Each tax season, questions about refund timing surge—especially from taxpayers who rely on refundable credits like the Earned Income Tax Credit (EITC) and the Additional Child Tax Credit (ACTC). These refunds often represent a meaningful source of financial support, and delays can cause understandable concern.

For the 2026 filing season, the IRS has set clear expectations around when EITC and ACTC refunds will be released. While the rules themselves are not new, understanding the timing—and the reasons behind it—can help taxpayers plan better and reduce frustration. Knowing the three critical IRS dates makes all the difference.

Why EITC and ACTC Refunds Follow a Different Timeline

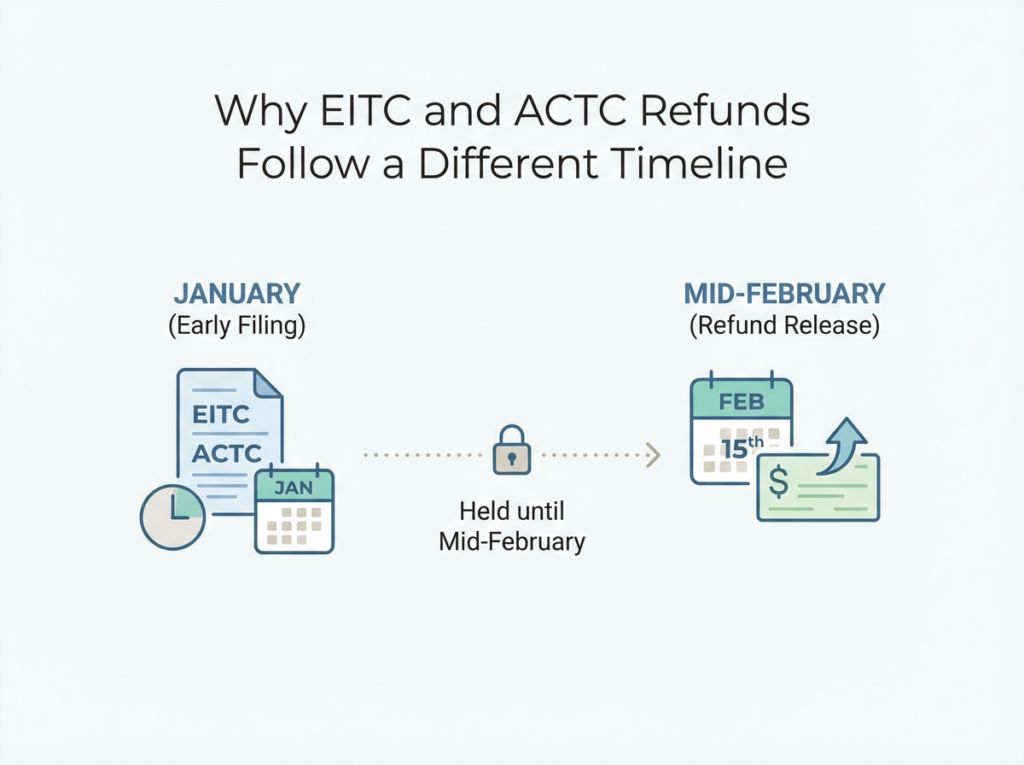

Refunds that include the EITC or ACTC are subject to special rules under the Protecting Americans from Tax Hikes (PATH) Act. The PATH Act requires the IRS to hold these refunds until mid-February, regardless of how early the return is filed.

The goal is fraud prevention. By delaying refunds, the IRS has additional time to verify:

Income reported on Forms W-2 and 1099

Withholding amounts

Dependent and qualifying child information

Although the delay can be frustrating, it has become a predictable and built-in part of the filing season.

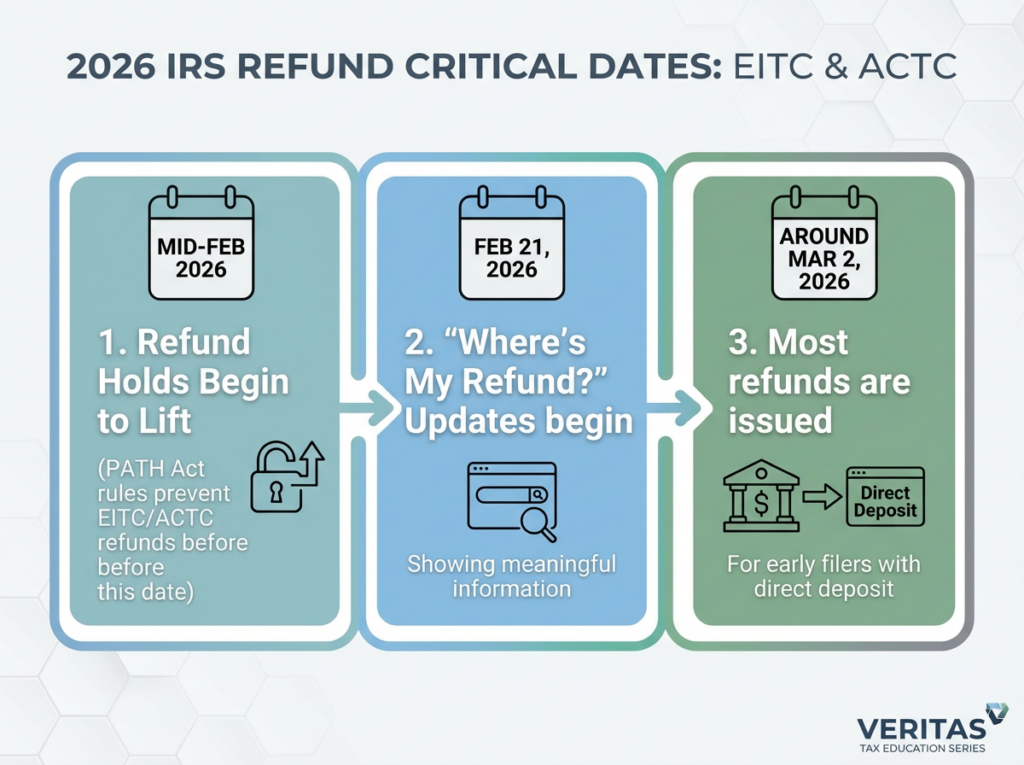

📅 The 3 Critical IRS Dates to Know for 2026

1. Mid-February 2026: Refund Holds Begin to Lift

Under the PATH Act, the IRS cannot issue refunds that include EITC or ACTC before mid-February. This rule applies even if:

The return is filed on the first day of the season

The return is accurate and complete

Direct deposit is selected

This means taxpayers claiming these credits should not expect refunds in January or early February.

2. February 21, 2026: “Where’s My Refund?” Updates

By around February 21, 2026, the IRS expects its “Where’s My Refund?” tool to begin showing meaningful updates for most EITC and ACTC filers.

Once a return is approved, the tool will display a projected deposit date, which helps set realistic expectations. Tax professionals should encourage clients to rely on this tool rather than daily follow-ups.

3. Around March 2, 2026: Most Refunds Are Issued

The IRS has stated that most taxpayers who file early, claim EITC or ACTC, and choose direct deposit should receive refunds around March 2, 2026, assuming no issues with the return.

Some refunds may arrive slightly earlier or later depending on:

Bank or debit card processing times

Weekends or holidays

Internal financial institution policies

Paper-filed returns and refunds issued by check will take longer.

How Refund Delivery Method Affects Timing

Choosing electronic filing with direct deposit remains the fastest and most reliable way to receive a refund. Taxpayers who opt for:

Paper filing

Mailed checks

should expect additional delays beyond the March 2 target window.

Even when the IRS releases funds, the final deposit timing depends on how quickly the taxpayer’s financial institution processes incoming payments.

Common Issues That Can Delay EITC or ACTC Refunds

Even with clear refund dates, some returns are delayed due to errors or mismatches. Common triggers include:

Incorrect Social Security numbers for dependents

Income that does not match Forms W-2 or 1099-NEC

Errors on Schedule 8812 (Credits for Qualifying Children and Other Dependents)

Missing or incomplete documentation

Because refundable credits are a major IRS enforcement focus, these returns receive additional scrutiny.

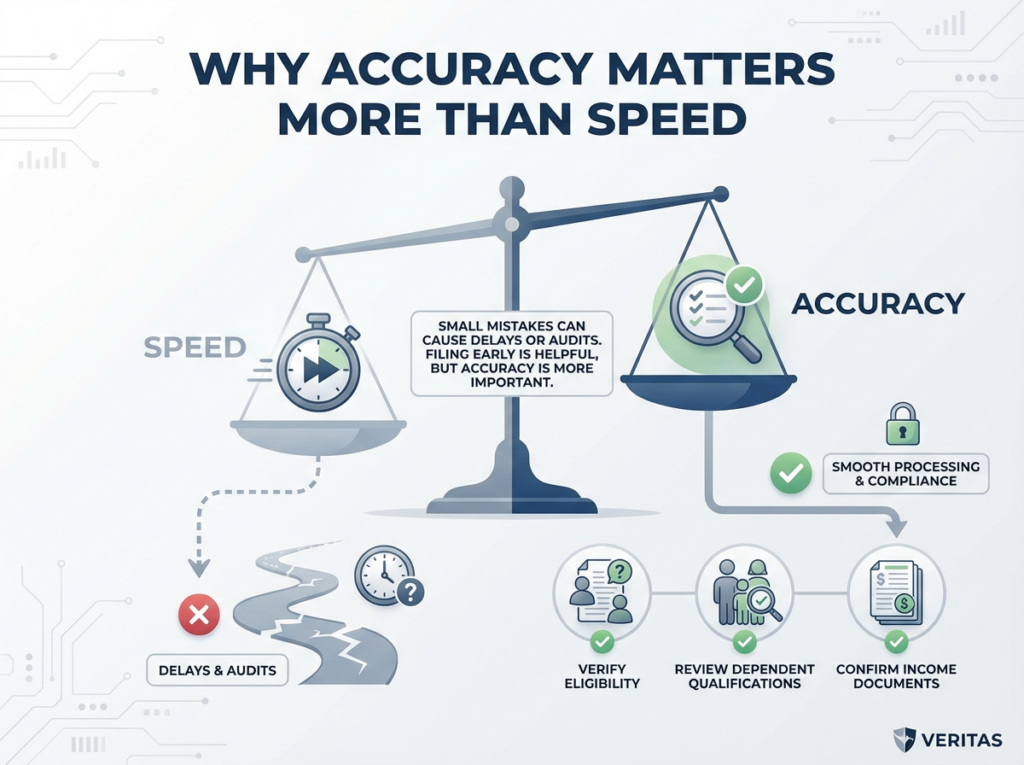

Why Accuracy Matters More Than Speed

Filing early is helpful, but accuracy matters more than speed when claiming EITC or ACTC. Tax professionals must meet strict due diligence requirements, and even small mistakes can cause processing delays or correspondence audits.

Verifying eligibility, reviewing dependent qualifications, and confirming income documents before filing helps prevent avoidable delays and protects both the taxpayer and the preparer.

Helping Clients Plan Around Refund Timing

For many families, EITC and ACTC refunds are used to:

Pay down debt

Catch up on household expenses

Build emergency savings

Clear communication about refund timing helps clients plan responsibly and reduces pressure to use high-cost refund advance products.

Setting expectations early—especially explaining that March refunds are normal, not delayed—can significantly reduce anxiety during filing season.

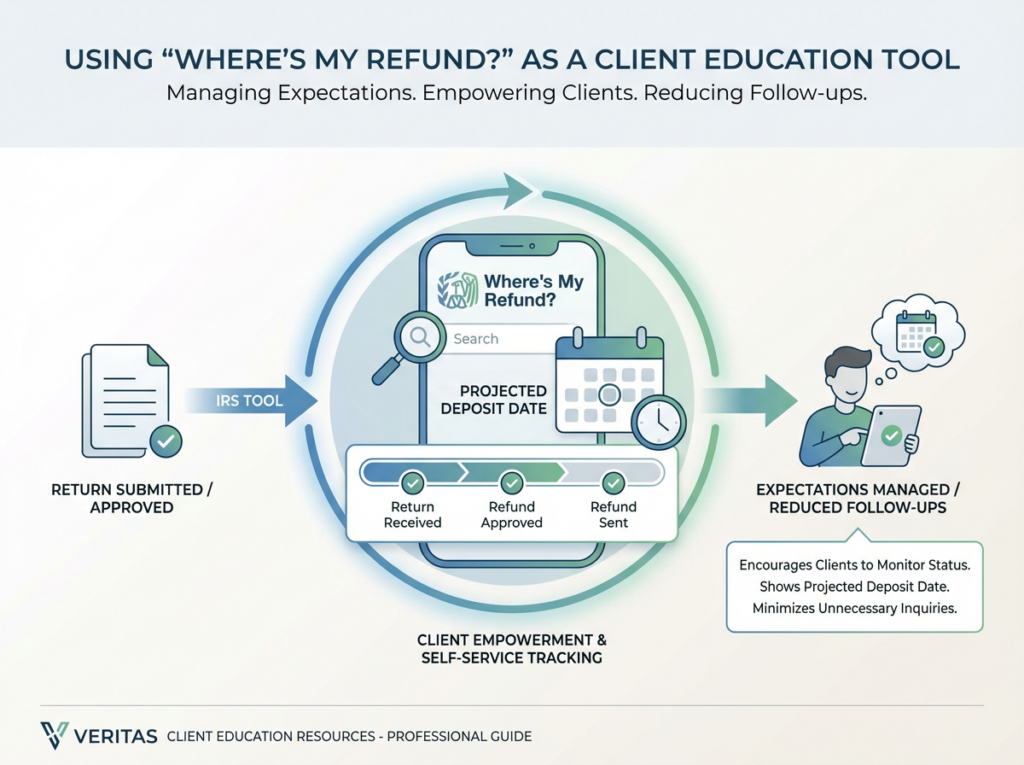

Using “Where’s My Refund?” as a Client Education Tool

The IRS “Where’s My Refund?” tool remains one of the most effective ways to manage expectations. Once a return shows as approved, the projected deposit date provides a reliable window for when funds should arrive.

Encouraging clients to use this tool empowers them and reduces unnecessary follow-ups.

A Timely Reminder for Tax Professionals

As refund-related questions increase, proactive education becomes a value-add. Explaining:

The PATH Act delay

The March 2 target date

Common causes of delays

helps build trust and reinforces confidence in your practice.

For professionals looking to deepen their technical understanding, continued education on child-related credits remains essential—especially as enforcement around refundable credits continues to evolve.

