Critical Tax Planning for Aging Clients: How to Protect Home, Health, and Family Assets

Tax planning for aging clients becomes increasingly important as individuals move into their 80s and 90s and begin facing major life transitions. Many clients from the Silent Generation—generally born between 1928 and 1945—value stability, simplicity, and cautious financial decision-making shaped by decades of experience.

As health needs evolve and family involvement increases, tax planning for aging clients typically centers around three critical areas: decisions about the family home, paying for health and long-term care, and transitioning assets to the next generation. These moments present meaningful opportunities for tax professionals to provide guidance that goes far beyond basic compliance.

Why Tax Planning for Aging Clients Requires Proactive Attention

Unlike younger taxpayers, aging clients often have fixed income streams such as Social Security, pensions, and retirement distributions. At the same time, expenses—particularly medical and care-related costs—tend to rise. Effective tax planning for aging clients focuses on preserving wealth, minimizing avoidable taxes, and reducing uncertainty for both clients and their families.

Waiting until a home is sold or care becomes urgent can limit available options. Year-end planning allows tax professionals to identify opportunities early and avoid costly surprises.

Tax Planning for Aging Clients When Selling a Longtime Home

Many aging clients have lived in the same home for decades and may have no remaining mortgage. While selling the home can provide liquidity or simplify living arrangements, it can also create significant capital gains exposure.

Section 121 of the Internal Revenue Code allows eligible taxpayers to exclude up to $250,000 of gain ($500,000 for married taxpayers filing jointly) on the sale of a primary residence. This exclusion is a cornerstone of tax planning for aging clients.

Key considerations include:

- Time spent in a licensed nursing facility does not automatically disqualify the exclusion, provided the residency test is met.

- Capital improvements—such as accessibility upgrades, bathroom modifications, or structural repairs—can increase basis and reduce taxable gain.

- Homes that were rented at any point may trigger depreciation recapture, which is not excludable.

Your advisory role: Assist clients in reconstructing basis, gathering improvement records, and confirming eligibility for the §121 exclusion. Proper documentation can result in substantial tax savings.

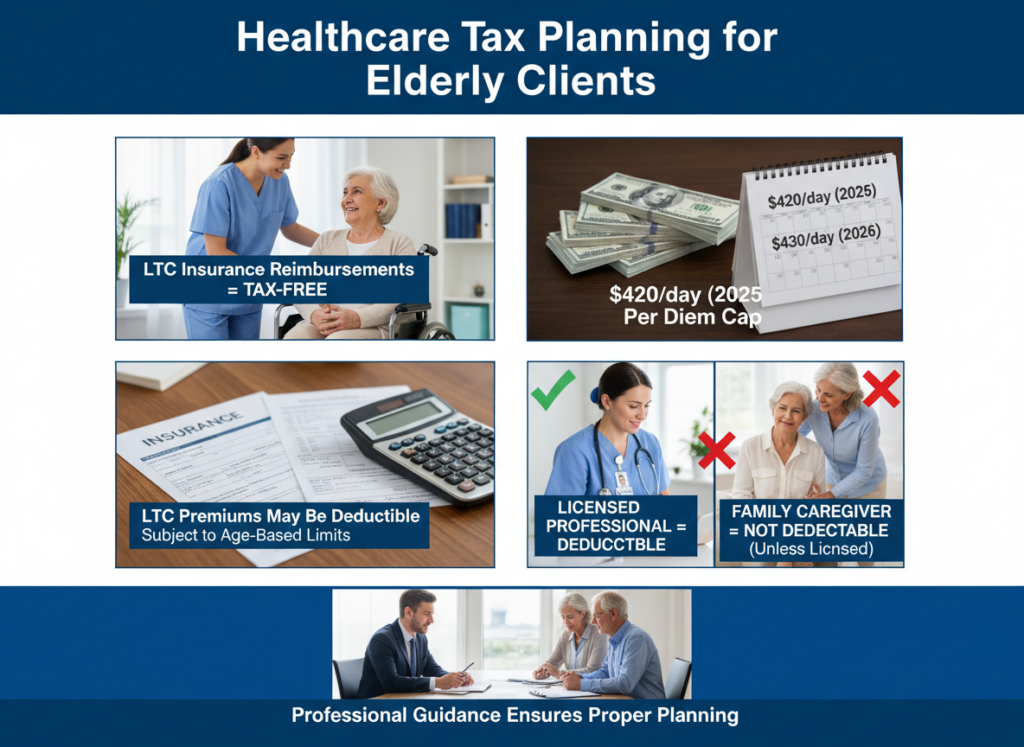

Planning for Health Care and Long-Term Care Costs

Health care is often the most significant financial concern for elderly clients. Tax planning for aging clients must address how care is funded and which expenses qualify for tax benefits.

