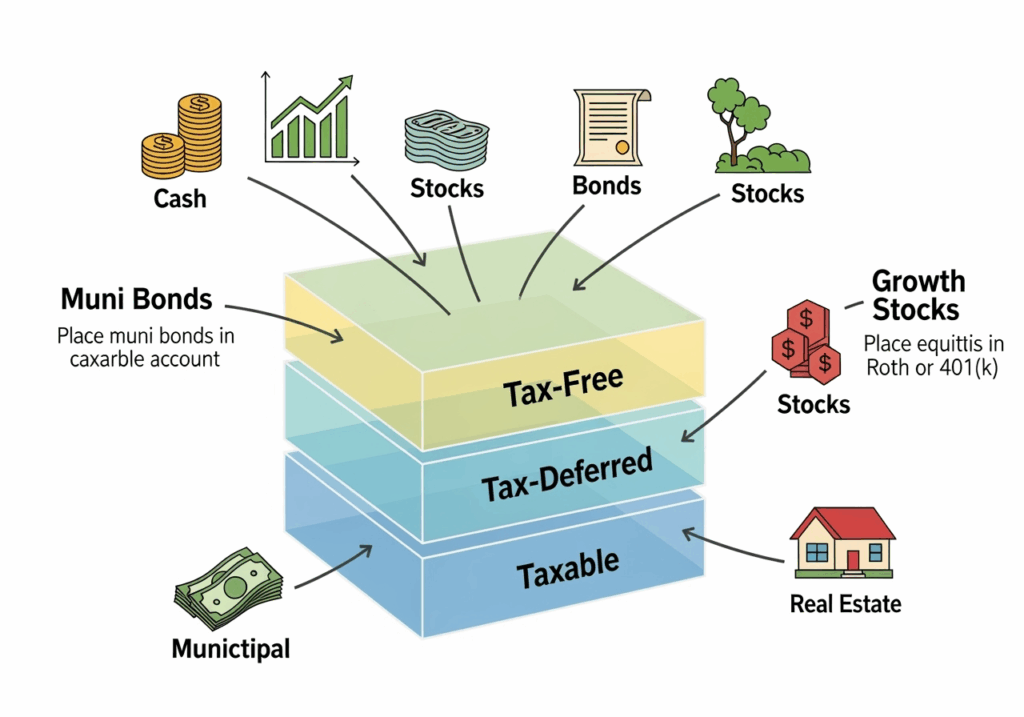

Asset Location Optimization:

- Hold tax-inefficient investments in tax-advantaged accounts

- Place tax-efficient investments in taxable accounts

- Coordinate across multiple account types for maximum benefit

5. Tax-Loss Harvesting Coordination:

- Realize losses in taxable accounts while maintaining tax-free growth elsewhere

- Avoid wash sale rules when rebalancing across account types

- Use tax-free income to reduce the need for taxable rebalancing

Global Considerations for International Investors

At Veritas Accounting Services, we understand that tax-efficient investing becomes even more complex for international investors and expatriates. Our global expertise across the US, UK, UAE, Singapore, Ireland, and Malaysia ensures that your tax-free investment strategy considers:

- Treaty benefits between countries

- Foreign tax credit optimization

- Cross-border retirement planning

- Compliance requirements in multiple jurisdictions

International Tax-Free Opportunities

Different countries offer unique tax-advantaged investment vehicles:

- UK ISAs (Individual Savings Accounts): Tax-free growth and withdrawals

- Singapore CPF: Comprehensive retirement and healthcare savings

- UAE investment structures: Tax-efficient wealth accumulation strategies

- Irish life assurance bonds: Tax-deferred growth opportunities

The Veritas Advantage: Comprehensive Tax-Efficient Planning

With over a decade of experience and 1000+ successful projects, Veritas Accounting Services specializes in creating holistic financial strategies that maximize after-tax returns. Our certified QuickBooks and Xero experts work closely with your investment advisors to ensure your portfolio is optimized for tax efficiency.

Our Integrated Approach Includes:

- Tax planning consultations to identify optimization opportunities

- Investment income analysis and tax impact assessments

- Retirement planning coordination with tax-free income strategies

- Ongoing monitoring to ensure continued tax efficiency

Technology-Driven Solutions

Our seamless integration with leading accounting platforms ensures:

- Real-time tax impact monitoring of investment decisions

- Automated reporting of tax-free income sources

- Coordinated planning between business and personal finances

- Compliance tracking across multiple jurisdictions

Take Action: Don’t Let Tax Inefficiency Erode Your Wealth

The opportunity cost of maintaining a tax-inefficient portfolio compounds over time. Every year you delay implementing tax-free investment strategies is another year of unnecessary tax payments and missed wealth accumulation.