Final Takeaway

Waiting for an EITC or ACTC refund can feel stressful, but the timeline for 2026 is clear and predictable. Understanding the three critical IRS dates—mid-February holds, late-February status updates, and early-March deposits—helps taxpayers plan with confidence.

With accurate filing, electronic submission, and direct deposit, most refunds will arrive right on schedule. And with the right guidance, what feels like a delay becomes simply part of a system designed to protect taxpayers and the integrity of the tax process.

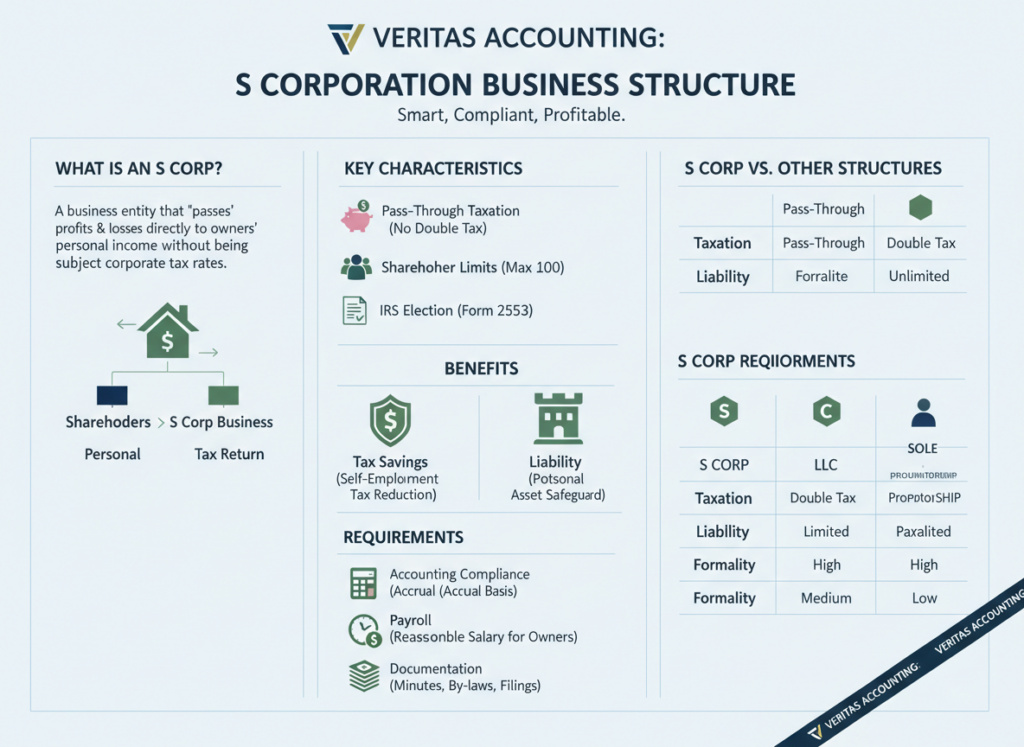

Choosing the right business structure is one of the most impactful decisions a business owner can make. Many entrepreneurs are drawn to the S corporation because of its potential tax savings, but fewer understand the accounting discipline and compliance rules that come with it. An S corporation can be a smart move—but only when it is set up and maintained correctly.

Without proper S corporation accounting and taxation, the benefits that attract business owners can quickly turn into IRS scrutiny, penalties, and expensive corrections. This guide explains how S corporations work, how they are taxed, what accounting requirements matter most, and the costly mistakes business owners should avoid.

What Is an S Corporation?

An S corporation is a business entity that allows income, losses, deductions, and credits to pass through to shareholders for federal tax purposes. While it is legally formed as a corporation—or an LLC that elects S status—it avoids the double taxation associated with C corporations.

To become an S corporation, a business must file Form 2553 with the IRS and meet eligibility requirements. Once approved, the entity files an annual Form 1120-S, and shareholders report their share of income on their personal returns through Schedule K-1.

Understanding S corporation accounting and taxation starts with recognizing that tax savings depend on strict compliance.

Who Can Own an S Corporation?

The IRS places firm restrictions on who can own an S corporation. Violating these rules can automatically terminate S status.

Shareholders must generally be US citizens or resident individuals

Only one class of stock is permitted

Certain trusts and estates may qualify, but partnerships and corporations usually do not

Ownership changes should always be reviewed in advance to protect S corporation status.

How S Corporation Taxation Works

Pass-Through Income

An S corporation does not pay federal income tax at the entity level. Instead, profits and losses pass through to shareholders, who report them on their individual tax returns.

One of the most misunderstood aspects of S corporation accounting and taxation is that shareholders pay tax on their share of income even if no cash is distributed. Distributions are not required for income to be taxable.

Reasonable Compensation: A Critical IRS Rule

The IRS requires shareholders who actively work in the business to receive reasonable compensation as wages. This rule exists to prevent owners from avoiding payroll taxes.

Reasonable compensation must:

Be paid through payroll

Be subject to Social Security and Medicare taxes

Reflect industry standards and job duties

Any remaining profits may be distributed and are generally not subject to payroll taxes. However, underpaying salary is one of the most common audit triggers for S corporations. Proper handling of reasonable compensation is central to compliant S corporation accounting and taxation.

Distributions and Shareholder Basis

Distributions are often viewed as “tax-free,” but that is only true up to the shareholder’s basis. Basis is the shareholder’s investment in the company and determines:

Whether losses are deductible

Whether distributions are taxable

Gain or loss upon sale of shares

Accurate basis tracking is essential. Without it, distributions may be incorrectly reported, leading to unexpected taxes.

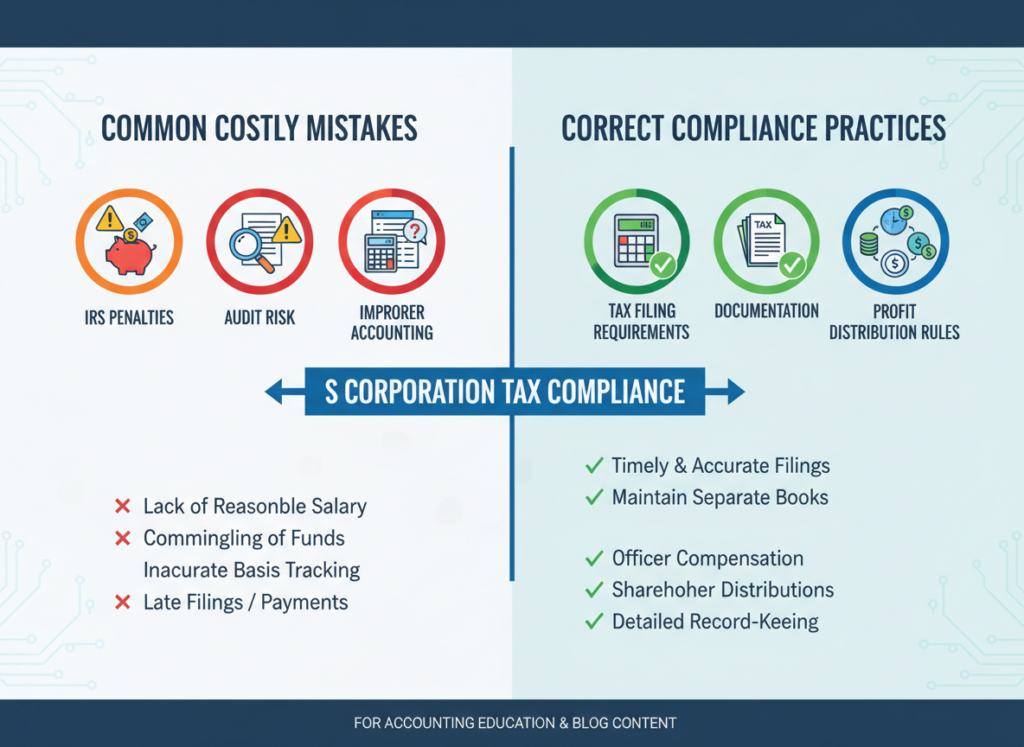

Accounting Requirements for S Corporations

Choosing an Accounting Method

Most S corporations use either the cash or accrual method of accounting. The selected method must be applied consistently and accurately. Proper S corporation accounting and taxation depends on correct income recognition and expense timing.

Tracking Shareholder Basis Correctly

Shareholder basis increases with:

Capital contributions

Pass-through income

It decreases with:

Distributions

Pass-through losses

Many S corporations fail to track basis annually, which can create problems even when bookkeeping appears accurate.

Reconciling Book and Tax Differences

Financial accounting income does not always equal taxable income. Differences arise from depreciation methods, limitations on meals, and timing differences. These must be reconciled properly on Form 1120-S to ensure accurate reporting.

Payroll and State Compliance Considerations

S corporations must comply with:

Federal and state payroll filings

Unemployment insurance

Workers’ compensation requirements

State income or franchise taxes

Some states impose entity-level taxes on S corporations or do not fully follow federal S corp rules. Multi-state operations require careful income sourcing and compliance planning.

Costly S Corporation Mistakes to Avoid

Many S corporation problems stem from avoidable errors, including:

Paying distributions without payroll

Underpaying owner salary

Missing payroll tax filings

Violating shareholder eligibility rules

Ignoring shareholder basis tracking

These mistakes can result in penalties, interest, and loss of S corporation status.

When an S Corporation Makes Sense—and When It Doesn’t

Businesses planning to retain significant earnings

Entity selection should be revisited as income, ownership, and goals evolve.

Tax Planning Opportunities for S Corporations

When managed properly, S corporation accounting and taxation can support:

Reduced self-employment taxes

Optimized owner compensation

Strategic distribution planning

Retirement contribution strategies

Proactive planning turns compliance into a financial advantage rather than a burden.

Final Thoughts

An S corporation can be a powerful structure—but it is not automatically the right move for every business. The benefits only materialize when accounting, payroll, and tax rules are followed carefully.

Business owners who understand S corporation accounting and taxation and work with experienced professionals are far more likely to capture tax savings while avoiding costly mistakes. When handled correctly, an S corporation becomes not just a tax strategy, but a stable foundation for long-term growth.

Tax planning for aging clients becomes increasingly important as individuals move into their 80s and 90s and begin facing major life transitions. Many clients from the Silent Generation—generally born between 1928 and 1945—value stability, simplicity, and cautious financial decision-making shaped by decades of experience.

As health needs evolve and family involvement increases, tax planning for aging clients typically centers around three critical areas: decisions about the family home, paying for health and long-term care, and transitioning assets to the next generation. These moments present meaningful opportunities for tax professionals to provide guidance that goes far beyond basic compliance.

Why Tax Planning for Aging Clients Requires Proactive Attention

Unlike younger taxpayers, aging clients often have fixed income streams such as Social Security, pensions, and retirement distributions. At the same time, expenses—particularly medical and care-related costs—tend to rise. Effective tax planning for aging clients focuses on preserving wealth, minimizing avoidable taxes, and reducing uncertainty for both clients and their families.

Waiting until a home is sold or care becomes urgent can limit available options. Year-end planning allows tax professionals to identify opportunities early and avoid costly surprises.

Tax Planning for Aging Clients When Selling a Longtime Home

Many aging clients have lived in the same home for decades and may have no remaining mortgage. While selling the home can provide liquidity or simplify living arrangements, it can also create significant capital gains exposure.

Section 121 of the Internal Revenue Code allows eligible taxpayers to exclude up to $250,000 of gain ($500,000 for married taxpayers filing jointly) on the sale of a primary residence. This exclusion is a cornerstone of tax planning for aging clients.

Key considerations include:

Time spent in a licensed nursing facility does not automatically disqualify the exclusion, provided the residency test is met.

Capital improvements—such as accessibility upgrades, bathroom modifications, or structural repairs—can increase basis and reduce taxable gain.

Homes that were rented at any point may trigger depreciation recapture, which is not excludable.

Your advisory role: Assist clients in reconstructing basis, gathering improvement records, and confirming eligibility for the §121 exclusion. Proper documentation can result in substantial tax savings.

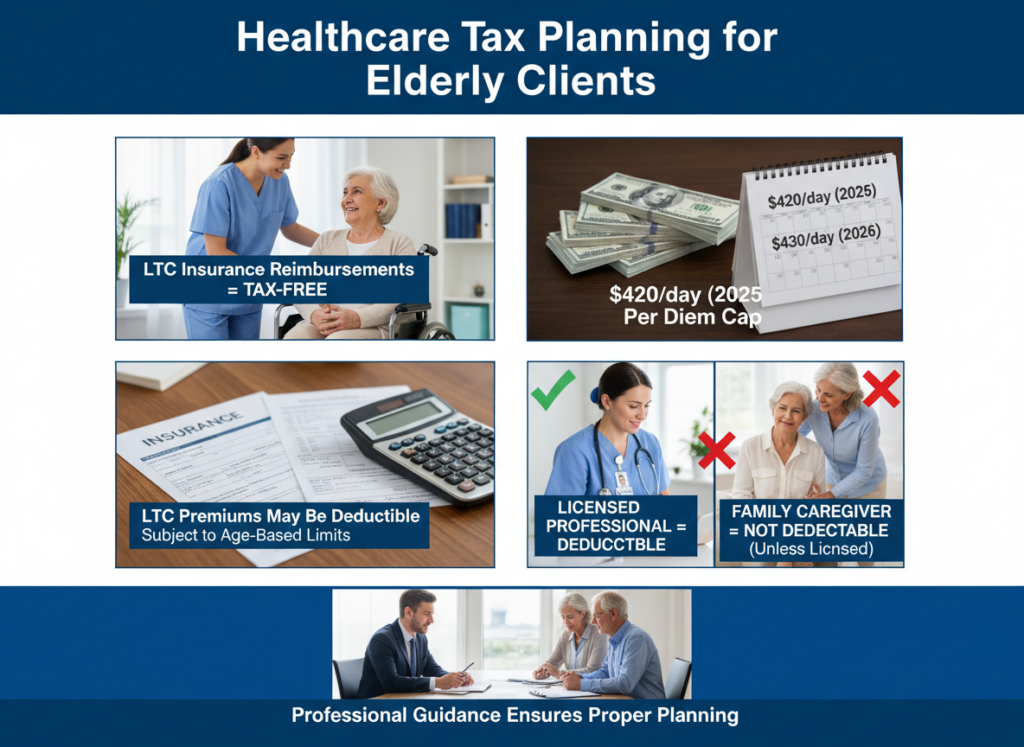

Planning for Health Care and Long-Term Care Costs

Health care is often the most significant financial concern for elderly clients. Tax planning for aging clients must address how care is funded and which expenses qualify for tax benefits.

