Big Donation, Bigger Mistake: Why the Tax Court Rejected a $188,563 Charitable Deduction

A large charitable donation may reflect generosity, goodwill, and community spirit. But as one recent Tax Court charitable deduction case proves, generosity alone is never enough to secure a tax benefit.

In early 2026, the U.S. Tax Court rejected a $188,563 noncash charitable contribution claimed by taxpayers in Gibson v. Commissioner. The ruling is a powerful reminder that charitable deductions are governed by strict substantiation rules under §170 of the Internal Revenue Code.

The lesson is clear: documentation determines deductions — not intentions.

The Facts Behind the Tax Court Charitable Deduction Case

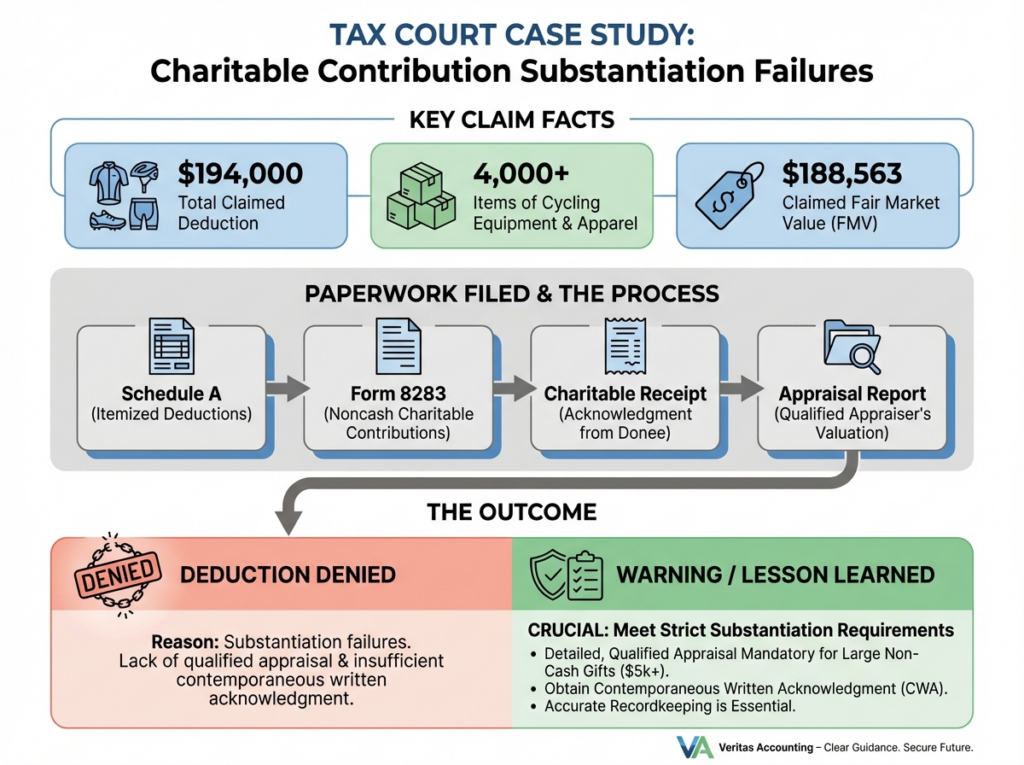

The taxpayers filed a joint 2019 return claiming nearly $194,000 in noncash charitable contributions. The majority of that deduction came from more than 4,000 items described as “high-end cycling equipment apparel.”

The claimed fair market value?

$188,563.

To support the deduction, the taxpayers included:

- Schedule A (Itemized Deductions)

- Form 8283 (Noncash Charitable Contributions)

- A charitable receipt

- An appraisal report (produced during IRS examination)

At first glance, it appeared the paperwork existed. But the Tax Court charitable deduction was ultimately denied because critical substantiation requirements were not satisfied.