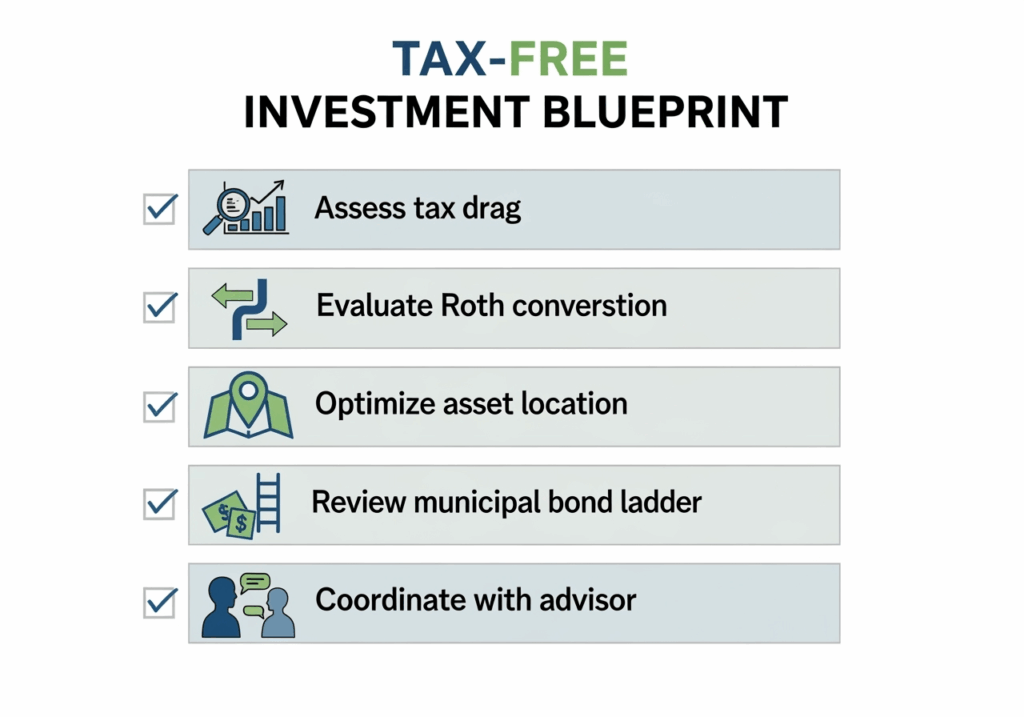

Immediate Action Items:

- Calculate your current tax drag: Determine how much you’re paying in unnecessary investment taxes

- Assess your tax bracket trajectory: Plan for future income changes

- Review your asset location: Ensure tax-efficient placement of investments

- Evaluate conversion opportunities: Consider Roth conversions during low-income periods

Next Steps:

- Schedule a consultation to review your current investment tax burden

- Analyze your portfolio for tax-efficiency opportunities

- Develop a strategic plan to maximize tax-free income

- Implement and monitor your optimized investment strategy

Conclusion

Tax-free investment income isn’t just about avoiding taxes—it’s about building a more efficient, sustainable wealth accumulation strategy. In today’s complex tax environment, the difference between tax-efficient and tax-inefficient investing can mean hundreds of thousands of dollars over a lifetime.

Don’t let this opportunity pass by. Contact Veritas Accounting Services today to discover how tax-free investment income strategies can transform your financial future.

Ready to optimize your investment portfolio for maximum tax efficiency?

Contact Veritas Accounting Services:

• Email: hello@veritasaccountingservices.com

• Phone: +1(678) 723-6003 | +91 9725552243

• US Office: 8735 Dunwoody Place – 4549, Atlanta, GA

• India Office: C-305, The Imperial Heights, 150ft Ring Road, Rajkot

Serving clients globally across the US, UK, UAE, Singapore, Ireland, and Malaysia with expert tax planning and accounting solutions.

GET IN TOUCH

Schedule a FREE Consultation

Connect With Us On Socials!

Tax-Free Investment Income Tax-Free Investment Income Tax-Free Investment Income Tax-Free Investment Income Tax-Free Investment Income Tax-Free Investment Income Tax-Free Investment Income