Important points to review include:

Qualified long-term care (LTC) insurance reimbursements are generally tax-free.

Per diem LTC benefits are capped ($420 per day in 2025 and $430 per day in 2026).

Premiums for qualified LTC insurance may be deductible medical expenses, subject to age-based limits.

Payments to family caregivers are not deductible medical expenses unless the caregiver is a licensed professional.

Many families assume informal caregiving arrangements provide tax advantages, which is often not the case. Clear explanations help manage expectations and support better planning decisions.

Your advisory role: Review LTC policies, explain reimbursement limits, and help families understand which expenses qualify for deductions.

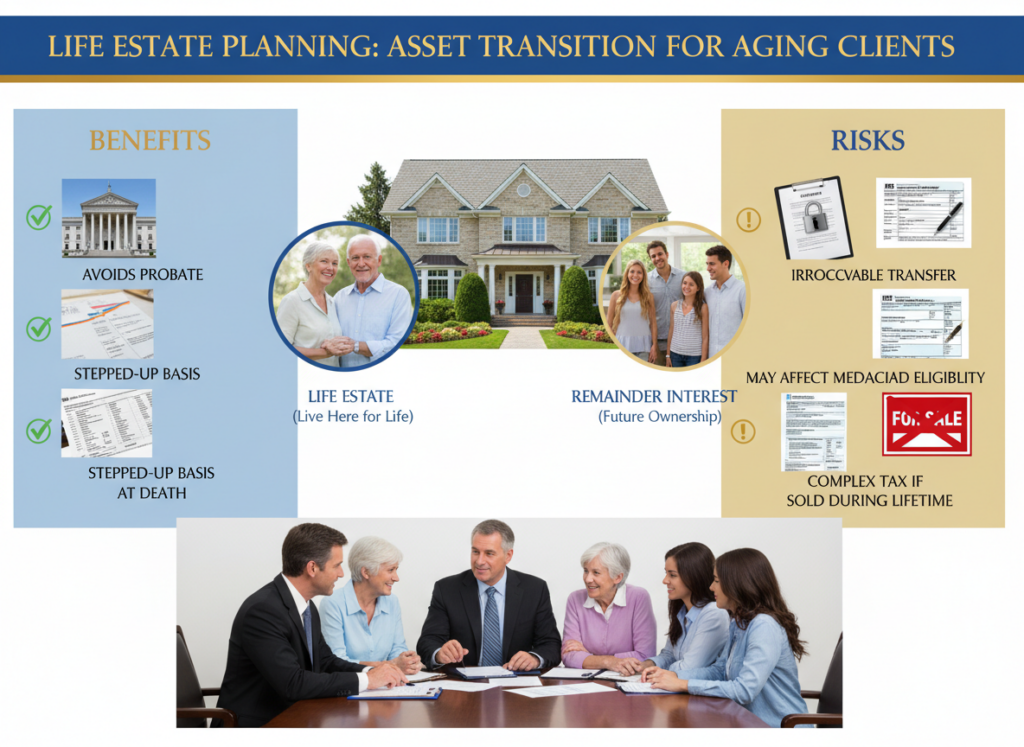

Life Estates and Asset Transfers in Tax Planning for Aging Clients

As clients age, asset transition planning becomes increasingly important. Tax planning for aging clients often includes evaluating whether a life estate is appropriate.

A life estate allows the client to retain the right to live in the home for life while transferring the remainder interest to heirs. Potential benefits include probate avoidance and a stepped-up basis at death.

However, there are notable risks:

Transfers are generally irrevocable.

Gift tax reporting may be required.

Medicaid eligibility may be affected.

Selling the home during the client’s lifetime can create complex tax consequences.

Your advisory role: Help clients and families weigh the pros and cons, model possible outcomes, and coordinate with estate planning attorneys when appropriate.

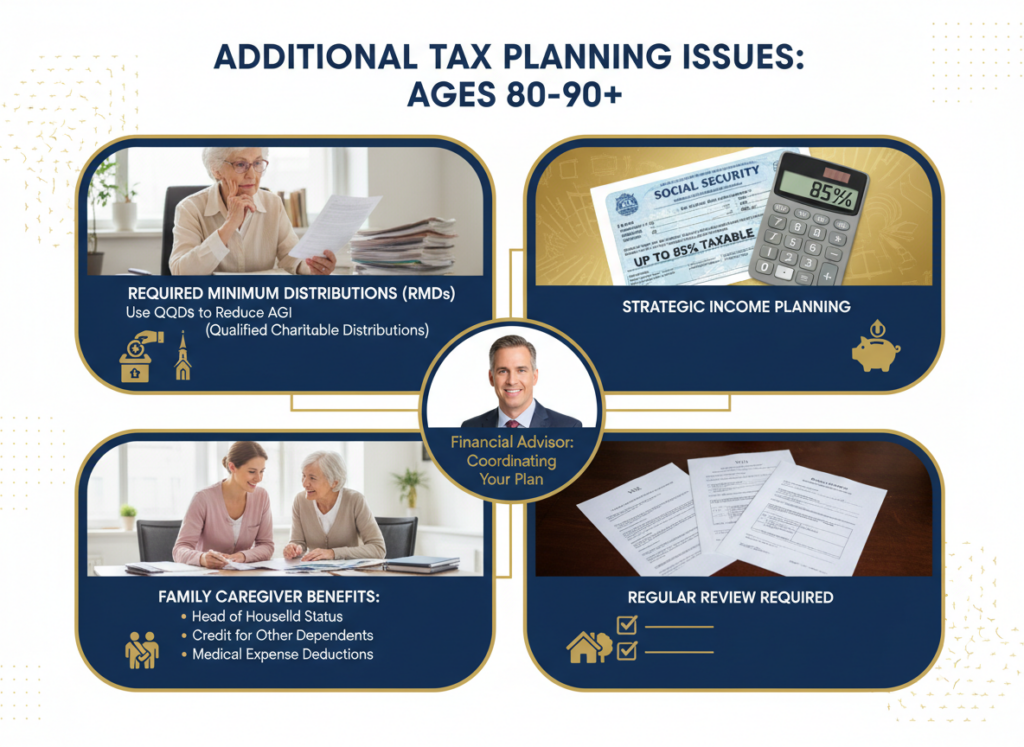

Additional Tax Planning Issues for Clients in Their 80s and 90s

Comprehensive tax planning for aging clients also includes attention to several ongoing tax matters:

Required Minimum Distributions (RMDs)

Even modest retirement accounts can create taxable income. Qualified charitable distributions (QCDs) allow clients to satisfy RMDs while reducing adjusted gross income.

Social Security Taxation

Depending on income levels, up to 85% of Social Security benefits may be taxable. Strategic planning can help manage marginal tax brackets.

Family Caregiver Tax Benefits

Adult children supporting an aging parent may qualify for head of household filing status, the credit for other dependents, or medical expense deductions if requirements are met.

Estate Planning Maintenance

Wills, powers of attorney, health care directives, and beneficiary designations should be reviewed regularly to prevent unintended outcomes.

The Advisory Value of Tax Planning for Aging Clients

For tax professionals, tax planning for aging clients represents a valuable advisory niche. These engagements often involve multiple family members and can lead to long-term, multigenerational relationships.

Action steps you can take:

Ask proactive questions before health or housing changes occur.

Encourage organized documentation of medical expenses and home improvements.

Educate adult children alongside aging parents.

Position your firm as experienced in senior and family-focused tax planning.

Final Takeaway

Aging clients face pivotal decisions involving their homes, health care, and family assets. Tax planning for aging clients is not just about reducing tax—it’s about providing clarity, protection, and confidence during life’s most important transitions.

By addressing these issues early and thoughtfully, tax professionals can safeguard client wealth, reduce family stress, and deliver meaningful value when it matters most.

Business entity selection is one of the most impactful decisions a business owner can make, yet it is often left untouched for years. As 2025 draws to a close and the tax landscape prepares for meaningful changes in 2026, year-end planning offers a critical opportunity to reassess whether a company’s current structure still supports its financial, tax, and long-term goals.

Entity selection affects far more than tax rates. It shapes how income is taxed, how losses are used, how compensation is structured, and how a business prepares for growth, retirement, or succession. A thoughtful review before year-end allows tax professionals and business owners to align structure with strategy—before deadlines pass and options narrow.

Why Business Entity Selection Matters at Year-End

Year-end is when income levels become clear, ownership changes are finalized, and planning for the coming year begins. This timing makes business entity selection especially important. Decisions made now can influence tax outcomes not only for the current year but well into 2026 and beyond.

Expected rate adjustments, evolving compliance requirements, and shifting business goals mean that a structure that worked in prior years may no longer be optimal. Reviewing entity choice at year-end allows advisors to identify whether staying the course makes sense or whether restructuring could deliver meaningful tax or operational benefits.

Understanding Business Entity Selection Across Common Structures

Effective business entity selection requires understanding how each entity type operates under current law and how it may be affected by upcoming changes.

C Corporations

C corporations offer a flat corporate tax rate and a familiar legal framework. They are often well-suited for businesses that plan to reinvest profits, pursue outside investors, or prepare for equity-based growth. However, double taxation remains a central consideration. Profits taxed at the corporate level may be taxed again when distributed to shareholders, which can reduce overall tax efficiency for owners seeking regular distributions.

S Corporations

S corporations provide pass-through taxation while allowing flexibility in managing compensation and distributions. For many closely held businesses, this balance can be attractive. That said, eligibility rules—such as limits on shareholders, ownership restrictions, and the single-class-of-stock requirement—must be reviewed regularly. Reasonable compensation remains a key compliance issue and should be part of any year-end evaluation.

Partnerships and Multi-Member LLCs

Partnerships and multi-member LLCs offer the greatest flexibility in business entity selection. Special allocations, tiered ownership, and customized economic arrangements make them ideal for complex or evolving businesses. However, this flexibility comes with added administrative responsibility, including basis tracking, capital account maintenance, and careful handling of self-employment tax exposure.

How Business Entity Selection Impacts Tax Outcomes

Choosing the right entity structure affects how income and losses flow to owners. As income increases or business activity shifts, the tax efficiency of one entity compared to another can change significantly.

Year-end planning allows professionals to model how 2026 tax rules may affect pass-through income, corporate earnings, or owner compensation. A structure that minimizes tax under current conditions may become less favorable as thresholds, rates, or limitations change.

Year-End Planning Tools That Affect Business Entity Selection

Several planning tools can influence business entity selection, but many come with strict timing requirements. Late S elections, check-the-box classifications, or restructuring transactions may be available only if action is taken before year-end or within specific election windows.

Missing these deadlines can delay a desired strategy by an entire year, potentially resulting in higher taxes or lost planning opportunities. Reviewing entity options before year-end ensures that clients do not miss critical elections that could support their 2026 objectives.

Business Entity Selection and Long-Term Planning Goals

Entity choice does not exist in isolation. Business entity selection interacts closely with retirement planning, succession strategies, and compensation design.

A business planning for a future sale or generational transfer may benefit from the flexibility offered by partnership structures. Owners seeking to maximize retirement contributions may find different opportunities depending on whether they operate as an S corporation or C corporation. Evaluating entity choice with a long-term lens helps ensure that today’s structure does not limit tomorrow’s options.

Communicating Business Entity Selection Decisions to Clients

Many business owners find business entity selection confusing, especially when an LLC can be taxed in multiple ways. Clear communication is essential. Explaining how distributions, wages, basis, and compliance obligations differ between entities empowers clients to participate in the decision-making process.

When clients understand the trade-offs involved, they are more likely to feel confident in the chosen structure and committed to long-term planning strategies. Year-end conversations provide a natural opportunity to revisit these topics and reinforce proactive planning.

Preparing for 2026 Through Smart Business Entity Selection

As 2026 approaches, tax professionals should encourage clients to view business entity selection as an evolving strategy rather than a one-time decision. Economic conditions change, tax laws evolve, and business goals shift. Regular reviews ensure that entity choice remains aligned with both current operations and future plans.

Proactive evaluation at year-end allows businesses to enter the new tax year with clarity, confidence, and a structure designed to support growth and compliance.

Key Takeaway

Business entity selection is a foundational element of effective tax and business planning. Year-end offers the ideal moment to reassess whether a company’s current structure still supports its goals in light of upcoming 2026 changes.

By reviewing entity choice now—before deadlines pass—business owners and advisors can position the business for tax efficiency, operational flexibility, and long-term success. A well-timed evaluation today can prevent costly adjustments tomorrow and ensure the business is built for what lies ahead to support sustainable growth.

Final Thoughts

Business entity selection is not a decision that should be made once and forgotten. As tax laws evolve and business goals change, the structure that once worked well may no longer deliver the best results. Reviewing entity choice at year-end allows business owners to step into the next tax year with clarity, confidence, and a structure aligned to both current operations and future plans.

Taking time now to reassess entity selection can help avoid missed opportunities, reduce tax inefficiencies, and support long-term growth. A proactive review before year-end ensures that your business enters the new year prepared, compliant, and strategically positioned for what lies ahead.

