Santa’s 2025 Tax Puzzle: What the New OBBBA Rules Mean for the Man in Red

OBBBA tax rules have reshaped several areas of federal taxation, and as 2025 draws to a close, even hypothetical clients deserve a fresh look. Santa Claus has long been a seasonal favorite for tax professionals exploring complex classification issues, but the introduction of the One Big Beautiful Bill Act adds new relevance to his case.

If Santa were a real client today, OBBBA tax rules would force practitioners to reassess how his activities are categorized, what deductions remain available, and how modern compliance standards apply to unconventional operations.

Is Santa Performing a Service Under OBBBA Tax Rules?

Santa operates a global system that tracks behavior, records outcomes, and determines benefits. From a tax standpoint, that activity begins to resemble a service model. While Santa does not invoice families, tax law focuses less on intent and more on structure and consideration.

Under OBBBA tax rules, the classification of services becomes even more important because new deductions and compliance thresholds hinge on how labor is defined. Santa himself may not receive wages, tips, or overtime, but his workforce certainly does.

The elves’ extended hours during peak production bring OBBBA’s overtime-related deductions into focus. Even in a fictional setting, OBBBA tax rules highlight how compensation structures affect deductions at the entity level.

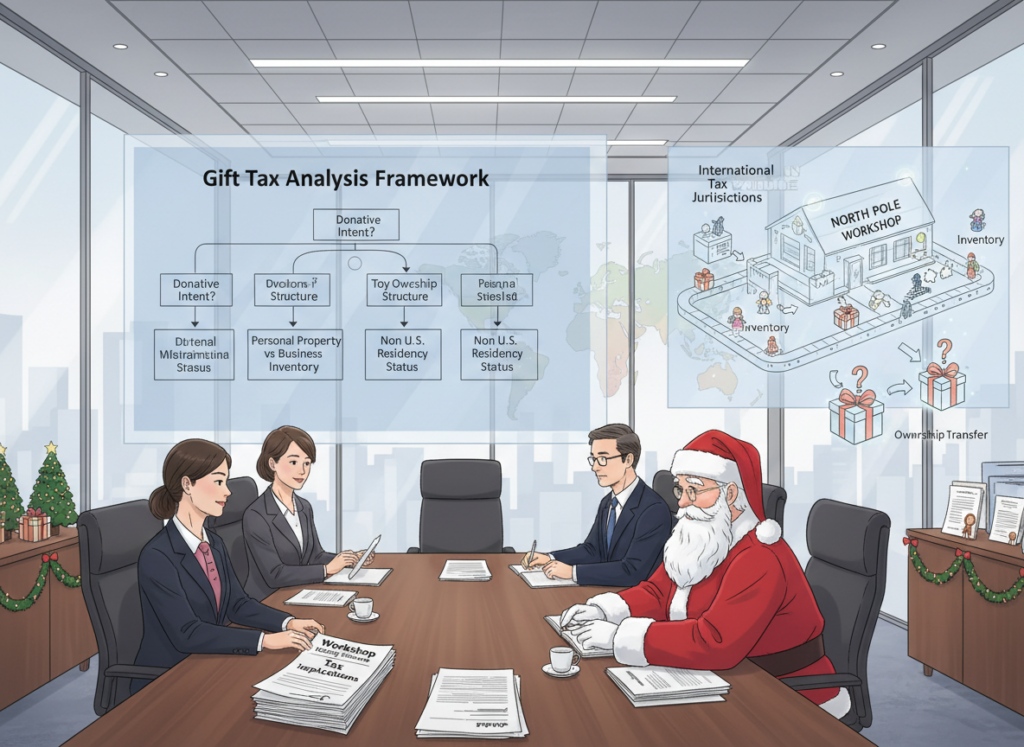

Are Santa’s Deliveries “Gifts” for Tax Purposes?

Gift tax analysis always begins with donative intent, and Santa’s intent appears clear. However, tax professionals must ask deeper questions that OBBBA tax rules do not override but make more visible:

- Who owns the toys before delivery?

- Are the toys personal property or business inventory?

- Does the workshop function as a producing entity?

If the workshop owns the toys, Santa may not be the donor at all. Additionally, Santa’s non-U.S. residency status likely removes him from federal gift tax exposure entirely. Still, OBBBA tax rules reinforce the importance of identifying ownership and residency before assuming tax treatment.

Business or Hobby: Why OBBBA Tax Rules Raise the Stakes

One of the most critical questions under OBBBA tax rules is whether Santa’s workshop operates as a business or a hobby. The distinction matters far more after 2025.

Tax professionals would evaluate:

- Profit motive

- Recordkeeping practices

- Reliance on royalties and licensing income

If the workshop is a business, expenses reduce taxable income directly. If it is a hobby, the outcome is dramatically different.

Under OBBBA tax rules, the suspension of miscellaneous itemized deductions becomes permanent. This means hobby expenses are largely nondeductible going forward. Combined with a larger standard deduction, Santa would gain no tax benefit from hobby-related expenses.

In short:

- Business classification = deductions preserved

- Hobby classification = deductions effectively eliminated

This is exactly why OBBBA tax rules make entity and activity classification more important than ever.

Royalties, Licensing, and Passive Income Considerations

Santa’s image generates significant licensing income through films, merchandise, and branding. These royalties would typically be reported as passive income. However, OBBBA tax rules indirectly affect how these income streams interact with deductions and loss limitations.

If Santa’s workshop is treated as a business, certain expenses could offset active income. If not, royalties may remain taxable without corresponding deductions, reinforcing the importance of proactive planning under OBBBA tax rules.

Does the Sleigh Qualify Under New Deduction Rules?

OBBBA introduced a personal auto loan interest deduction, prompting questions about asset eligibility. Santa’s sleigh, while iconic, does not meet statutory definitions of a qualifying vehicle.

While the answer is clearly no, the example is instructive. OBBBA tax rules demonstrate how narrowly drafted deductions require precise asset classification. Practitioners must evaluate eligibility carefully rather than relying on assumptions.

Santa’s Digital Operations and Cross-Border Issues

Santa’s operation now includes real-time tracking, online engagement, and digital visibility across borders. While not all of this generates income, expanding commercialization could create sourcing and nexus considerations.

Under OBBBA tax rules, digital income streams and licensing arrangements require careful review, particularly when U.S.-source income is involved. Even hypothetical clients illustrate how global operations intersect with modern tax compliance.

Residency and Where Santa Pays Tax

Residency remains the starting point for all tax analysis. Santa’s North Pole residence suggests nonresident alien status. As a result, only U.S.-source income would fall under IRS jurisdiction.

While OBBBA tax rules do not change residency tests, they do influence how deductions, withholding, and reporting apply to nonresident taxpayers. Santa’s situation underscores the continued importance of jurisdictional analysis.

What Tax Professionals Can Learn from Santa’s 2025 Puzzle

Santa’s hypothetical return demonstrates how OBBBA tax rules affect real-world decision-making. Classification, intent, structure, and timing now carry greater consequences than before.

Seasonal examples like this are more than entertainment. They sharpen analytical skills, reinforce compliance fundamentals, and help practitioners stay alert to emerging changes.

Final Takeaway

Santa’s 2025 tax puzzle reminds us that tax law complexity doesn’t disappear just because the facts are unconventional. With OBBBA tax rules reshaping deductions, classifications, and planning strategies, tax professionals must approach every client—real or imagined—with renewed precision.

Understanding how these rules apply today ensures better outcomes tomorrow, long after the sleigh has left the rooftop.

GET IN TOUCH

Schedule a FREE Call

Connect on our Socials!