Important points to review include:

- Qualified long-term care (LTC) insurance reimbursements are generally tax-free.

- Per diem LTC benefits are capped ($420 per day in 2025 and $430 per day in 2026).

- Premiums for qualified LTC insurance may be deductible medical expenses, subject to age-based limits.

- Payments to family caregivers are not deductible medical expenses unless the caregiver is a licensed professional.

Many families assume informal caregiving arrangements provide tax advantages, which is often not the case. Clear explanations help manage expectations and support better planning decisions.

Your advisory role: Review LTC policies, explain reimbursement limits, and help families understand which expenses qualify for deductions.

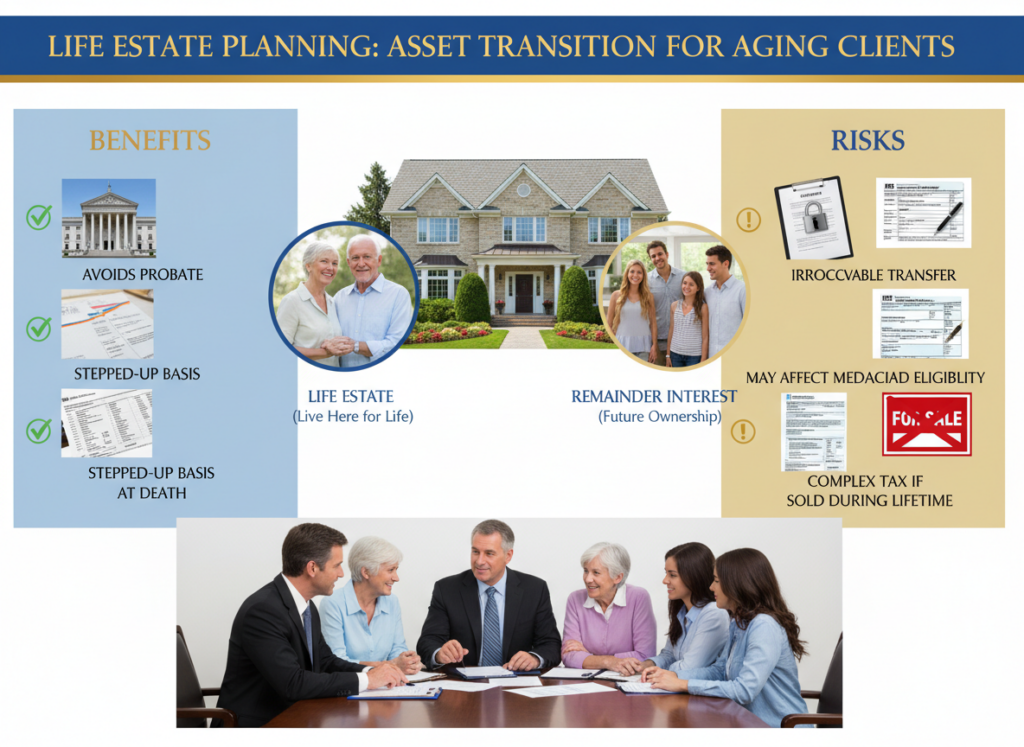

Life Estates and Asset Transfers in Tax Planning for Aging Clients

As clients age, asset transition planning becomes increasingly important. Tax planning for aging clients often includes evaluating whether a life estate is appropriate.

A life estate allows the client to retain the right to live in the home for life while transferring the remainder interest to heirs. Potential benefits include probate avoidance and a stepped-up basis at death.

However, there are notable risks:

- Transfers are generally irrevocable.

- Gift tax reporting may be required.

- Medicaid eligibility may be affected.

- Selling the home during the client’s lifetime can create complex tax consequences.

