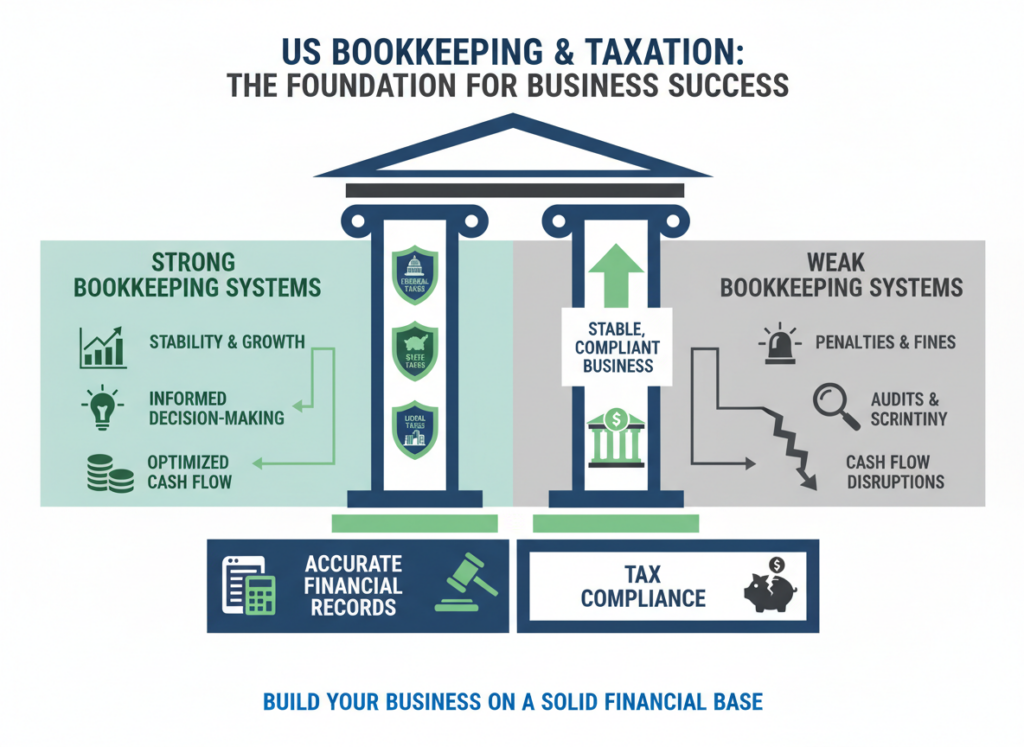

US Bookkeeping and Taxation: What Businesses Must Get Right

US bookkeeping and taxation are the foundation of every compliant and financially stable business operating in the United States. Regardless of size or industry, businesses are expected to maintain accurate financial records and meet federal, state, and local tax obligations on time. When bookkeeping systems are weak or tax rules are misunderstood, the consequences can include penalties, audits, cash flow disruptions, and poor financial decisions.

Understanding how US bookkeeping and taxation work together allows business owners to stay compliant, plan effectively, and make informed decisions throughout the year—not just at tax time.

Why US Bookkeeping and Taxation Are Closely Connected

Bookkeeping and taxation are often discussed separately, but in practice they are inseparable. Every tax return filed with the IRS is built on bookkeeping data. If transactions are recorded incorrectly or not supported with documentation, tax filings will also be inaccurate.

Strong US bookkeeping and taxation practices ensure that income is reported correctly, deductions are supported, and tax liabilities are calculated accurately. Businesses that invest in clean bookkeeping experience fewer surprises and smoother interactions with tax authorities.

Core Bookkeeping Requirements for US Businesses

Accurate recordkeeping is the backbone of US bookkeeping and taxation. At a minimum, businesses must maintain:

- A structured chart of accounts

- Detailed records of income and expenses

- Bank and credit card reconciliations

- Accounts receivable and payable tracking

- Supporting documents such as invoices and receipts

These records support financial statements and form the basis for all tax filings. Without disciplined bookkeeping, even well-intentioned businesses can fall out of compliance.