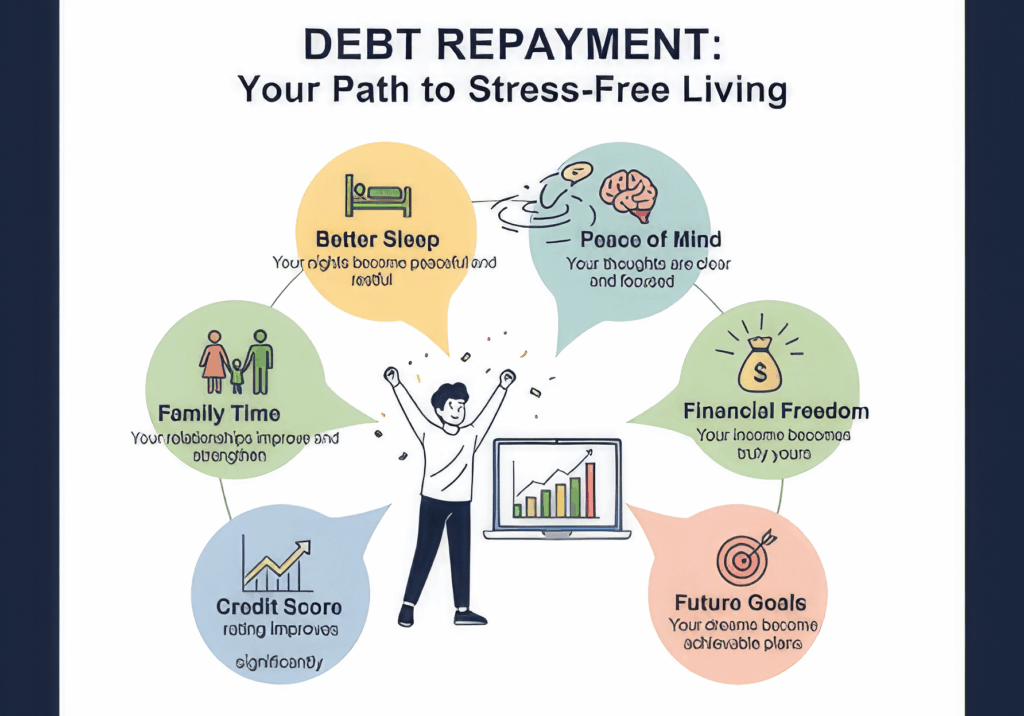

If you’re drowning in credit cards, loans, or medical bills, you’re not alone—but you can Crush Your Debt Faster with a clear plan. The problem for most people isn’t a lack of effort; it’s a lack of strategy. You pay a little here, a little there, and it feels like nothing ever changes.

Two proven methods can turn that around:

The Debt Snowball Method

The Debt Avalanche Method

Both are powerful debt repayment strategies that help you stay focused and make real progress. In this guide, you’ll learn how each method works, who they’re best for, and how to choose the one that helps you Crush Your Debt Faster without burning out.

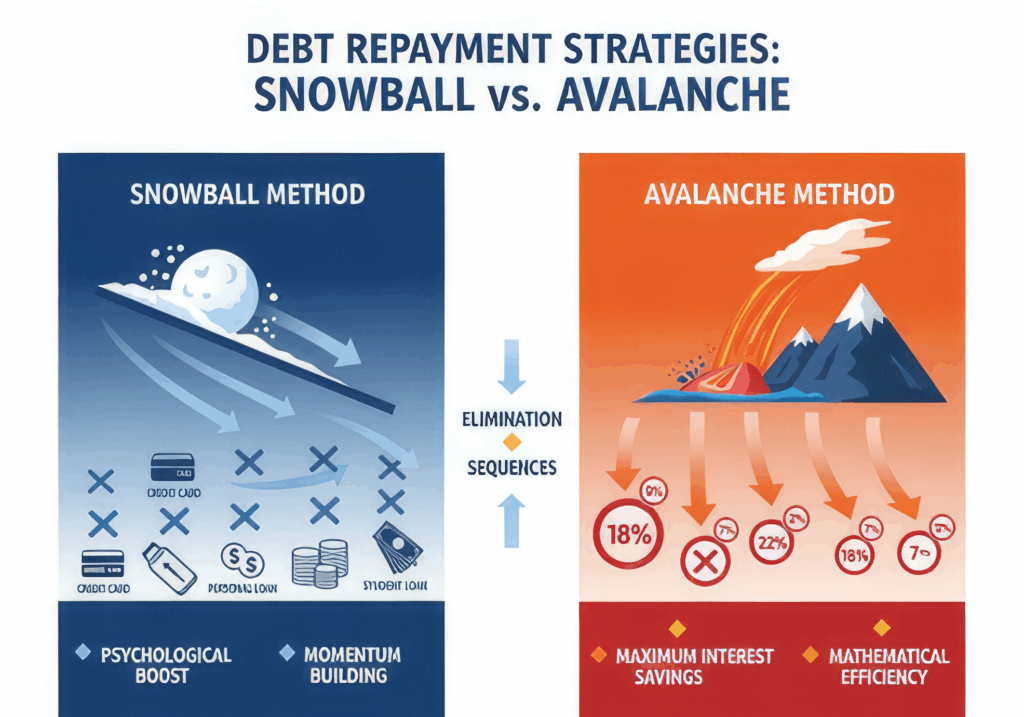

What Is the Debt Snowball Method?

The Debt Snowball Method is built around small, fast wins. Instead of worrying about interest rates, you focus on paying off your smallest debts first and create momentum.

How the Snowball Method Works

List all your debts from smallest balance to largest.

Pay the minimum on every debt.

Put all extra money toward the smallest debt.

Once that debt is gone, “snowball” its payment into the next smallest debt.

Repeat until every debt is paid off.

Even though this method isn’t always mathematically perfect, it helps you Crush Your Debt Faster because it keeps you emotionally engaged.

Why the Snowball Method Works

You eliminate entire balances quickly.

Each win builds motivation and confidence.

The plan is simple, so you’re less likely to quit.

Best for: people who feel overwhelmed, emotional spenders, and anyone who needs quick proof that their efforts are working.

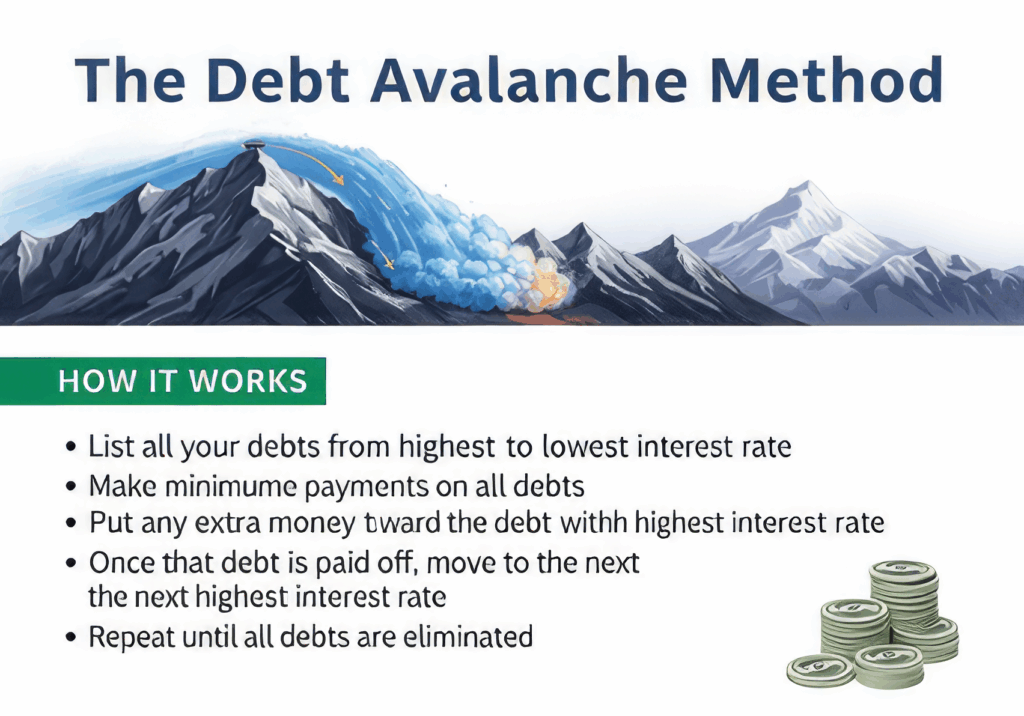

What Is the Debt Avalanche Method?

The Debt Avalanche Method is focused on saving the most money in interest and often paying off everything in less time overall. Instead of looking at balance size, you look at interest rates.

How the Avalanche Method Works

List all your debts from highest interest rate to lowest.

Pay the minimum on all debts.

Put all extra money toward the highest-interest debt.

Once it’s paid off, move to the next highest rate.

Continue until you’re completely debt-free.

This approach helps you Crush Your Debt Faster from a financial perspective, even if early progress is less visible.

Why the Avalanche Method Works

You pay less total interest.

You usually finish your debt-free journey sooner.

It’s especially powerful for high-interest credit cards.

Best for: disciplined people who like numbers, want to minimize interest, and don’t need immediate emotional wins.

Snowball vs. Avalanche: Key Differences

Use this in a Table block in WordPress:

Feature

Debt Snowball

Debt Avalanche

Main Focus

Smallest balance first

Highest interest rate first

Motivation

Fast emotional wins

Long-term savings

Interest Saved

Less

More

Speed Overall

Sometimes slower

Often faster

Complexity

Very simple

Requires tracking rates

Best For

Motivation & momentum

Efficiency & savings

In simple terms:

Snowball is emotion-first, math-second.

Avalanche is math-first, emotion-second.

To Crush Your Debt Faster, you need the one that aligns with how you think and behave.

Which Strategy Will Help You Crush Your Debt Faster?

The “best” strategy is the one you actually stick with.

Ask yourself:

Do I lose motivation when progress is slow?

Do I care more about paying less interest or feeling progress sooner?

Do I like simple, no-math plans or detailed, optimized ones?

Choose the Snowball Method If…

You’ve started and stopped debt payoff plans before.

You feel better when you see entire accounts hit zero.

You want an easy way to Crush Your Debt Faster through motivation.

Choose the Avalanche Method If…

You’re patient and disciplined.

You want to save the most money on interest.

You’re okay waiting longer for the first “big win.”

There’s no wrong answer. The real mistake is staying stuck and using no system at all.

Can You Combine Both Strategies?

Absolutely. You don’t have to pick one and stay with it forever. A hybrid approach can help you Crush Your Debt Faster while balancing emotion and efficiency.

Start with a mini Snowball: Pay off one or two tiny debts first to create quick momentum.

Switch to Avalanche: Once you feel focused and confident, reorder your remaining debts by interest rate and attack the highest one.

Reset when needed: If you feel stuck again, temporarily use the Snowball on a small balance to regain motivation.

This blended method gives you the emotional wins of Snowball and the interest savings of Avalanche.

Real-Life Example: Which Method Wins?

Meet Sam. Sam has these debts:

Debt Type

Balance

Interest Rate

Credit Card A

$1,500

22%

Credit Card B

$800

18%

Personal Loan

$3,000

10%

Medical Bill

$500

0%

Sam can put $450 per month toward debt.

With the Debt Snowball

Order from smallest balance:

Medical Bill – $500

Credit Card B – $800

Credit Card A – $1,500

Personal Loan – $3,000

Sam wipes out the medical bill in just over one month, then Credit Card B a few months later. These fast wins make Sam feel powerful and in control—and that feeling helps Sam Crush Debt Faster because the plan doesn’t get abandoned.

With the Debt Avalanche

Order by highest interest rate:

Credit Card A – 22%

Credit Card B – 18%

Personal Loan – 10%

Medical Bill – 0%

Sam needs more time before one entire account disappears, but pays much less interest overall and finishes the total payoff sooner than with Snowball.

Takeaway:

Snowball helps Sam stay emotionally committed.

Avalanche helps Sam save more and mathematically Crush Debt Faster.

You choose which “faster” matters more: faster emotionally, or faster financially.

Final Thoughts: Start Crushing Your Debt Today

You don’t need perfect timing, a big income, or a miracle. You just need a plan you’ll actually follow.

Use Debt Snowball if motivation is your biggest challenge.

Use Debt Avalanche if interest savings and efficiency matter most.

Use a hybrid strategy if you want both.

Most importantly, take action. The sooner you start, the sooner you’ll Crush Your Debt Faster and free up your income for saving, investing, and building the life you actually want.

Pick your strategy today and start your debt-free journey.

📞 Ready to Finally Crush Your Debt Faster and Take Control of Your Financial Future?

If you need expert guidance on budgeting, debt repayment planning, or complete financial management, Veritas Accounting Services is here to support you every step of the way.

Contact Veritas Accounting Services:

📧 Email:hello@veritasaccountingservices.com 📞 Phone: +1 (678) 723-6003 | +91 97255 52243 🏢 US Office: 8735 Dunwoody Place – 4549, Atlanta, GA 🏢 India Office: C-305, The Imperial Heights, 150ft Ring Road, Rajkot

We proudly serve clients across the US, UK, UAE, Singapore, Ireland, and Malaysia, offering personalized bookkeeping, debt planning, tax filing, and CFO-level financial

In the complex world of investment planning, one of the most overlooked strategies is maximizing tax-free investment income. While many investors focus solely on returns, the smartest wealth builders understand that it’s not what you earn—it’s what you keep after taxes that truly matters.

What is Tax-Free Investment Income?

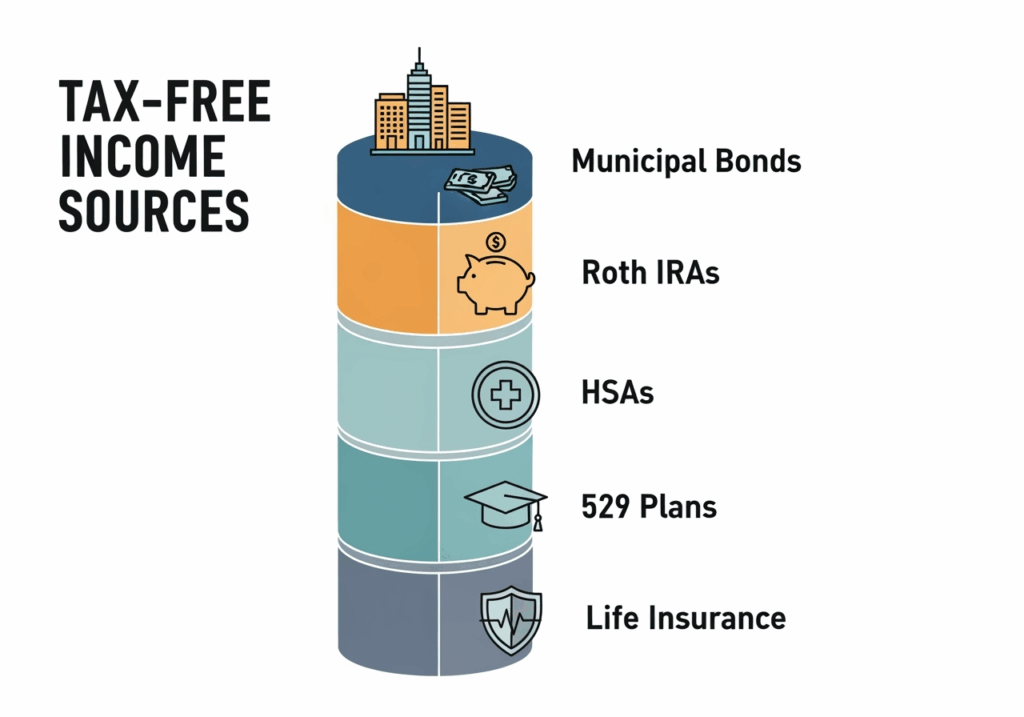

Tax-free investment income refers to earnings from specific investment vehicles that are exempt from federal income taxes, and in some cases, state and local taxes as well. The three primary sources include:

1. Municipal Bonds

Municipal bonds, or “munis,” are debt securities issued by state and local governments to fund public projects. The interest earned from these bonds is typically exempt from federal income tax and may also be exempt from state and local taxes if you live in the issuing state.

