IRS First-Time Abatement 2026: New Automatic Penalty Relief Explained

The first-time abatement 2026 update marks a major shift in how the IRS administers penalty relief for taxpayers. For years, taxpayers struggled with penalty notices—many not knowing that the IRS offered a First-Time Abatement (FTA) program at all. The IRS required taxpayers or tax professionals to call, write, or file a request to receive the penalty waiver.

Starting in 2026, the IRS will automatically apply first-time abatement 2026 relief when a taxpayer qualifies. This is one of the most significant modernization steps in recent IRS history.

This blog breaks down what first-time abatement 2026 means, who qualifies, how the automatic waiver works, and what tax professionals must do to prepare.

⭐ What Is First-Time Abatement (FTA)?

First-Time Abatement (FTA) has existed since 2001 and is one of the most widely applicable forms of IRS penalty relief. FTA is available for taxpayers who have a good compliance history and need relief from certain penalties.

Under first-time abatement 2026, the IRS will shift from a request-based model to an automatic system—helping millions of taxpayers who previously missed out due to lack of awareness.

FTA applies only to penalties related to:

- Failure to file

- Failure to pay

- Failure to deposit (for payroll taxes)

These penalties can be substantial, and first-time abatement 2026 may prevent financially strained taxpayers from paying unnecessary penalties.

📌 Penalties Eligible Under First-Time Abatement 2026

FTA continues to apply to only three penalty categories. Under the first-time abatement 2026 system, these penalties will be reviewed automatically:

✔ Failure to File Penalty

Assessed when a taxpayer submits a return after the due date.

✔ Failure to Pay Penalty

Applied when taxes remain unpaid by the deadline.

✔ Failure to Deposit Penalty

Relevant to employers who do not deposit payroll taxes on time.

Under first-time abatement 2026, these penalties may no longer require taxpayers to call the IRS or file Form 843 to request relief.

