Big Change for 2026: When Catch-Up Contributions Must Go Roth

A major retirement planning shift is coming. Beginning in 2026, Roth catch-up contributions 2026 will become mandatory for certain higher-wage employees under SECURE 2.0.

For years, many professionals nearing retirement used pre-tax catch-up contributions to reduce taxable income while increasing retirement savings. That flexibility is changing.

To understand the impact, we first need to break down what catch-up contributions are, how they worked before, and what exactly changes in 2026.

What Are Catch-Up Contributions?

Catch-up contributions are additional retirement plan contributions allowed for individuals age 50 or older.

Normally, retirement plans like 401(k)s limit how much employees can defer from their salary each year. Once someone turns 50, the IRS allows them to contribute an extra amount above the standard annual limit.

These extra contributions are called catch-up contributions.

The purpose is simple:

- Help older workers accelerate retirement savings

- Make up for years when contributions may have been lower

- Provide tax planning flexibility near retirement

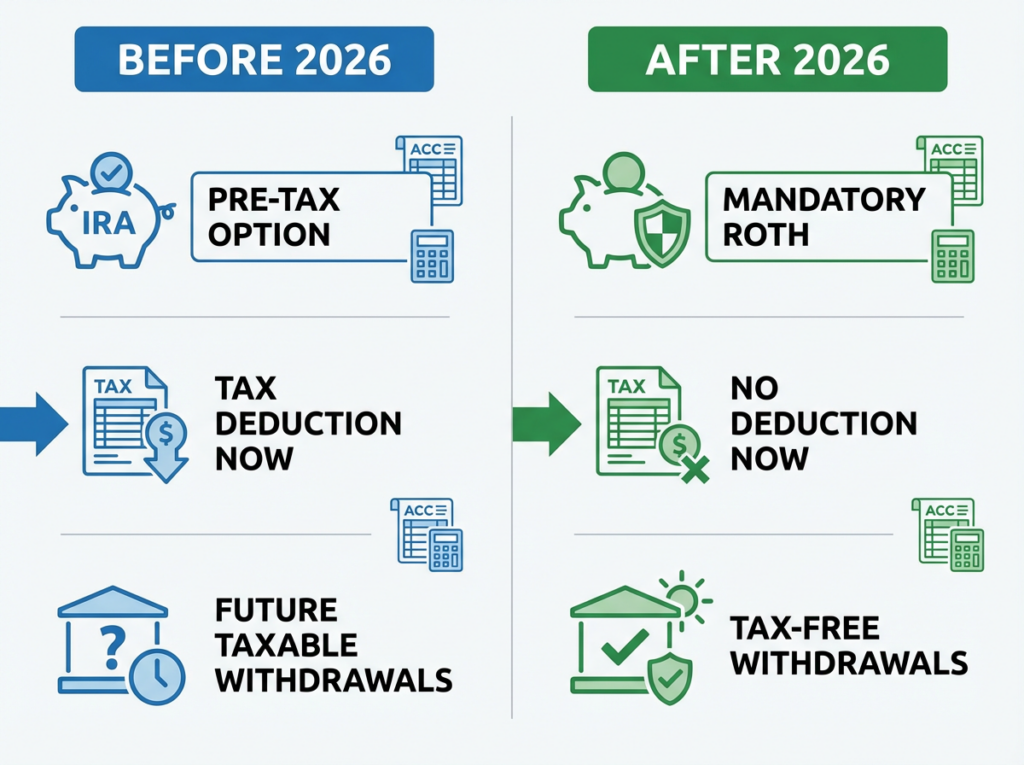

Before 2026, catch-up contributions could be made either:

- On a pre-tax basis, or

- On a Roth basis, if the plan allowed

That flexibility gave high earners powerful tax planning options.

What Is a Roth Catch-Up Contribution?

A Roth catch-up contribution is simply a catch-up contribution made on an after-tax basis.

This means:

- The contribution is included in current taxable income

- Taxes are paid now

- Qualified distributions in retirement are tax-free

By contrast, pre-tax catch-up contributions:

- Reduce current taxable income

- Defer taxes until retirement

- Are fully taxable when withdrawn

Until now, employees could choose between these two treatments.

How Catch-Up Contributions Worked Before 2026

Before the Roth catch-up contributions 2026 rule:

- Employees age 50+ could make catch-up contributions.

- They could elect pre-tax treatment.

- They could elect Roth treatment.

- The choice was entirely voluntary.

Many high earners preferred pre-tax catch-up contributions because they reduced current-year taxable income during peak earning years.