Types of Municipal Bonds to Consider:

General Obligation Bonds: Backed by the full faith and credit of the issuing municipality

Revenue Bonds: Secured by specific revenue streams from projects like toll roads or utilities

Private Activity Bonds: May be subject to AMT but offer higher yields

Build America Bonds: Federally subsidized municipal bonds with taxable interest

2. Roth IRAs

Unlike traditional IRAs, Roth IRA contributions are made with after-tax dollars. However, qualified withdrawals in retirement—including both contributions and earnings—are completely tax-free, making them a powerful long-term wealth-building tool.

Advanced Roth Strategies:

Roth Ladder Conversions: Systematic conversions over multiple years to manage tax brackets

Mega Backdoor Roth: For high earners with 401(k) plans allowing after-tax contributions

Roth IRA Inheritance Planning: Tax-free wealth transfer to beneficiaries

3. Life Insurance Payouts

Certain life insurance policies, particularly permanent life insurance with cash value components, can provide tax-free income through policy loans and withdrawals up to your basis in the policy.

Private Placement Life Insurance (PPLI): For ultra-high-net-worth individuals

Corporate-Owned Life Insurance (COLI): Business tax planning applications

Additional Tax-Free Income Sources

Health Savings Accounts (HSAs)

Often called the “triple tax advantage” account, HSAs offer:

Tax-deductible contributions

Tax-free growth

Tax-free withdrawals for qualified medical expenses

After age 65, withdrawals for non-medical purposes are taxed as ordinary income (like a traditional IRA)

529 Education Savings Plans

While contributions aren’t federally deductible, earnings grow tax-free and withdrawals for qualified education expenses are tax-free. Recent expansions allow:

K-12 tuition payments up to $10,000 annually

Student loan repayments up to $10,000 lifetime

Beneficiary changes to family members

Why Tax-Free Investment Income Matters More Than Ever

Protecting Your Overall Tax Picture

Tax-free investment income doesn’t just save you money on taxes—it provides strategic advantages that many investors overlook:

No impact on taxable income calculations: This income won’t push you into higher tax brackets

Medicare surcharge protection: High-income earners can avoid additional Medicare premiums triggered by modified adjusted gross income (MAGI)

Alternative Minimum Tax (AMT) benefits: Tax-free municipal bond interest generally doesn’t trigger AMT calculations

Social Security taxation: Lower taxable income may reduce the taxation of your Social Security benefits

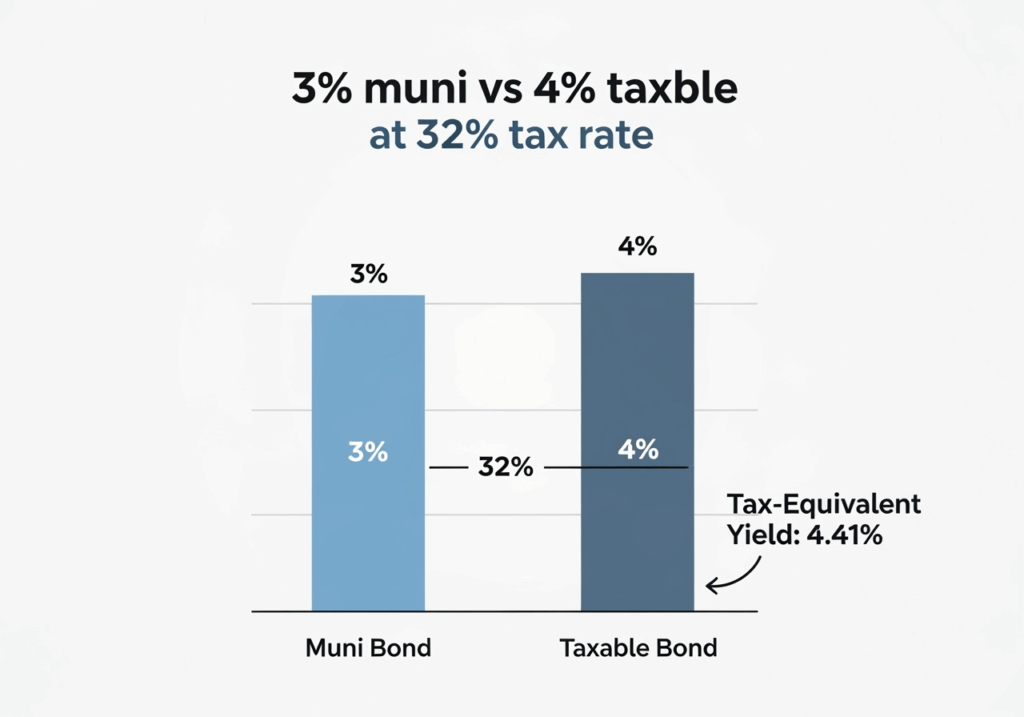

The Compound Effect of Tax Efficiency

Consider this scenario: An investor in the 32% tax bracket earning 4% on taxable bonds nets only 2.72% after taxes. Meanwhile, a municipal bond yielding 3% provides the full 3% return—effectively outperforming the taxable investment while reducing risk.

Interest rate sensitivity: Shorter-duration municipal bonds provide protection against rate increases

Credit quality improvements: Many municipalities have strengthened their financial positions post-pandemic

Supply and demand imbalances: Limited municipal bond issuance has created attractive opportunities

The Missed Opportunity: Why Many Portfolios Aren’t Optimized

Common Portfolio Oversights

Many investors and their advisors focus primarily on gross returns without considering the tax implications. This oversight becomes particularly costly for:

Strategic Implementation: Making Tax-Free Income Work for You

1. Portfolio Assessment and Rebalancing

The first step is conducting a comprehensive analysis of your current investment allocation. This involves:

Evaluating your current tax burden from investments

Identifying opportunities to shift from taxable to tax-advantaged accounts

Analyzing the after-tax returns of your current holdings

2. Municipal Bond Strategy

For investors in higher tax brackets, municipal bonds can be particularly attractive:

General obligation bonds backed by the full faith and credit of the issuer

Revenue bonds supported by specific project income

Tax-exempt bond funds for diversification and professional management

3. Maximizing Roth IRA Benefits

Strategic Roth IRA planning includes:

Roth conversions during lower-income years

Backdoor Roth strategies for high-income earners

Long-term planning to maximize tax-free growth

4. Advanced Tax-Free Strategies

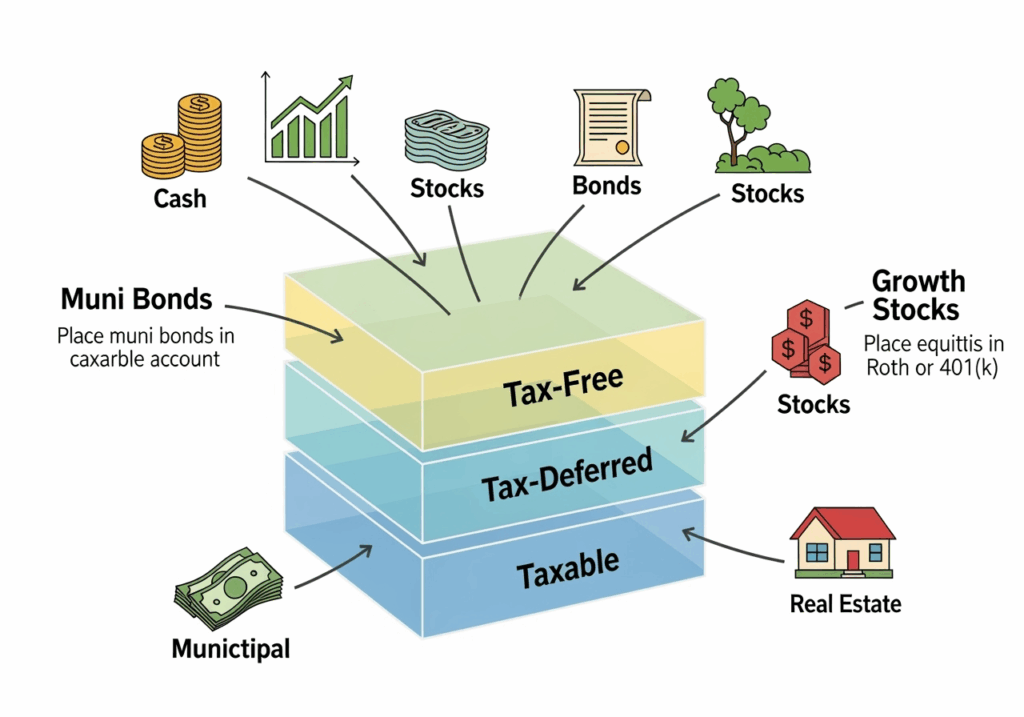

Asset Location Optimization:

Hold tax-inefficient investments in tax-advantaged accounts

Place tax-efficient investments in taxable accounts

Coordinate across multiple account types for maximum benefit

5. Tax-Loss Harvesting Coordination:

Realize losses in taxable accounts while maintaining tax-free growth elsewhere

Avoid wash sale rules when rebalancing across account types

Use tax-free income to reduce the need for taxable rebalancing

Global Considerations for International Investors

At Veritas Accounting Services, we understand that tax-efficient investing becomes even more complex for international investors and expatriates. Our global expertise across the US, UK, UAE, Singapore, Ireland, and Malaysia ensures that your tax-free investment strategy considers:

Treaty benefits between countries

Foreign tax credit optimization

Cross-border retirement planning

Compliance requirements in multiple jurisdictions

International Tax-Free Opportunities

Different countries offer unique tax-advantaged investment vehicles:

UK ISAs (Individual Savings Accounts): Tax-free growth and withdrawals

Singapore CPF: Comprehensive retirement and healthcare savings

Irish life assurance bonds: Tax-deferred growth opportunities

The Veritas Advantage: Comprehensive Tax-Efficient Planning

With over a decade of experience and 1000+ successful projects, Veritas Accounting Services specializes in creating holistic financial strategies that maximize after-tax returns. Our certified QuickBooks and Xero experts work closely with your investment advisors to ensure your portfolio is optimized for tax efficiency.

Our Integrated Approach Includes:

Tax planning consultations to identify optimization opportunities

Investment income analysis and tax impact assessments

Retirement planning coordination with tax-free income strategies

Ongoing monitoring to ensure continued tax efficiency

Technology-Driven Solutions

Our seamless integration with leading accounting platforms ensures:

Real-time tax impact monitoring of investment decisions

Automated reporting of tax-free income sources

Coordinated planning between business and personal finances

Compliance tracking across multiple jurisdictions

Take Action: Don’t Let Tax Inefficiency Erode Your Wealth

The opportunity cost of maintaining a tax-inefficient portfolio compounds over time. Every year you delay implementing tax-free investment strategies is another year of unnecessary tax payments and missed wealth accumulation.

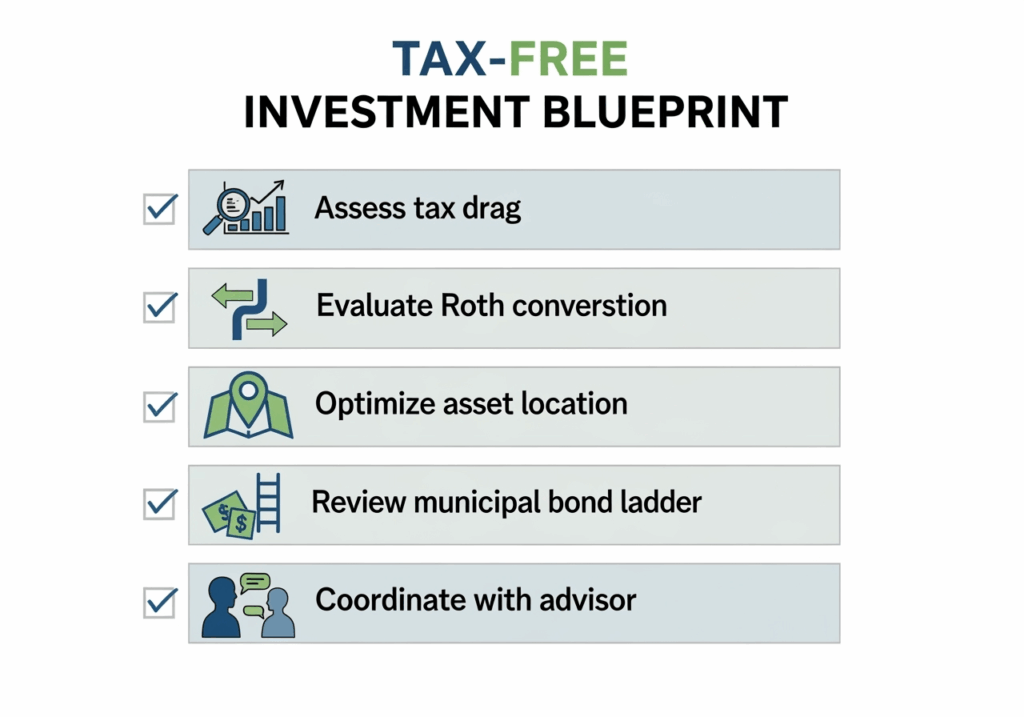

Immediate Action Items:

Calculate your current tax drag: Determine how much you’re paying in unnecessary investment taxes

Assess your tax bracket trajectory: Plan for future income changes

Review your asset location: Ensure tax-efficient placement of investments

Evaluate conversion opportunities: Consider Roth conversions during low-income periods

Next Steps:

Schedule a consultation to review your current investment tax burden

Analyze your portfolio for tax-efficiency opportunities

Develop a strategic plan to maximize tax-free income

Implement and monitor your optimized investment strategy

Conclusion

Tax-free investment income isn’t just about avoiding taxes—it’s about building a more efficient, sustainable wealth accumulation strategy. In today’s complex tax environment, the difference between tax-efficient and tax-inefficient investing can mean hundreds of thousands of dollars over a lifetime.

Don’t let this opportunity pass by. Contact Veritas Accounting Services today to discover how tax-free investment income strategies can transform your financial future.