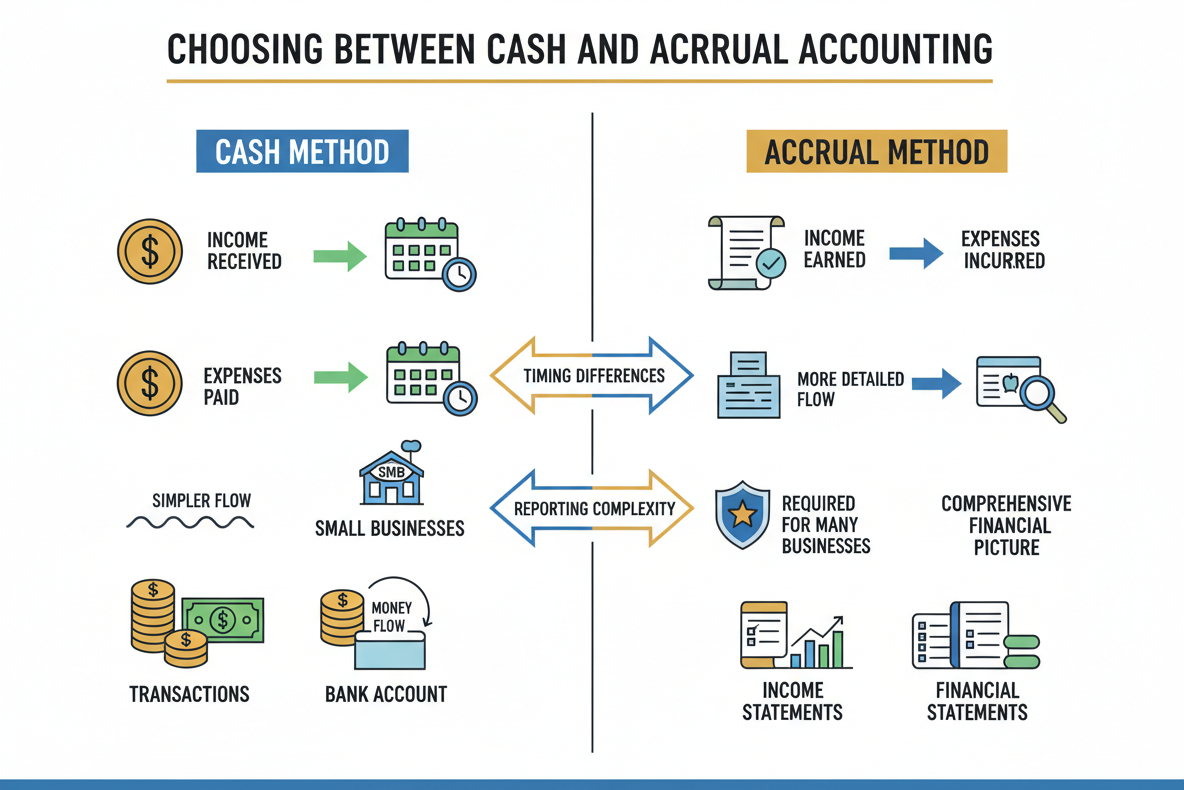

The accounting method used directly impacts US bookkeeping and taxation. Most small businesses choose between cash and accrual accounting.

- Cash method: Income is recorded when received, and expenses when paid. This method is simpler and often used by small businesses.

- Accrual method: Income and expenses are recorded when earned or incurred, regardless of cash movement. This method provides a more accurate financial picture and is required for many businesses.

Once selected, the accounting method must be applied consistently and may require IRS approval to change.

Federal Tax Responsibilities Businesses Must Manage

Federal tax compliance is a critical component of US bookkeeping and taxation. Depending on the business structure, obligations may include:

- Income tax (corporate or pass-through)

- Self-employment tax

- Payroll taxes (Social Security and Medicare)

- Federal unemployment tax (FUTA)

Accurate bookkeeping ensures these taxes are calculated correctly and paid on time. Missed or underpaid federal taxes can quickly lead to penalties and interest.

State and Local Tax Compliance

In addition to federal obligations, US bookkeeping and taxation include state and local requirements that vary by jurisdiction. These may involve:

- State income or franchise taxes

- Sales and use tax

- State payroll taxes

- Local business taxes or licenses

Businesses operating in multiple states must monitor nexus rules and ensure proper registration and filing in each applicable state.

Sales Tax Tracking and Reporting

Sales tax compliance has become more complex due to economic nexus rules. Businesses must track where they have sales tax obligations and accurately record taxable and exempt transactions.

Proper US bookkeeping and taxation practices include:

- Separating taxable and non-taxable sales

- Tracking collected sales tax separately

- Reconciling sales tax payable accounts

Errors in sales tax reporting can result in assessments, penalties, and costly audits.

Payroll Bookkeeping and Tax Compliance

Payroll is one of the highest-risk areas in US bookkeeping and taxation. Employers must calculate wages accurately, withhold the correct taxes, and remit payments to federal and state agencies.

Key payroll tax obligations include:

- Federal income tax withholding

- Social Security and Medicare taxes

- State income tax withholding

- Quarterly and annual payroll filings

Worker misclassification is a common compliance issue that can trigger audits and penalties.

Expense Classification and Deductibility

Correct expense categorization plays a major role in US bookkeeping and taxation. While many business expenses are deductible, some are subject to limits or special rules.