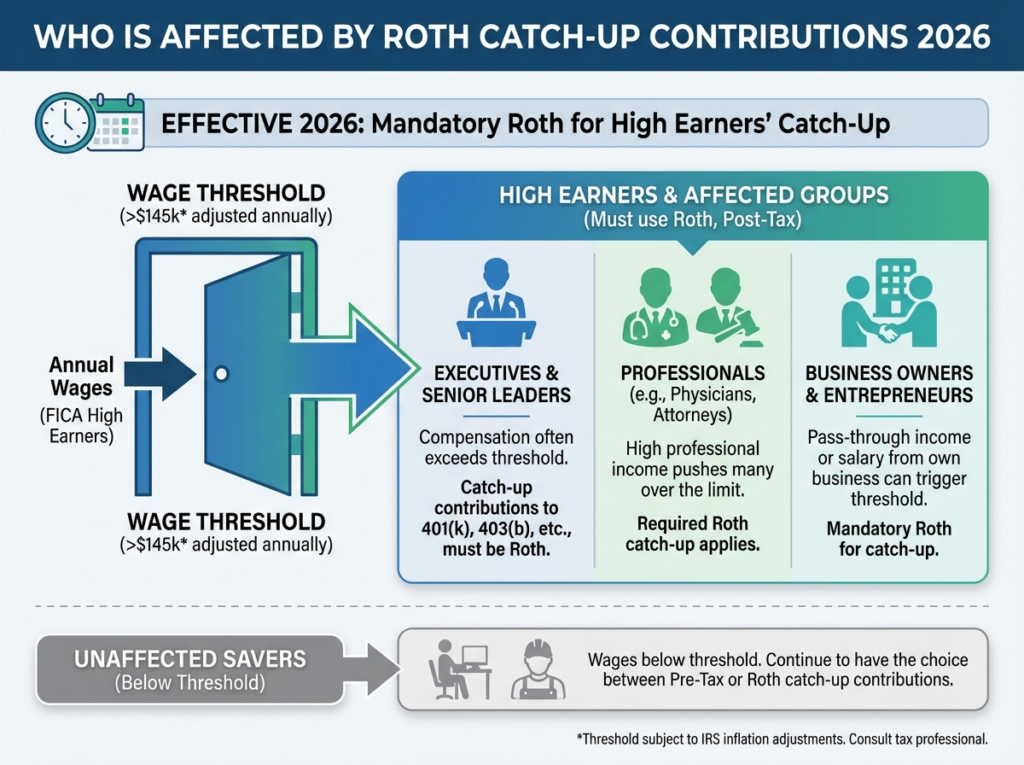

This strategy was particularly useful for:

- Executives

- Physicians

- Business owners

- Professionals nearing retirement

That voluntary flexibility disappears in 2026 for certain employees.

What Is Changing in 2026?

Under SECURE 2.0, a new provision under §414(v)(7)(A) introduces the mandatory Roth catch-up rule.

Beginning with taxable years after December 31, 2026:

If an employee’s prior-year FICA wages exceed the indexed wage threshold, their catch-up contributions must be made as Roth.

That means:

- No pre-tax option for catch-up contributions

- Catch-up contributions must go to a designated Roth account (DRA)

- Current taxable income increases

This is the core of the Roth catch-up contributions 2026 change.

Who Is Affected by Roth Catch-Up Contributions 2026?

The rule applies to employees whose prior-year FICA wages from the same employer exceed an indexed threshold.

Important clarifications:

- Wages are determined using Box 3 of Form W-2 (FICA wages)

- Not Box 1 taxable wages

- Not total household income

- Not self-employment income

If prior-year wages exceed the threshold:

Catch-up contributions must be Roth.

If wages do not exceed the threshold:

Employees may still choose pre-tax catch-up contributions.

New hires without prior-year FICA wages from the employer are not subject to the rule for that year.