Ready to optimize your investment portfolio for maximum tax efficiency?

Tax-Free Investment Income Tax-Free Investment Income Tax-Free Investment Income Tax-Free Investment Income Tax-Free Investment Income Tax-Free Investment Income Tax-Free Investment Income

To correctly classify business expenses is foundational to solid bookkeeping and financial decision-making. Yet, many business owners and freelancers trip up in this area—leading to lost deductions, inaccurate reporting, and extra stress during tax season. Let’s change that!

In this guide, you’ll learn:

What counts as a business expense (with real examples)

Why classification matters so much

Common and costly mistakes (and how to sidestep them)

Pro tips for flawless, stress-free accounting

Answers to the most frequent questions

A printable, actionable checklist to keep you organized

What Counts as a Business Expense? (With Real-World Examples)

Business expenses are the ordinary and necessary costs of running your company. But what does that mean in practice?

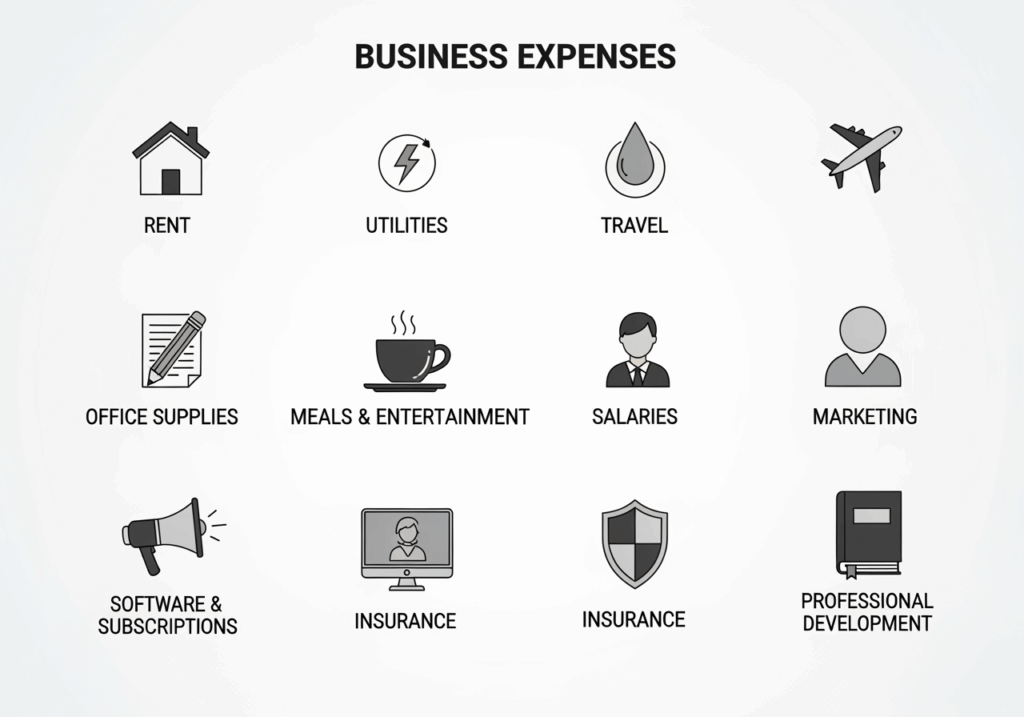

Here are popular categories and real examples for each:

Travel: Airfare, mileage, taxis/rideshares, hotels, meals on work trips

Meals and Entertainment: Taking clients out for lunch, company event catering (subject to strict limits)

Salaries and Wages: Staff pay, bonuses, payroll taxes

Professional Services: Legal, accounting, consulting fees

Insurance: Business liability, workers comp, property insurance

Marketing and Advertising: Website fees, online ads, print materials

Depreciation: Gradual cost deduction for major purchases like machinery or vehicles

Pro Tip: If you’re ever unsure if an expense qualifies, ask yourself—”Is this cost directly related to earning business income?” If the answer’s yes, it likely qualifies.

Why Correct Classification Matters

Classifying business expenses correctly doesn’t just make life easier for your accountant. Here’s why it truly matters:

Maximize Tax Deductions: Many allowable business expenses directly reduce taxable income, meaning less money owed to the government (and more in your pocket).

Financial Insights: Accurate expense tracking reveals which parts of your business are costing the most—and where you can cut back.

Audit Readiness: Clean, careful records make audits quick and painless if you ever get selected.

Credibility with Investors/Banks: Lenders or investors like to see well-organized, easy-to-explain financials.

Common Expense Classification Mistakes (With Solutions)

Let’s explore mistakes in detail, with real-world fixes:

1. Mixing Personal and Business Finances

Example: You grab a coffee using your business card, but it’s not a work-related purchase.

Fix: Set up separate bank accounts and credit cards. If you make a mistake, note the transaction as an owner draw or personal reimbursement.

2. Misclassifying Expenses

Example: Coding a business lunch with a client as “Office Supplies,” or putting software under “Equipment.”

Fix: Use accounting software with preset categories. Review transactions monthly for accuracy.

3. Missing Out on Small Deductions

Example: Ignoring small subscriptions or petty cash expenses; assuming they’re “too minor.”

Fix: Track every expense, even $2 ones. Digital tools make this frictionless; use expense scanning apps or file receipts in Google Drive.

4. Lost or Incomplete Documentation

Example: Tossing receipts or not collecting itemized bills.

Fix: Go digital—scan with your phone, save PDFs, or use receipt-management platforms like Expensify or Dext.

5. Over- or Underclaiming Deductions

Example: Claiming the full cost of your personal mobile as a business expense, or not claiming your home office at all.

Fix: Claim only the business-use portion. For mixed-use items (like utilities at home), use a percentage based on actual use.

6. Not Updating Categories as Business Grows

Example: Sticking to overly simple categories (“other expenses,” “miscellaneous”) as your business expands.

Use cloud-based software like QuickBooks, Xero, Zoho, or Wave, which auto-categorizes common expenses (and syncs with your bank!).

Set up rules so recurring transactions (like your internet bill) are always coded to the right category.

Be Consistent

Define your categories clearly and always use them the same way.

If you have a team, create a simple one-pager explaining what belongs where.

Schedule a Monthly “Money Date”

Take 30 minutes at the end of each month to review your transactions, match receipts, and fix any uncategorized expenses.

Educate the Whole Team

Train employees on proper receipt submission and expense types.

Use an approval system for purchases, so random expenses don’t slip through.

Document Your Expense Policy

Put your rules in writing! This helps if you ever hire a bookkeeper or get audited.

Ask for Professional Help

An accountant or bookkeeper can review your setup, optimize your categories, and ensure you’re maximizing deductions.

FAQs: Business Expense Classification

Classify Business Expenses

Q: Can I deduct all meals with clients? A: Not always. Many tax authorities cap meal deductions at 50%, and receipts/documentation are required. Casual or non-business meals don’t qualify.

Q: What if I work from a home office—how do I classify those expenses? A: Calculate the percentage of your home used for business (by area or time) and claim that portion of rent, utilities, and insurance as a business expense.

Q: Is my car a business expense if I also use it personally? A: Only claim the percentage of car expenses related to business miles. Use a mileage log or mileage-tracking app.

Q: What if I make a mistake? A: Adjust the transaction and document the change. Most software allows easy recategorization.

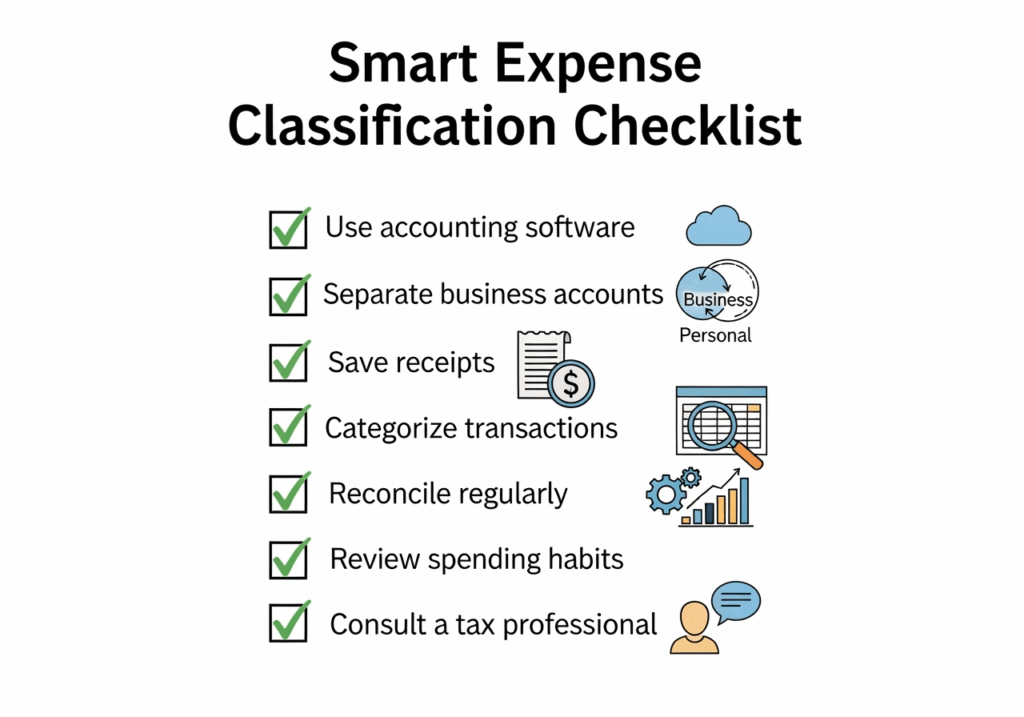

Actionable Checklist for Smarter Expense Classification

Feel free to print or bookmark this!

Setup

✅ Open designated business bank accounts ✅ Choose accounting or expense tracking software ✅ Create a clear chart of accounts (categories)

Ongoing Process

✅ Always use the business account for business purchases ✅ Save digital or physical receipts for all transactions ✅ Enter all expenses into your accounting system ✅ Review uncategorized/“miscellaneous” expenses each month ✅ Match bank and credit card transactions to entries ✅ Update categories as business grows

At Year-End

✅ Reconcile all accounts ✅ Check for missed deductions ✅ Provide clear records to your accountant ✅ Adjust categories for the new year’s goals

Final Thoughts

Getting business expense classification right isn’t just about tax season—it’s about taking charge of your business finances and making smarter decisions year-round. The more consistent (and organized) you are, the less likely you are to miss deductions, make costly errors, or panic during audits.

By using technology, documenting your process, and reviewing transactions regularly, you’ll build a system that works for you—not against you.

Need help setting up or reviewing your expense categories? Drop your questions in the comments or connect with our bookkeeping pros for a no-obligation consultation. Your future self—and your bottom line—will thank you!

classify business expenses classify business expenses classify business expenses classify business expenses classify business expenses classify business expenses classify business expenses classify business expenses classify business expenses classify business expenses classify business expenses classify business expenses classify business expenses classify business expenses classify business expenses classify business expenses classify business expenses classify business expenses

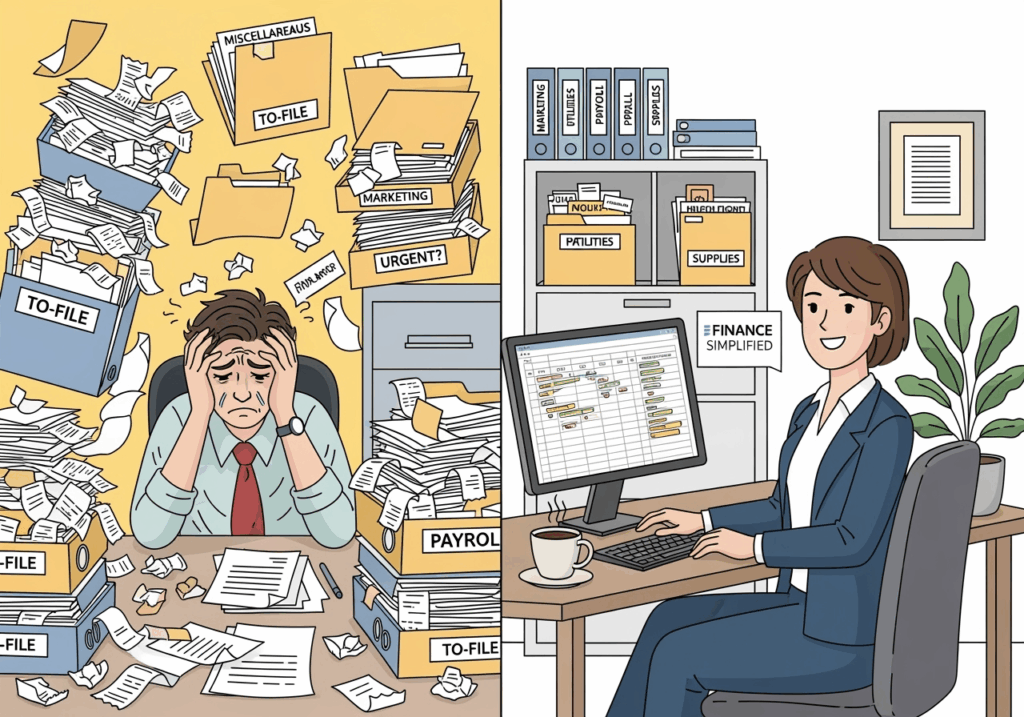

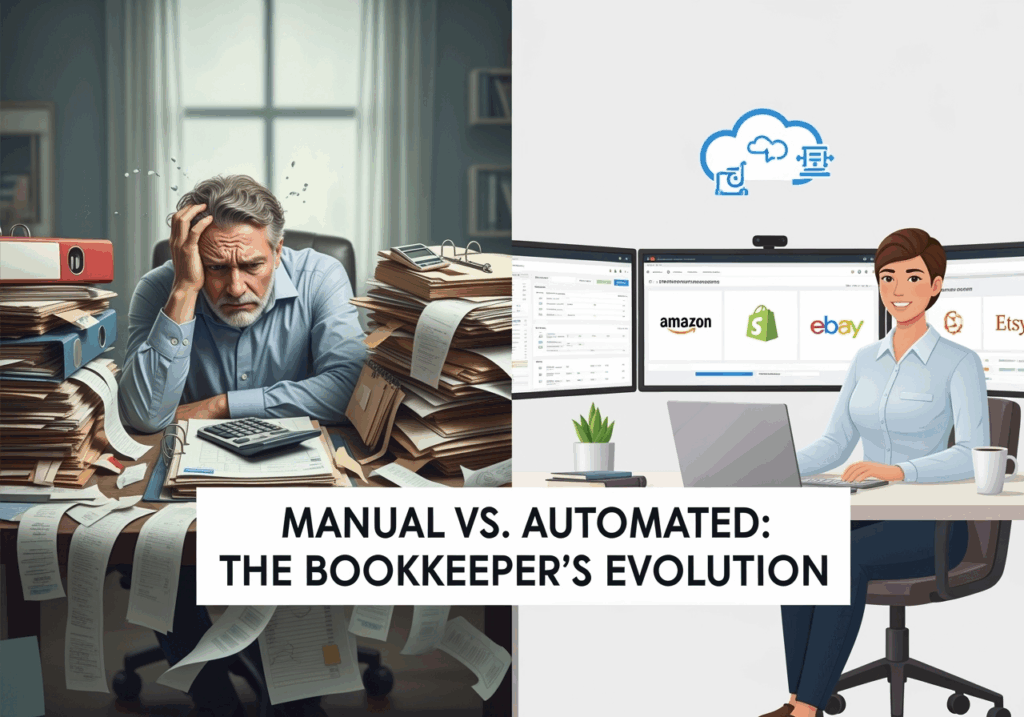

The need for bookkeepers to become strategic partners in today’s eCommerce landscape has never been greater. With eCommerce businesses rapidly expanding to multiple sales channels and automation technologies advancing at lightning speed, understanding how to streamline compliance, especially for sales tax, is essential for both client success and the growth of bookkeeping practices.

