Is an S Corporation the Right Move? Accounting, Taxes, and Costly Mistakes Explained

Choosing the right business structure is one of the most impactful decisions a business owner can make. Many entrepreneurs are drawn to the S corporation because of its potential tax savings, but fewer understand the accounting discipline and compliance rules that come with it. An S corporation can be a smart move—but only when it is set up and maintained correctly.

Without proper S corporation accounting and taxation, the benefits that attract business owners can quickly turn into IRS scrutiny, penalties, and expensive corrections. This guide explains how S corporations work, how they are taxed, what accounting requirements matter most, and the costly mistakes business owners should avoid.

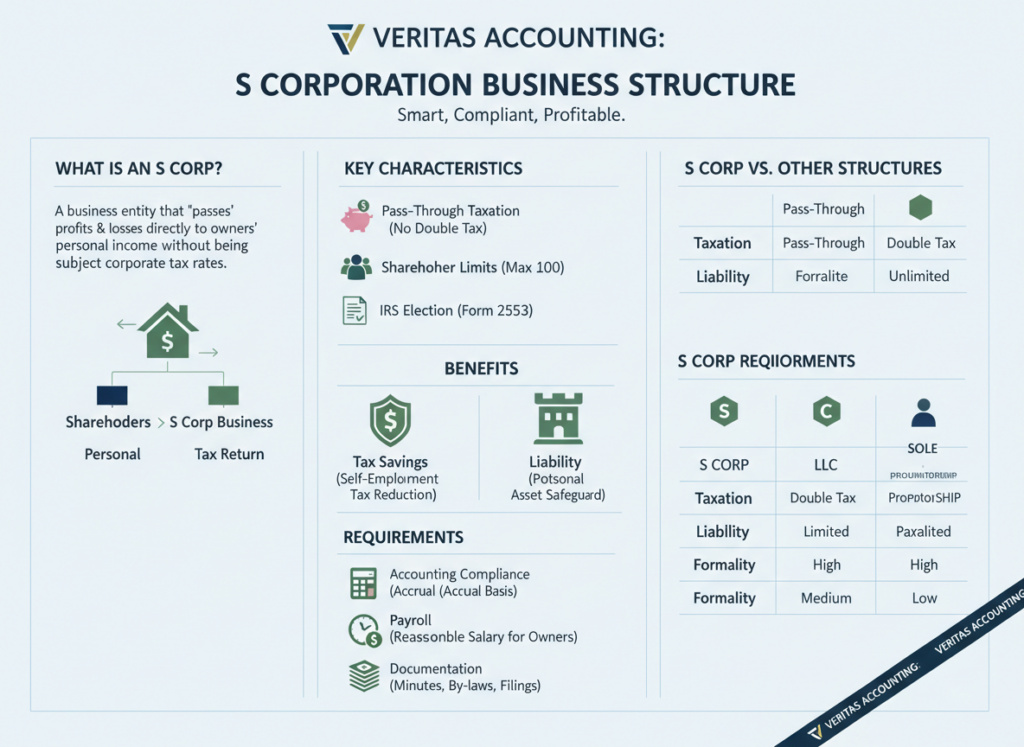

What Is an S Corporation?

An S corporation is a business entity that allows income, losses, deductions, and credits to pass through to shareholders for federal tax purposes. While it is legally formed as a corporation—or an LLC that elects S status—it avoids the double taxation associated with C corporations.

To become an S corporation, a business must file Form 2553 with the IRS and meet eligibility requirements. Once approved, the entity files an annual Form 1120-S, and shareholders report their share of income on their personal returns through Schedule K-1.

Understanding S corporation accounting and taxation starts with recognizing that tax savings depend on strict compliance.

Who Can Own an S Corporation?

The IRS places firm restrictions on who can own an S corporation. Violating these rules can automatically terminate S status.

Key ownership requirements include:

- A maximum of 100 shareholders

- Shareholders must generally be US citizens or resident individuals

- Only one class of stock is permitted

- Certain trusts and estates may qualify, but partnerships and corporations usually do not

Ownership changes should always be reviewed in advance to protect S corporation status.

How S Corporation Taxation Works

Pass-Through Income

An S corporation does not pay federal income tax at the entity level. Instead, profits and losses pass through to shareholders, who report them on their individual tax returns.

One of the most misunderstood aspects of S corporation accounting and taxation is that shareholders pay tax on their share of income even if no cash is distributed. Distributions are not required for income to be taxable.

Reasonable Compensation: A Critical IRS Rule

The IRS requires shareholders who actively work in the business to receive reasonable compensation as wages. This rule exists to prevent owners from avoiding payroll taxes.

Reasonable compensation must:

- Be paid through payroll

- Be subject to Social Security and Medicare taxes

- Reflect industry standards and job duties

Any remaining profits may be distributed and are generally not subject to payroll taxes. However, underpaying salary is one of the most common audit triggers for S corporations. Proper handling of reasonable compensation is central to compliant S corporation accounting and taxation.

Distributions and Shareholder Basis

Distributions are often viewed as “tax-free,” but that is only true up to the shareholder’s basis. Basis is the shareholder’s investment in the company and determines:

- Whether losses are deductible

- Whether distributions are taxable

- Gain or loss upon sale of shares

Accurate basis tracking is essential. Without it, distributions may be incorrectly reported, leading to unexpected taxes.