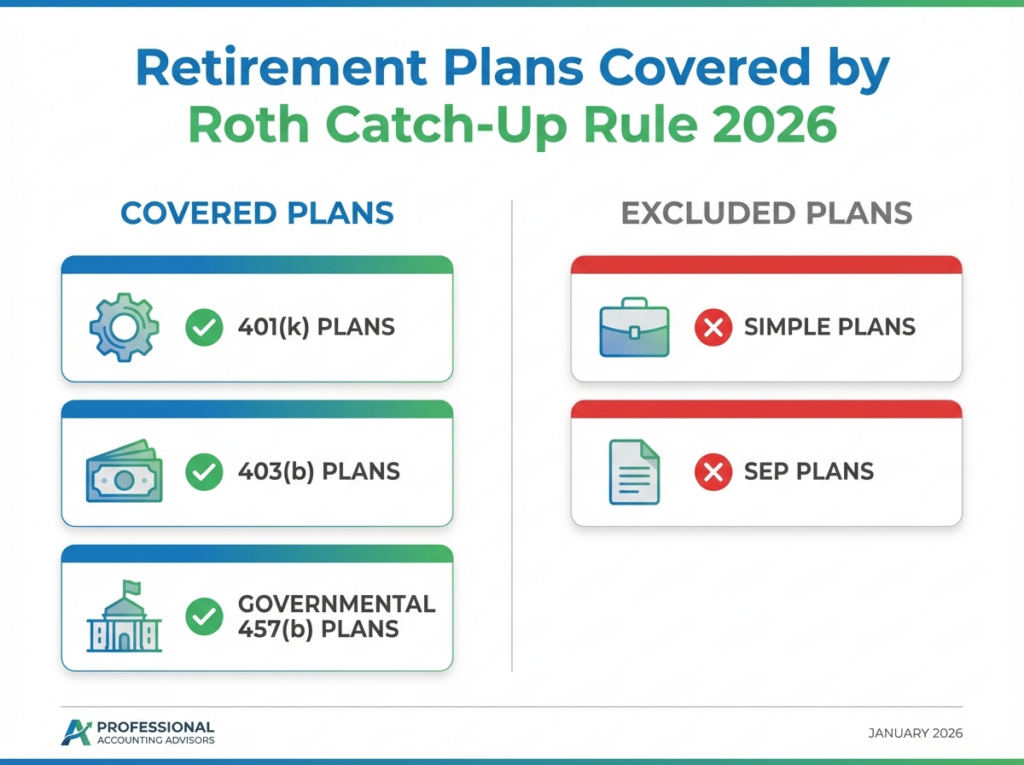

Which Retirement Plans Are Covered?

The Roth catch-up contributions 2026 rule applies to:

- §401(k) plans

- §403(b) plans

- Governmental §457(b) plans

It does not apply to:

- SIMPLE plans

- SEP plans

This means most common employer-sponsored defined contribution plans must comply.

What About the Higher Age-Based Catch-Up Increase?

SECURE 2.0 also increased catch-up limits for employees ages 60–63.

However, this change does not override the Roth requirement.

If the wage threshold is met:

- Standard catch-up contributions must be Roth

- Higher age-based catch-up contributions must also be Roth

The amount increases.

The tax treatment does not change.

What Happens If the Plan Does Not Offer Roth?

This is a significant issue.

Employer plans are not required to offer Roth contributions. But if they do not include a Roth feature:

Employees subject to Roth catch-up contributions 2026 cannot make catch-up contributions at all.

They cannot contribute them pre-tax.

They cannot contribute them Roth.

As a result, many plan sponsors are amending plan documents and updating payroll systems ahead of 2026.

Immediate Tax Impact for High Earners

The biggest shift under Roth catch-up contributions 2026 is the tax timing.

Before 2026:

Catch-up contributions reduced taxable income.

After 2026:

Catch-up contributions increase taxable income.

For example:

If a client contributes $7,500 in catch-up contributions:

- Previously: taxable income decreased by $7,500

- Now: taxable income increases by $7,500

This affects:

- Federal tax liability

- State income taxes

- Withholding amounts

- Estimated payments

- Medicare premium exposure

Cash flow planning becomes essential.

Why Congress Made This Change

The SECURE 2.0 Roth catch-up rule is largely a revenue acceleration measure.

By forcing higher earners to contribute catch-up amounts on a Roth basis:

- Taxes are collected now

- Instead of deferred decades into retirement

This increases short-term federal revenue.

For savers, however, the retirement savings opportunity remains intact — only the tax timing changes.

Strategic Planning Opportunities

Even though Roth catch-up contributions 2026 eliminate pre-tax flexibility for certain earners, strategic planning remains possible.

Tax professionals can help clients:

- Adjust regular deferral elections

- Optimize withholding

- Evaluate Roth conversions

- Coordinate charitable planning

- Diversify retirement income streams

In some cases, forced Roth contributions may actually enhance long-term tax diversification.

Payroll and Employer Compliance

Employers must:

- Identify employees above the wage threshold annually

- Update payroll systems

- Amend plan documents if necessary

- Communicate changes clearly

Treasury regulations generally apply after December 31, 2026. Earlier implementation is allowed under good-faith interpretation.

Employers should begin preparation well before 2026.

The Bottom Line

The Roth catch-up contributions 2026 rule marks one of the most significant retirement tax changes in recent years.

Before 2026:

Catch-up contributions could be pre-tax or Roth.

After 2026:

Certain high-wage employees must contribute catch-up amounts on a Roth basis.

The opportunity to save remains.

The tax timing changes.

For high earners and tax professionals, preparation now prevents surprises later.

Understanding what catch-up contributions are, how Roth catch-ups work, and how Roth catch-up contributions 2026 alter the landscape ensures smarter retirement planning in the years ahead.

The shift to Roth catch-up contributions 2026 does not eliminate retirement savings opportunities — it changes when taxes are paid. With careful modeling and timely adjustments, this new rule can be integrated into a broader, long-term retirement strategy.

Smart preparation in 2025 will make 2026 a planning opportunity, not a tax surprise.

GET IN TOUCH

Schedule a FREE Call

Connect on our Socials!