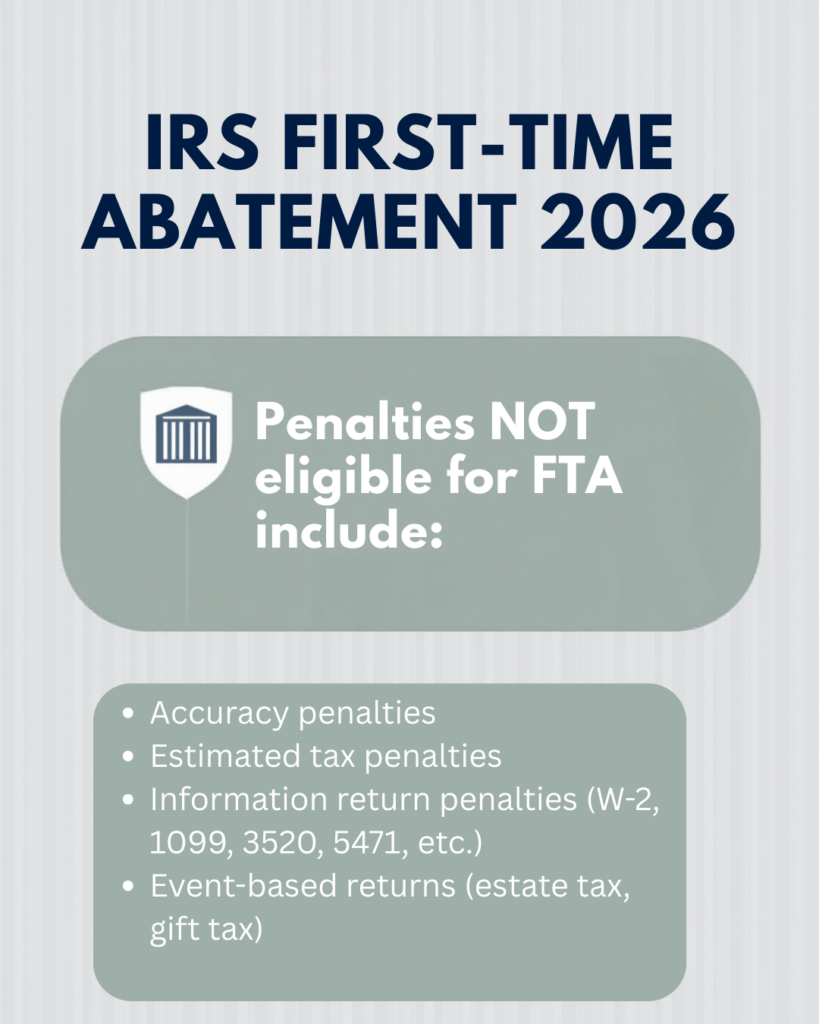

❌ Penalties NOT eligible for FTA include:

- Accuracy penalties

- Estimated tax penalties

- Information return penalties (W-2, 1099, 3520, 5471, etc.)

- Event-based returns (estate tax, gift tax)

🧾 Who Qualifies for First-Time Abatement 2026?

To qualify for first-time abatement 2026, taxpayers must meet existing FTA rules. These requirements remain unchanged.

🔹 1. Eligible Return Types

FTA applies only to:

- Individual: Form 1040 series

- Business: Form 1120, Form 1065

- Payroll: Form 940, 941, 944, 945

Not eligible under first-time abatement 2026:

Form 990 series, gift tax returns, estate tax returns, international forms.

🔹 2. Clean Compliance History

Taxpayer must have:

- No disqualifying penalties in the three years prior to the penalty year

- Estimated tax penalties do NOT disqualify

- For joint returns: BOTH spouses must meet the criteria

- For payroll taxes: must not have more than three prior Failure to Deposit waivers

Even under first-time abatement 2026, the IRS will evaluate compliance history before applying automatic relief.

🔹 3. Filing Compliance

All required tax returns for the previous three years must be filed.

This rule is unchanged under the first-time abatement 2026 automatic system.

🔹 4. Good Standing on Balances

Taxpayers must be current with IRS agreements or payment plans.

Automatic FTA in first-time abatement 2026 will be blocked if a taxpayer is not in good standing.

🚀 What’s Changing in 2026?

Currently, taxpayers must manually request FTA by:

- Calling the IRS

- Writing a letter

- Filing Form 843

Beginning in first-time abatement 2026, the IRS will automatically issue the waiver when all criteria are met.

This modernization comes after years of recommendations from:

- Treasury Inspector General for Tax Administration (TIGTA)

- National Taxpayer Advocate (NTA)

- Industry tax associations

In November 2025, Erin Collins (NTA) confirmed that the IRS will be implementing the automatic first-time abatement 2026 capability.