Accounting Requirements for S Corporations

Choosing an Accounting Method

Most S corporations use either the cash or accrual method of accounting. The selected method must be applied consistently and accurately. Proper S corporation accounting and taxation depends on correct income recognition and expense timing.

Tracking Shareholder Basis Correctly

Shareholder basis increases with:

- Capital contributions

- Pass-through income

It decreases with:

- Distributions

- Pass-through losses

Many S corporations fail to track basis annually, which can create problems even when bookkeeping appears accurate.

Reconciling Book and Tax Differences

Financial accounting income does not always equal taxable income. Differences arise from depreciation methods, limitations on meals, and timing differences. These must be reconciled properly on Form 1120-S to ensure accurate reporting.

Payroll and State Compliance Considerations

S corporations must comply with:

- Federal and state payroll filings

- Unemployment insurance

- Workers’ compensation requirements

- State income or franchise taxes

Some states impose entity-level taxes on S corporations or do not fully follow federal S corp rules. Multi-state operations require careful income sourcing and compliance planning.

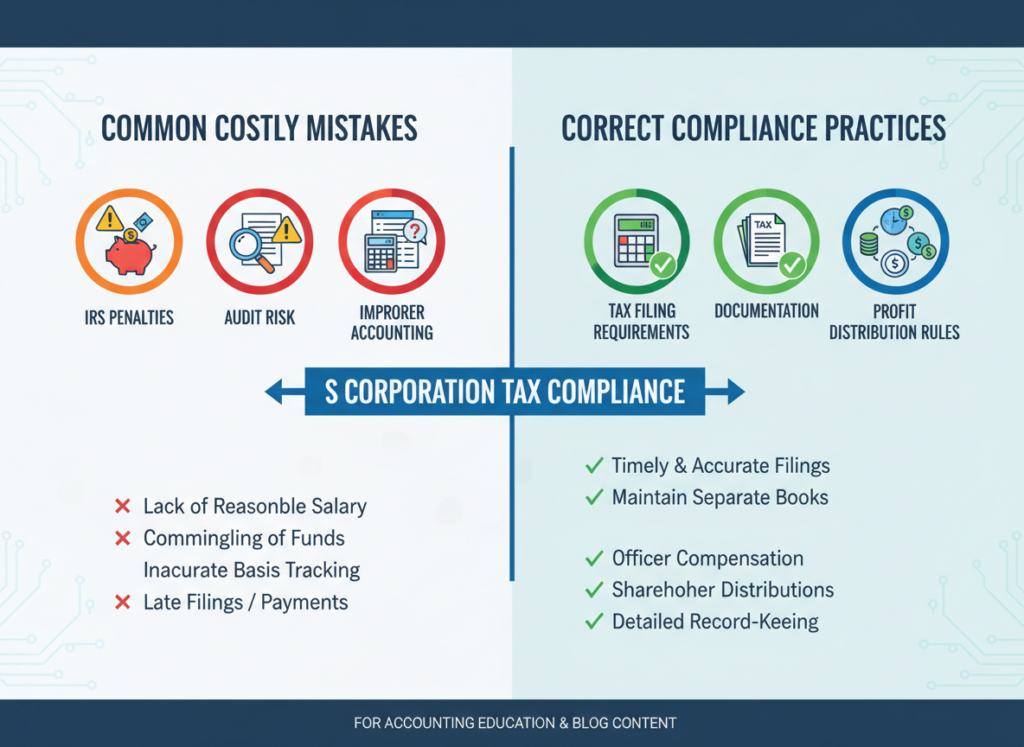

Costly S Corporation Mistakes to Avoid

Many S corporation problems stem from avoidable errors, including:

- Paying distributions without payroll

- Underpaying owner salary

- Missing payroll tax filings

- Violating shareholder eligibility rules

- Ignoring shareholder basis tracking

These mistakes can result in penalties, interest, and loss of S corporation status.

When an S Corporation Makes Sense—and When It Doesn’t

An S corporation is often well-suited for:

- Profitable owner-operated businesses

- Professional service firms

- Consulting and agency businesses

It may not be ideal for:

- Companies seeking outside investors

- Businesses issuing multiple equity classes

- Businesses planning to retain significant earnings

Entity selection should be revisited as income, ownership, and goals evolve.

Tax Planning Opportunities for S Corporations

When managed properly, S corporation accounting and taxation can support:

- Reduced self-employment taxes

- Optimized owner compensation

- Strategic distribution planning

- Retirement contribution strategies

Proactive planning turns compliance into a financial advantage rather than a burden.

Final Thoughts

An S corporation can be a powerful structure—but it is not automatically the right move for every business. The benefits only materialize when accounting, payroll, and tax rules are followed carefully.

Business owners who understand S corporation accounting and taxation and work with experienced professionals are far more likely to capture tax savings while avoiding costly mistakes. When handled correctly, an S corporation becomes not just a tax strategy, but a stable foundation for long-term growth.

GET IN TOUCH

Schedule a FREE Call

Connect on our Socials!