Why Multi-Channel eCommerce Changes Everything

Moving Beyond Traditional Bookkeeping

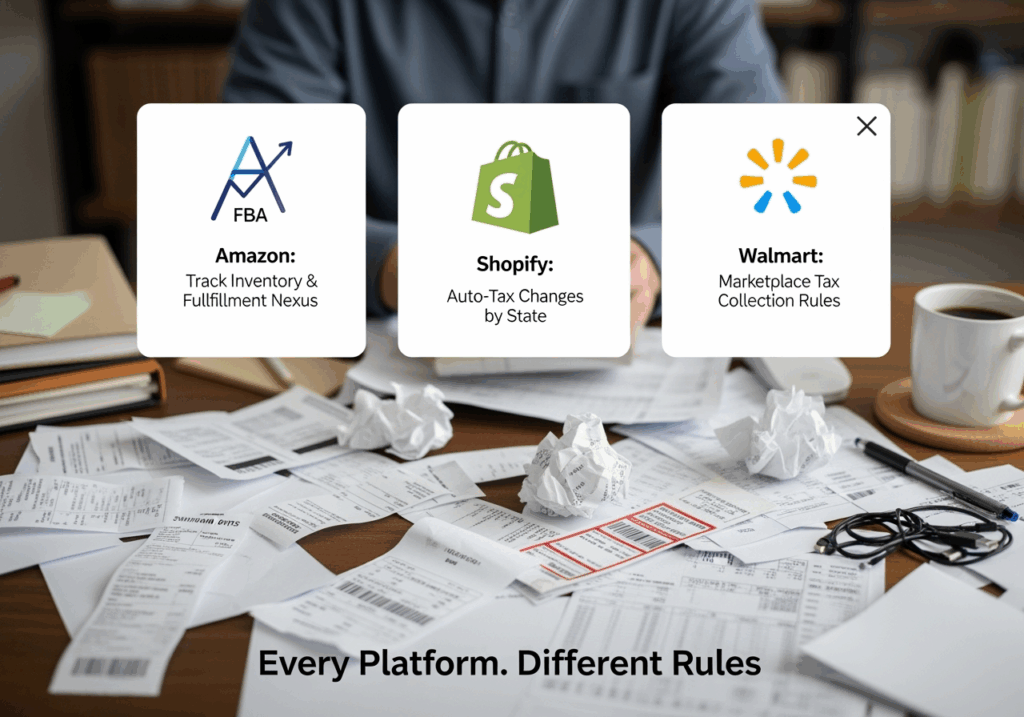

In the past, bookkeeping focused on ledgers and periodic reconciliations for a single online platform like Shopify or Amazon. Today, thriving eCommerce businesses operate on numerous platforms—Amazon, Shopify, eBay, Etsy, Walmart, Facebook Shops, and their own websites. Each generates unique data streams, reporting requirements, and tax obligations.

Key challenge: Manual processes can’t keep up. Studies show bookkeepers relying on old methods spend significantly more time for lower accuracy—investing up to 73% more effort yet achieving only around 64% accuracy in tracking sales tax compliance for multi-channel clients.

The Opportunity: Bookkeepers must transform into orchestrators of automated systems and real-time data specialists—using technology to minimize manual work and maximize insight.

The Rise of AI in Bookkeeping

Artificial intelligence has revolutionized multi-channel bookkeeping. AI-powered tools can now:

Auto-categorize transactions across channels.

Detect sales tax nexus triggers in real time.

Predict upcoming compliance needs based on client growth.

Results from AI adoption include:

89% reduction in manual data entry.

94% increase in sales tax tracking accuracy.

Capability for a bookkeeper to handle 3x more clients without extra staff.

This shift frees professionals to move from repetitive data entry into valuable client advisory and strategic roles instead.

Common Platform-Specific Bookkeeping Challenges

Each sales platform presents unique headaches:

Amazon FBA: Requires inventory tracking across fulfillment centers and a deep understanding of marketplace tax collection rules.

Shopify: Ongoing regulatory changes make it crucial to re-examine sales tax setups, particularly as Shopify introduces automatic tax collection for relevant states.

Multi-channel Inventory: Managing stock and margins across platforms can quickly spiral out of control without automation.

General Compliance: Ensuring accurate documentation in the event of a tax audit is much more complex when multiple platforms are involved.

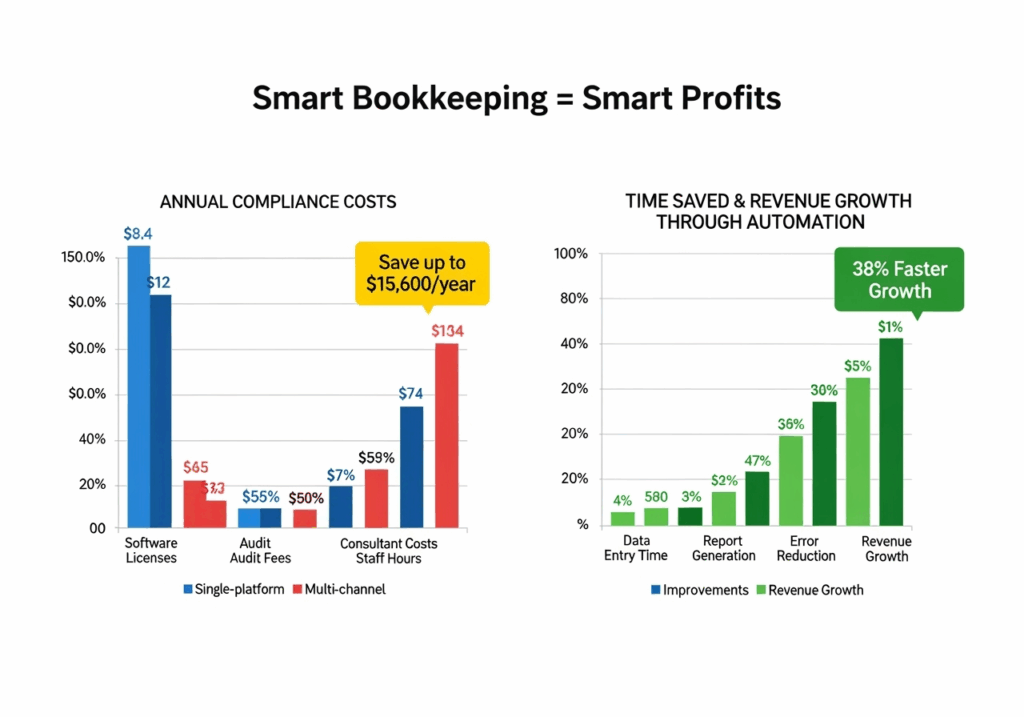

The Financial Impact of Multi-Channel Complexity

Bookkeepers can help clients not only avoid costly tax penalties but also directly improve operational efficiency.

Cost of compliance and bookkeeping: Multi-channel stores typically spend $2,400–$4,800 a year (vs. $800–$1,200 for single-platform sellers).

Potential savings from professional management: $8,400–$15,600 per year through streamlined, automated workflows.

Revenue growth advantage: Businesses on multiple channels grow revenue 38% faster than those on a single platform.

The bottom line: Effective bookkeeping turns what many see as a cost into a profit driver, enabling scalability and peace of mind.

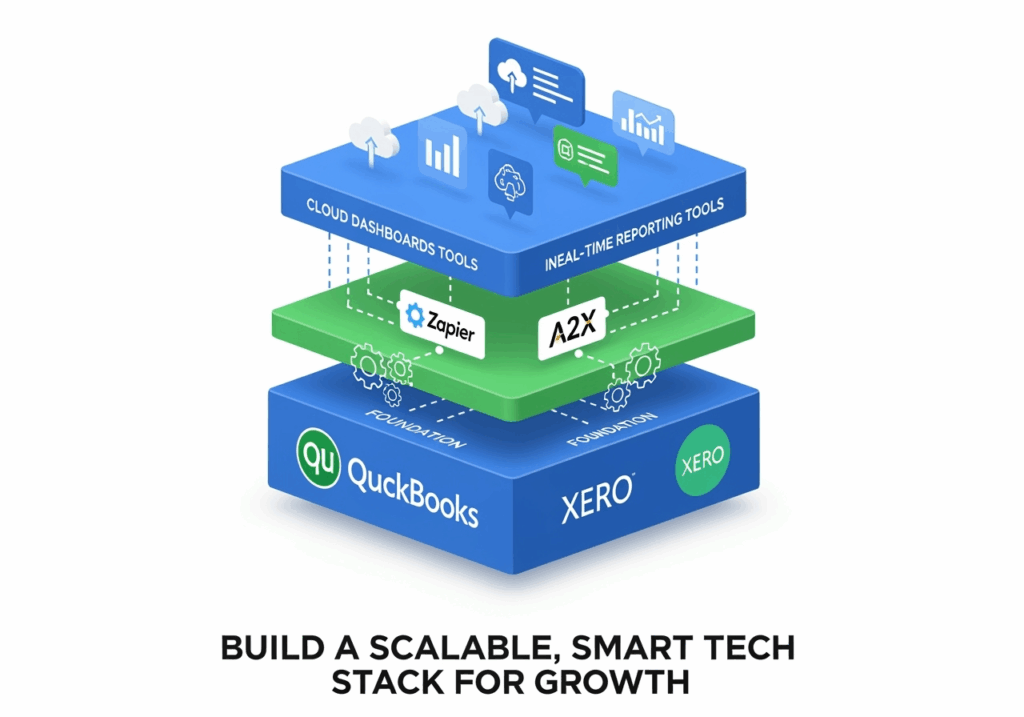

Today’s most successful bookkeeping practices rely on much more than accounting software like QuickBooks or Xero (though these should be your foundation).

Best-in-class practices also adopt:

eCommerce integration and automation tools (for sales data import, inventory sync, and multi-platform reconciliation).

Cloud-based dashboards, for 24/7 real-time access and collaboration.

Custom reports, breaking down profitability and compliance status by channel.

These investments deliver transparency, scalability, and confidence for both bookkeepers and clients.

Why Automated Sales Tax Management Is Essential

Sales tax compliance is the highest-value, most urgent service for eCommerce clients:

Multi-state nexus triggers: Identifying and registering for state sales tax as required by law.

Marketplace facilitators: Some platforms collect and remit tax, but your client is still responsible for reporting and proper record-keeping.

Automation platforms: Specialized sales tax apps eliminate manual tracking and ensure every filing is timely and complete.

Business impact: Clients typically see payback on automation within 4-6 months through penalty avoidance and saved time. For bookkeepers, sales tax services command premium rates but require minimal hands-on work after setup.

International Operations: A Lucrative Niche

International sellers entering the US face even greater complexity:

Navigating both US and home country regulations.

Handling US tax ID registration.

Managing currency and banking requirements.

These clients see the value in premium, expert services—often investing 40–60% more than domestic-only businesses. Mastering this area can set your firm apart and substantially grow your client base.

Step-by-Step: Growing Your Multi-Channel Bookkeeping Specialization

Identify potential within your existing clients. Many may be considering new sales channels—position yourself as their go-to advisor for expansion.

Invest systematically in technology. Start with core accounting integrations. Layer in automation as you add clients and revenue.

Commit to continuous learning. Stay up-to-date on eCommerce trends, tax rules, and new automation tools. This fosters innovation and justified premium billing.

Market your expertise. Tell your story clearly—how you help clients save time, avoid penalties, and optimize growth.

What the Future Holds?

eCommerce complexity and automation are only going to increase. Bookkeepers who future-proof their practices now will seize the biggest opportunities:

Combining technical skill with strategic advice.

Vying for top positioning in an expanding, lucrative market.

Serving as true partners in their clients’ growth journeys, rather than just vendors.

Why Partner with Veritas Accounting Services?

Choosing the right partner for your accounting and bookkeeping can be the difference between surviving and thriving in today’s eCommerce landscape. Veritas Accounting Services stands out through its deep expertise, innovative technology, and commitment to your business’s long-term success.

Built on Decades of Multi-Channel Experience

Veritas Accounting Services draws upon decades of hands-on experience, managing books and compliance for businesses with operations spanning the globe. This cross-border expertise means clients benefit from specialized knowledge in managing the challenges of international VAT, US sales tax, and complicated multi-channel reporting requirements. Whether you sell on Amazon, Shopify, Etsy, Walmart, or your own website, the Veritas team understands the pain points unique to eCommerce and knows how to navigate them smoothly.

Proprietary, Seamless Integration with Leading Software

The technology stack at Veritas is robust and highly adaptable. Clients enjoy seamless integration with industry-leading cloud platforms, including QuickBooks Online, Xero, Wave, Zoho Books, and other specialized eCommerce accounting tools. This integration not only speeds up processes, but also enables real-time reconciliation, inventory tracking, and advanced analytics across every channel you utilize—all while maintaining absolute accuracy and compliance. Automated solutions provided by Veritas eliminate manual data entry, drastically reduce errors, and free you to focus on scaling your business.