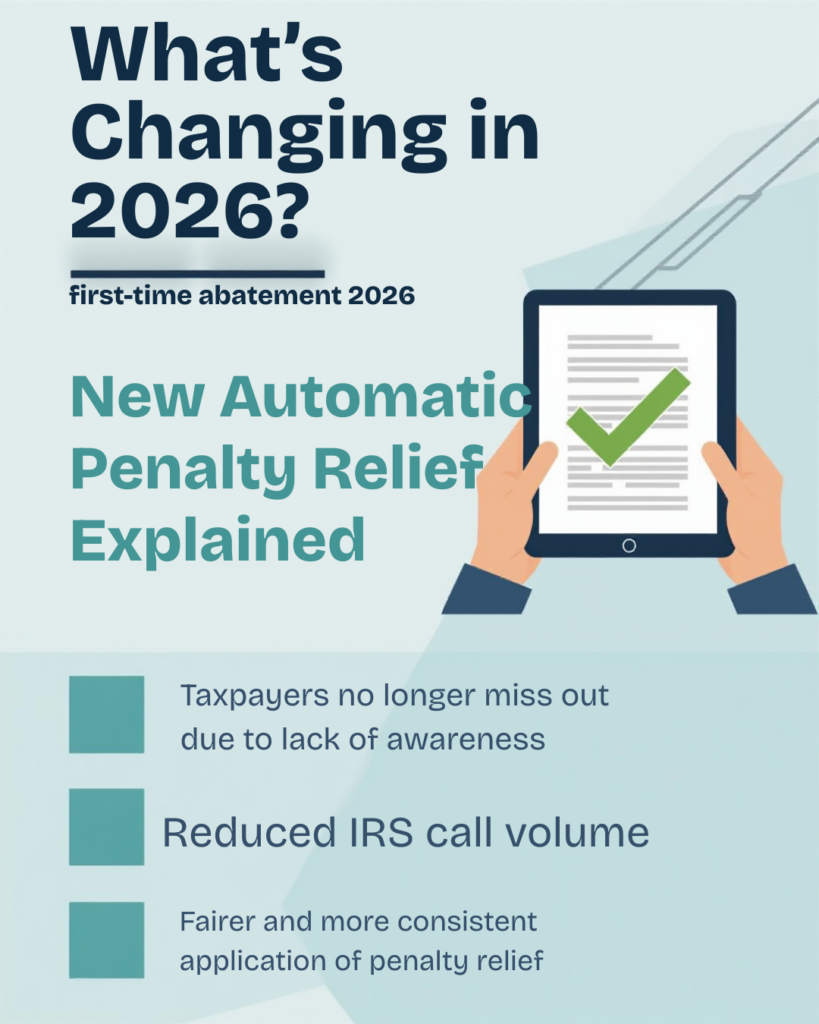

🌟 Benefits of Automatic FTA:

- Taxpayers no longer miss out due to lack of awareness

- Reduced IRS call volume

- Faster processing

- Fairer and more consistent application of penalty relief

🧠 Why First-Time Abatement 2026 Matters

Millions of taxpayers qualify for FTA every year, but only a small percentage receive the waiver. Reasons include:

- Not knowing the program existed

- Difficulty contacting the IRS

- Confusion about eligibility

- Filing delays that complicate penalty removal

With first-time abatement 2026, the IRS aims to eliminate these barriers.

This change especially benefits:

- First-time filers

- Taxpayers facing temporary financial hardship

- Small businesses with payroll deposit issues

- Tax professionals who handle high call volumes during tax season

🛠️ Action Steps for Tax Professionals

Even though first-time abatement 2026 becomes automatic, tax professionals must remain vigilant.

🔍 1. Review Client Accounts for Missed Past FTA Opportunities

Clients may still qualify for relief for earlier years (before 2026).

Tax pros can:

- Obtain Form 2848

- Call the IRS Practitioner Priority Service

- File Form 843 when appropriate

📅 2. Watch for IRS Implementation Guidance

Key details will be published as the IRS finalizes:

- System automation rules

- Exception-handling processes

- How to address cases where automatic FTA is not applied

- Employer deposit penalty workflows

📝 3. Ensure Clients Maintain Filing Compliance

Missing returns automatically disqualify taxpayers from first-time abatement 2026.

Encourage clients to catch up before penalties hit.

💡 4. Understand Prior COVID-Era Penalty Relief Coding

The IRS provided administrative penalty waivers for:

- 2019–2020 late filing

- 2020–2021 failure to pay

These do NOT disqualify taxpayers from first-time abatement 2026, but IRS coding inconsistencies may require manual intervention.

🔚 Final Thoughts

The introduction of first-time abatement 2026 represents a major IRS modernization that brings more fairness and access to penalty relief. Millions of taxpayers will benefit from automatic evaluations rather than needing to request relief through complex processes.

Tax professionals should stay informed, monitor IRS publications, and proactively review client accounts to ensure no qualified taxpayer misses out on penalty relief.

📞 Need Help Navigating IRS Penalties or Compliance?

Veritas Accounting Services is here to support you.

📧 hello@veritasaccountingservices.com

📞 +1 (678) 723-6003 | +91 97255 52243

US Office: 8735 Dunwoody Place – 4549, Atlanta, GA

India Office: C-305, The Imperial Heights, Rajkot

Serving clients in the US, UK, UAE, Singapore, Ireland & Malaysia with expert tax and compliance solutions.

Schedule a FREE Call

Contact us on social