Why the Tax Court Charitable Deduction Was Denied

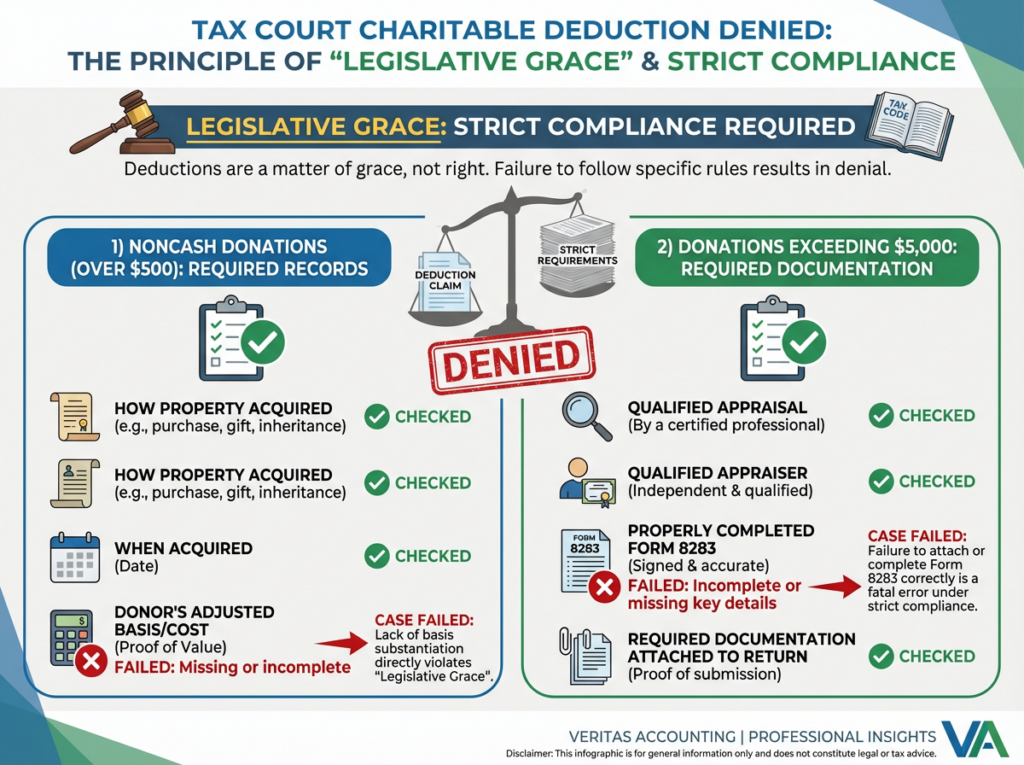

Charitable contribution deductions are considered a “matter of legislative grace.” That phrase means taxpayers must strictly comply with statutory requirements in order to receive the benefit.

Under §170 substantiation rules:

For noncash donations over $500:

Taxpayers must maintain records showing:

- How the property was acquired

- When it was acquired

- The donor’s adjusted basis (cost)

For donations exceeding $5,000:

Taxpayers must obtain:

- A qualified appraisal

- From a qualified appraiser

- Properly complete Form 8283

- Attach required documentation to the return

The Tax Court charitable deduction failed because these requirements were not properly met.

The Critical Basis Problem

One of the biggest weaknesses in the case was the lack of reliable basis information.

The taxpayers claimed the items were received as a gift from a family member. However:

- They could not confirm whether the property was inherited or gifted during the donor’s lifetime.

- They could not establish the original owner’s cost basis.

- They lacked documentation supporting acquisition details.

This matters because the charitable deduction is not always based solely on fair market value.

If the donated property would generate ordinary income or short-term capital gain upon sale, the deduction may be limited to adjusted basis — not fair market value.

Without reliable basis documentation, the court could not verify the allowable amount.

Result: The Tax Court charitable deduction was denied.

The Appraisal Was Not Enough

Although the taxpayers eventually produced an appraisal report, timing and compliance matter.

The court found issues including:

- Failure to establish that the appraiser met the IRS definition of a qualified appraiser.

- Lack of critical acquisition and basis information within the appraisal.

- Questions regarding proper documentation attachment.

Under IRS charitable deduction rules, producing an appraisal after an audit begins does not cure technical filing deficiencies.

The Tax Court charitable deduction demonstrates that compliance must occur at the time of filing.

Fair Market Value Is Not Always the Answer

Many taxpayers believe that fair market value automatically determines the deductible amount. This is incorrect.