Your advisory role: Help clients and families weigh the pros and cons, model possible outcomes, and coordinate with estate planning attorneys when appropriate.

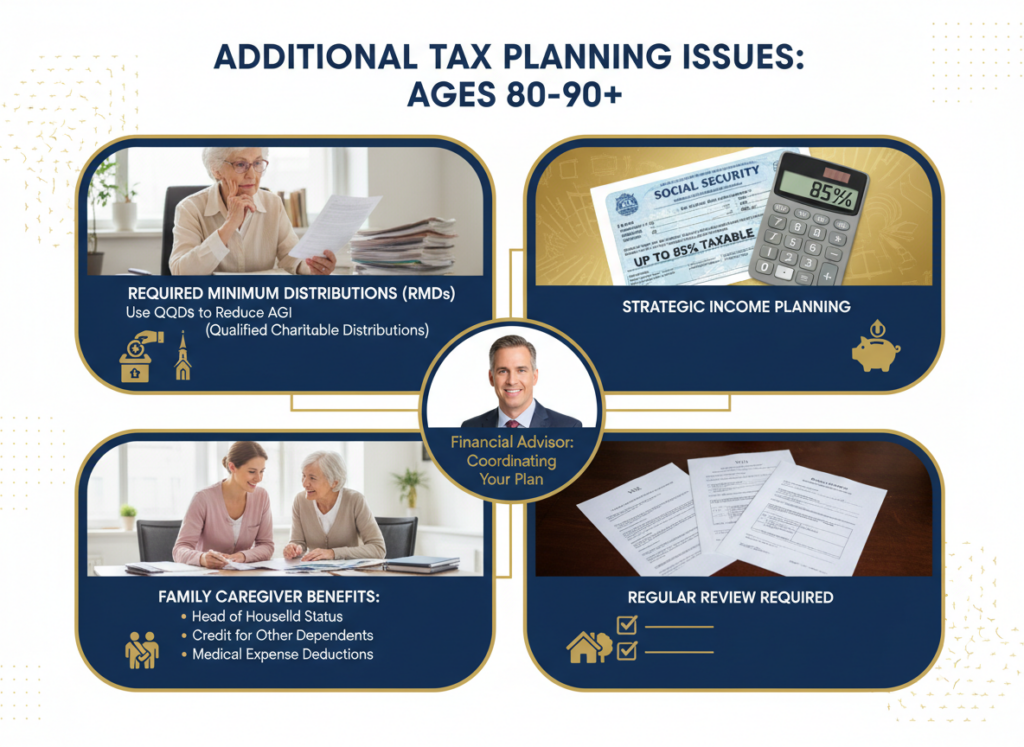

Additional Tax Planning Issues for Clients in Their 80s and 90s

Comprehensive tax planning for aging clients also includes attention to several ongoing tax matters:

Required Minimum Distributions (RMDs)

Even modest retirement accounts can create taxable income. Qualified charitable distributions (QCDs) allow clients to satisfy RMDs while reducing adjusted gross income.

Social Security Taxation

Depending on income levels, up to 85% of Social Security benefits may be taxable. Strategic planning can help manage marginal tax brackets.

Family Caregiver Tax Benefits

Adult children supporting an aging parent may qualify for head of household filing status, the credit for other dependents, or medical expense deductions if requirements are met.

Estate Planning Maintenance

Wills, powers of attorney, health care directives, and beneficiary designations should be reviewed regularly to prevent unintended outcomes.

The Advisory Value of Tax Planning for Aging Clients

For tax professionals, tax planning for aging clients represents a valuable advisory niche. These engagements often involve multiple family members and can lead to long-term, multigenerational relationships.

Action steps you can take:

- Ask proactive questions before health or housing changes occur.

- Encourage organized documentation of medical expenses and home improvements.

- Educate adult children alongside aging parents.

- Position your firm as experienced in senior and family-focused tax planning.

Final Takeaway

Aging clients face pivotal decisions involving their homes, health care, and family assets. Tax planning for aging clients is not just about reducing tax—it’s about providing clarity, protection, and confidence during life’s most important transitions.

By addressing these issues early and thoughtfully, tax professionals can safeguard client wealth, reduce family stress, and deliver meaningful value when it matters most.

GET IN TOUCH

Schedule a FREE Call

Connect on our Socials!