Common areas requiring attention include:

- Meals and entertainment expenses

- Vehicle and travel costs

- Home office deductions

- Asset capitalization and depreciation

Well-maintained books allow businesses to claim legitimate deductions while avoiding aggressive positions that could raise red flags.

Record Retention and IRS Documentation Standards

The IRS requires businesses to retain financial records for several years. Strong US bookkeeping and taxation practices include maintaining:

- Bank statements and reconciliations

- Receipts and invoices

- Payroll records

- Tax returns and supporting schedules

Proper documentation supports tax positions and simplifies responses to IRS inquiries or audits.

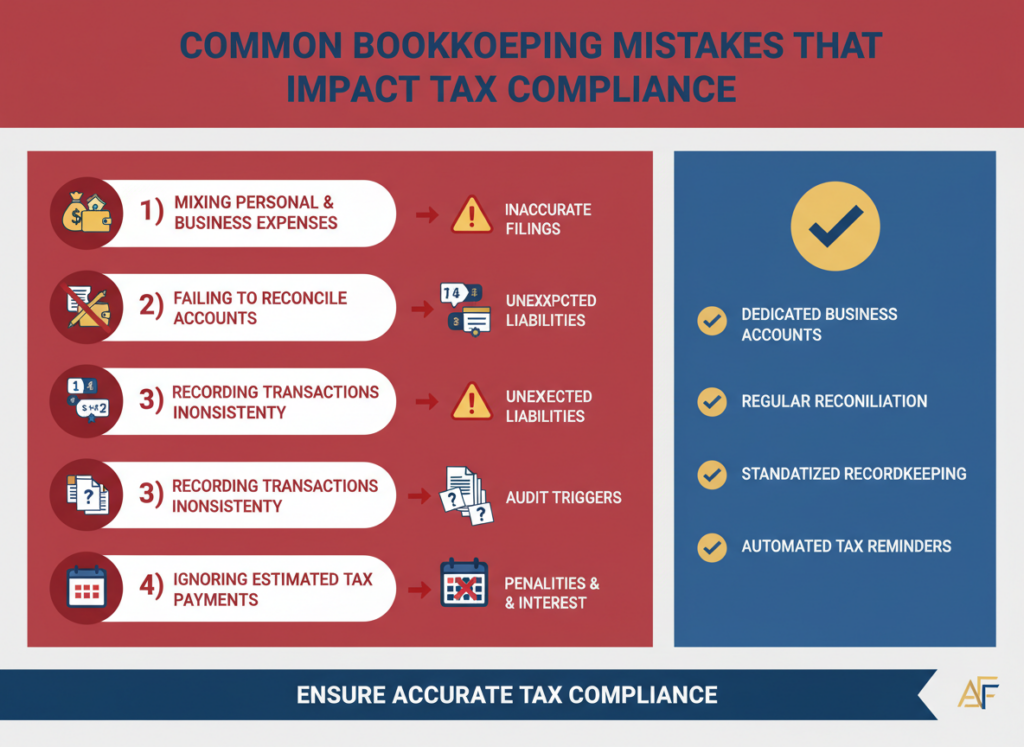

Common Bookkeeping Mistakes That Impact Tax Compliance

Several recurring errors undermine US bookkeeping and taxation, including:

- Mixing personal and business expenses

- Failing to reconcile accounts regularly

- Recording transactions inconsistently

- Ignoring estimated tax payments

These mistakes often result in inaccurate tax filings and unexpected liabilities.

The Value of Professional Bookkeeping and Tax Support

Many businesses rely on professional services to manage US bookkeeping and taxation effectively. Experienced professionals help ensure accuracy, consistency, and compliance while identifying opportunities for tax efficiency.

Outsourcing or hiring qualified support allows business owners to focus on growth while reducing compliance risks.

Year-End Bookkeeping and Tax Preparation

Year-end is a critical period for US bookkeeping and taxation. Closing the books properly ensures that financial statements are accurate before tax returns are prepared.

Key year-end tasks include:

- Reconciling all accounts

- Reviewing income and expense classifications

- Confirming depreciation and asset records

- Preparing tax-ready financial statements

Strong year-end processes reduce stress and improve tax outcomes.

Final Takeaway

US bookkeeping and taxation are not just compliance requirements—they are essential tools for financial clarity and business success. Accurate bookkeeping supports reliable tax reporting, while proactive tax planning depends on clean financial data.

Businesses that get the fundamentals right reduce risk, improve decision-making, and stay compliant with IRS and state regulations. By prioritizing strong bookkeeping systems and understanding tax obligations, companies can operate with confidence and build a solid foundation for long-term growth.

GET IN TOUCH

Schedule a FREE Call

Connect on our Socials!