In this case, testimony suggested confusion regarding how fair market value applied. The court found no support for assumptions that deductions could be arbitrarily reduced or discounted percentages applied.

The IRS allowed only a small portion of the total claimed noncash charitable contribution.

The remaining $188,563 was disallowed.

Again, the Tax Court charitable deduction ruling reinforces that valuation must align with statutory rules — not personal interpretation.

The Burden of Proof in a Tax Court Charitable Deduction Case

Under §7491(a), the burden of proof generally remains with the taxpayer unless strict recordkeeping requirements are satisfied.

To shift the burden to the IRS, taxpayers must:

- Maintain proper records

- Introduce credible evidence

- Fully comply with substantiation requirements

In this case, the taxpayers failed to meet those standards.

Without adequate charitable deduction documentation, courts will not reconstruct the deduction on behalf of taxpayers.

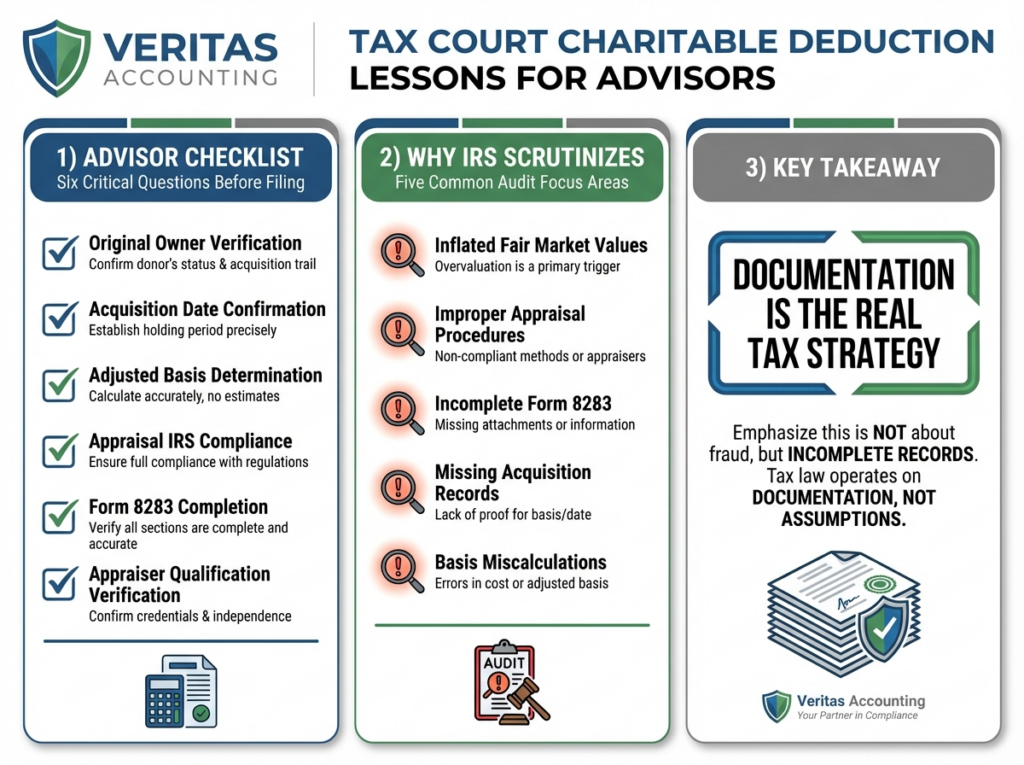

What Tax Professionals Should Learn

The Tax Court charitable deduction decision provides a practical checklist for advisors.

Before filing large noncash charitable contribution deductions, ask:

- Who originally owned the property?

- What was the acquisition date?

- What was the adjusted basis?

- Does the appraisal meet IRS regulatory requirements?

- Is Form 8283 fully completed and attached?

- Has the appraiser’s qualification been verified?

If any of these answers are uncertain, the deduction is vulnerable.

Why the IRS Scrutinizes Large Noncash Charitable Contributions

Noncash charitable contribution deductions are a frequent audit focus area.

Reasons include:

- Inflated fair market values

- Improper appraisal procedures

- Incomplete Form 8283 filings

- Missing acquisition records

- Basis miscalculations

The Tax Court charitable deduction ruling illustrates that the IRS and courts apply strict compliance standards, particularly for high-dollar deductions.

Documentation Is the Real Tax Strategy

This case was not about fraud or intentional misconduct.

It was about incomplete records.

Tax law does not operate on assumption or fairness. It operates on documentation.

Even a legitimate donation will fail if statutory substantiation rules are ignored.

That is the ultimate takeaway from this Tax Court charitable deduction case.

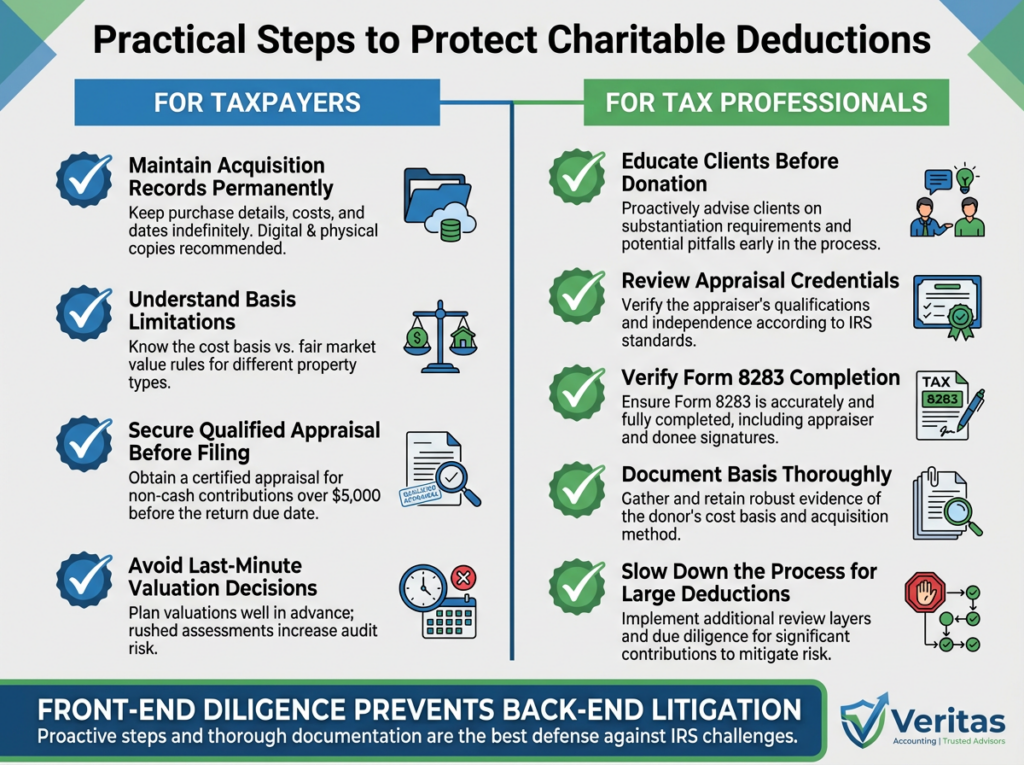

For taxpayers:

- Maintain acquisition records permanently for high-value property.

- Understand basis limitations before claiming fair market value.

- Secure a qualified appraisal before filing.

- Avoid last-minute valuation decisions.

For tax professionals:

- Educate clients before donation occurs.

- Review appraisal credentials.

- Verify Form 8283 completion carefully.

- Document basis thoroughly.

- Slow the process down when large deductions are involved.

Front-end diligence prevents back-end litigation.

Final Takeaway

The Tax Court charitable deduction decision in Gibson v. Commissioner is not about generosity. It is about compliance.

A $188,563 deduction disappeared not because the donation lacked goodwill, but because it lacked technical substantiation.

The court will not fill in missing details. The IRS will not assume accuracy. And fair market value alone will not rescue incomplete documentation.

Charitable giving remains powerful and meaningful. But for tax purposes, the most important word is not generosity — it is documentation.

GET IN TOUCH

Schedule a FREE Call

Connect on our Socials!