Proven Track Record: 340+ International Clients Served

When you work with Veritas, you join an expanding network of 340+ happy international brands who have successfully optimized and protected their financial operations. The results speak for themselves—Veritas clients consistently achieve a 99.7% compliance accuracy rate, drastically lowering exposure to penalties, tax audits, and administrative burden. By minimizing risk and creating transparent, audit-ready reporting, Veritas provides peace of mind so you can pursue growth with confidence.

More Than Bookkeepers—Strategic Growth Partners

Veritas doesn’t just keep your books; the team acts as your virtual CFO, advisor, and strategic partner. Their personalized process includes in-depth business analysis, proactive compliance monitoring, and recommendations on cashflow management, forecasting, and even process automation for scaling up efficiently. This level of involvement helps clients unlock hidden savings, capture new opportunities, and stay ahead of regulatory changes, both in the US and internationally.

Flexible, Scalable Services Designed for You

Whether you’re a fast-growing startup or a seasoned multinational, Veritas tailors its solutions to fit your needs. You gain the flexibility to scale services up or down as your operations evolve, thanks to the team’s experience with a wide range of business models and industries—from eCommerce and logistics to restaurants and professional services.

If you’re ready to build a future-proof, competitive, and growth-oriented practice—or need a dedicated accounting partner capable of supporting your multi-channel eCommerce ambitions—reach out to Veritas Accounting Services today at hello@veritasaccountingservices.com or call +1(678) 723-6003.

Navigating sales tax compliance as a marketplace seller can be overwhelming, especially with constantly evolving regulations across 45 US states. With marketplace facilitator laws now generating over $13.7 billion annually and economic nexus thresholds affecting 2.4 million e-commerce businesses, knowing what to prioritize—and what to skip—has never been more critical. Prioritizing the right compliance strategies protects both your bottom line and your peace of mind.

Recent data from the sales tax Institute reveals a startling reality: 67% of marketplace sellers are either over-complying, wasting valuable resources on unnecessary tasks, or under-complying, risking substantial penalties. The average penalty for non-compliance reached $4,200 per business in 2024, while businesses that over-comply spend an unnecessary $2,400 annually on redundant compliance activities. This comprehensive guide will help you focus your efforts where they matter most while avoiding common compliance traps that drain time and resources without adding value.

Understanding Your Marketplace Coverage: The Foundation of Smart Compliance

Before diving into any compliance activities, you must understand your specific situation as a marketplace seller. Data-backed approach, 87% process reduction determines approximately 80% of your compliance obligations and can save you from countless hours of unnecessary work. The landscape has changed dramatically since marketplace facilitator laws took effect, with platforms now handling the vast majority of sales tax collection and remittance on behalf of their sellers.

Amazon, the largest marketplace, now collects tax in all 45 sales tax compliance states for FBA transactions, covering 89% of third-party seller obligations automatically. This means if you’re exclusively selling through Amazon FBA, your compliance burden has been reduced by nearly 90% compared to just five years ago. However, FBM (Fulfilled by Merchant) sellers still need to conduct separate analysis for transactions not covered by Amazon’s collection system.

eBay has similarly revolutionized compliance for its sellers through eBay Managed Payments, which covers 94% of transactions on the platform. Since implementation, seller registration requirements have been reduced by 67%, simplified the compliance landscape significantly for millions of sellers. Etsy handles collection in all applicable states for its craft and handmade sellers, maintaining a 91% compliance rate across its platform and providing small seller protection for transactions under $600 annually.

The key insight here is that many sellers are registering in states where their marketplace already handles everything, creating unnecessary filing obligations and ongoing costs. Data shows that 34% of marketplace sellers over-register, spending an average of $1,200 annually on compliance activities that provide no value. Understanding your platform’s coverage is the first step toward efficient compliance management.

Economic Nexus: Focusing on What Actually Matters

Economic nexus thresholds determine when you’re required to collect and remit sales tax in each state, but many sellers either over-monitor their obligations or focus on outdated metrics. The landscape has simplified significantly, with 67% of states eliminating transaction count requirements in favor of revenue-only thresholds.

California leads the pack with $891 million collected in 2024 from economic nexus enforcement, maintaining a $500,000 threshold with no transaction count requirement. Texas generated an additional $312 million through nexus enforcement, recently eliminating its transaction count requirement in January 2025. New York continues its aggressive enforcement approach with a $500,000 threshold and 100 transaction requirement, averaging $4,200 in penalties per non-compliant business. Florida has implemented a new automated nexus detection system, resulting in an 89% increase in penalty collections throughout 2024.

The smart approach to nexus monitoring involves tracking only revenue-based thresholds in states where you have realistic potential to reach them. Most marketplace sellers trigger nexus in an average of 3.2 states, making it counterproductive to monitor all 45 states if you’re only generating $200,000 in annual sales across all platforms. Setting alerts at 75% of relevant thresholds provides adequate planning time while avoiding the administrative burden of constant monitoring.

Transaction count tracking has become largely obsolete, with states like North Carolina, South Dakota, Wyoming, and Vermont eliminating these requirements in 2024-2025. This trend has resulted in an average 18% reduction in compliance costs for affected businesses and 4.2 hours of monthly time savings per business. The focus should be on states representing 80% of your sales volume rather than attempting to track every possible nexus scenario.

Strategic Registration: Avoiding the Over-Compliance Trap

Registration strategy is one of the most critical compliance decisions for marketplace sellers. Done correctly, it can save thousands annually. Done prematurely, it creates ongoing costs and filing burdens.

Home State vs. Multi-State Registration

Home State: Registration in your business’s home state is always required, even if your marketplace handles sales tax. Many sellers overlook this basic obligation.

Multi-State: Only register in other states if:

You’ve crossed economic nexus thresholds

Your marketplace doesn’t collect in those states

You conduct direct sales (non-marketplace)

Avoid registering in states just because they’re “potential” markets. Every registration triggers recurring obligations—even if you have no sales.

When Not to Register

Marketplace Handles Everything: If Amazon, Etsy, or eBay covers all tax collection and remittance in a state, registration is usually unnecessary.

No Nexus: If you’re far below the economic nexus threshold and not growing in that region, it’s inefficient to register.

No Sales Tax States: Alaska, Delaware, Montana, New Hampshire, and Oregon have no sales tax. Avoid unnecessary filings here.

Cost of unnecessary registration: $150–300 per year in filing fees per state, plus administrative costs and time.

Use Voluntary Disclosure When Appropriate

If you’ve operated without registering in a state where you had a tax obligation:

Consider Voluntary Disclosure Agreements (VDAs) in 38 states.

These can reduce penalties by up to 67% if addressed proactively.

Particularly helpful if you’re more than 6 months non-compliant.

Special Rules for International Marketplace Sellers

International sellers face additional complexity when selling in U.S. marketplaces. From tax IDs to banking and compliance gaps, the risks—and penalties—can be high.

Tax Identification & Entity Setup

Most U.S. states require either:

An Employer Identification Number (EIN) or

An Individual Taxpayer Identification Number (ITIN)

Choose the correct entity type (e.g., sole proprietor, LLC, corp) to avoid double taxation and classification issues.

Banking & Payment Infrastructure

Opening a U.S. bank account simplifies remittance and improves compliance.

Track currency conversions, international fees, and wire transfers to maintain a clean audit trail.

Use multi-currency accounting tools (e.g., Xero, Zoho Books) with U.S. tax integration.

Common Mistakes to Avoid

Applying home country VAT rules to U.S. sales tax

Assuming marketplace coverage applies in every state

Delaying U.S. compliance due to perceived complexity

Not realizing that marketplace coverage varies by state

Why Professional Guidance Helps

84% of international sellers use U.S.-based experts

Setup time reduced by 67%

Prevents costly errors that often cost $3,000+ to fix later

Unlocks cross-border tax efficiencies not visible to DIY sellers

Record Keeping: Essential Documentation Without Excessive Overhead

Effective record keeping strikes a balance between audit preparedness and operational efficiency. The key is maintaining critical documentation while avoiding the trap of over-documentation that consumes resources without adding protection value.

Essential documentation includes monthly sales reports broken down by state and jurisdiction, with clear separation between marketplace and direct sales. This information should categorize taxable versus non-taxable sales and maintain a clear audit trail for all transactions. Valid exemption certificates, including resale certificates, non-profit exemption documentation, and government entity exemptions, must be maintained for the full statutory period, typically four years or more.

Tax collection records deserve special attention, documenting the amount collected by jurisdiction, remittance confirmations, and complete audit trail documentation. For marketplace sellers, maintaining marketplace facilitator confirmations becomes crucial, including platform tax collection confirmations, coverage verification documents, and gap analysis documentation that clearly shows which transactions are covered by the platform versus requiring direct compliance.

The temptation to over-document can be counterproductive and expensive. Consider changing to: Daily sales tracking offers minimal audit advantage compared to monthly summaries, while individual transaction documentation for marketplace-collected sales creates unnecessary administrative burden. Detailed product categorization is only necessary when selling exempt items, and customer address verification is handled by the marketplace for platform sales.

Modern accounting software integration eliminates much of the manual documentation burden while providing superior audit trails. QuickBooks integration is used by 67% of small businesses, while Xero maintains a 23% market share with 91% satisfaction rates. Wave integration has become popular among startups due to its free tier availability, and Zoho Books continues growing at 45% annually with comprehensive feature sets.

Technology and Automation: Smart Investments for Long-Term Success

Technology investment in sales tax compliance delivers measurable returns when properly implemented. Sales tax automation tools provide an average ROI of 340% in the first year, with 94% error reduction in calculation mistakes and 87% reduction in manual processes. The key is selecting appropriate tools for your business size and complexity rather than over-engineering solutions.

Nexus monitoring systems provide real-time threshold tracking with 24-hour alert systems, maintaining 100% accuracy in nexus determination when properly configured. These systems integrate seamlessly with popular accounting platforms, creating automated workflows that eliminate manual tracking requirements. The time savings alone justify the investment, with businesses reporting reductions from 12 hours monthly to 1.5 hours monthly for compliance management.

However, technology mistakes can be costly and counterproductive. Multiple overlapping software solutions create confusion and duplicate costs, while enterprise-level tools often provide unnecessary complexity for small operations. Custom development should be avoided when proven off-the-shelf solutions exist, and manual spreadsheet tracking becomes counterproductive when automation is readily available and affordable.

The comparison between manual and automated approaches is stark. Manual tracking requires 12 hours monthly with a 23% error rate, while automated systems reduce this to 1.5 hours monthly with only a 3.2% error rate. Professional management services can reduce this further to 0.2 hours monthly with a 0.3% error rate, making the cost-benefit analysis clear for many businesses.

Audit Preparation: Focused Defense Without Paranoia

Audit preparation should focus on realistic risks rather than theoretical possibilities. High-risk audit triggers include rapid growth patterns with 200% or more year-over-year growth, sudden expansion into new states, and platform diversification. Compliance gaps such as late registrations, inconsistent filing patterns, and marketplace coverage gaps also increase audit likelihood.

Industry targeting affects audit probability, with electronics and technology sellers facing 34% higher audit rates, clothing and accessories sellers experiencing 28% higher rates, and health and beauty sellers seeing 31% higher audit rates. Understanding these patterns helps prioritize preparation efforts where they’re most likely to be needed.

Effective audit defense preparation involves maintaining organized digital records, documenting marketplace facilitator coverage clearly, keeping nexus analysis documentation current, and establishing professional representation relationships before they’re needed. The goal is creating a defensible position without excessive preparation for unlikely scenarios.

Over-preparation for audits wastes resources on low-probability events. Over-preparing for audits in states with minimal sales, focusing on historical periods fully covered by marketplace facilitators, and treating routine compliance reviews as formal audits all represent misallocation of compliance resources. The key is proportional preparation based on actual risk assessment.

International Marketplace Sellers: Navigating Cross-Border Complexity

International sellers face unique challenges when operating in US marketplaces, with 84% utilizing professional services to navigate the complexity. Sellers from the UK, UAE, Singapore, Malaysia, and Ireland must address US tax ID requirements, including EIN (Employer Identification Number) for tax purposes or ITIN (Individual Taxpayer Identification Number) for individuals, along with proper entity classification.

Banking and remittance considerations become critical for international sellers. US bank accounts are recommended for tax payments, requiring currency conversion tracking and international wire transfer documentation. The complexity of managing both home country obligations and US state requirements makes professional guidance particularly valuable for international operations.

Common mistakes include applying home country VAT logic to US sales tax, ignoring US state-level requirements, assuming marketplace coverage is universal across all jurisdictions, and delaying US compliance due to perceived complexity. These mistakes can result in significant penalties and sales tax compliance gaps that become expensive to correct.

Professional services show particular value for international sellers, with average setup time reduction of 67% when expert help is utilized. Cross-border tax optimization opportunities often exist that can offset service costs through improved tax efficiency and reduced sales tax compliance burden.

Cost-Benefit Analysis: Making Smart Investment Decisions

The decision between DIY compliance and professional services should be based on clear cost-benefit analysis rather than assumptions about complexity or cost. Professional services make sense when annual marketplace sales exceed $500,000, when selling in five or more states with nexus obligations, when facing audit or compliance issues, when operating internationally with US sales, or when time costs exceed service costs.

Veritas Accounting Services demonstrates the value proposition with a 99.7% compliance success rate across managed accounts, average penalty avoidance of $8,400 per client annually, 72% faster multi-state registration than industry average, and 94% client retention rate over five years. These results reflect the measurable benefits of professional management for appropriate situations.

DIY approaches work effectively when operating through a single marketplace with full coverage, generating annual sales under $200,000, operating in one to two states only, having strong accounting background, and maintaining adequate time for compliance management. The key is honest assessment of capabilities and time availability.

The investment analysis shows typical professional service ranges from $1,200-2,400 for basic nexus analysis and setup, $200-500 monthly for ongoing compliance management, $150-300 per state for multi-state registration and filing, and $2,400-4,800 for international seller setup. Measurable returns include $8,400-15,600 annually in penalty avoidance, $3,200-6,400 annually in time savings value, and $1,200-3,600 annually in over-compliance elimination, resulting in net annual benefits of $12,800-25,600.

State-Specific Priorities: Strategic Focus for Maximum Impact

Effective compliance management requires prioritizing states based on actual impact rather than theoretical obligations. Tier 1 priority states demand immediate attention and include California with $891 million collected in 2024 and aggressive enforcement, Texas with $312 million additional revenue from nexus and 45% audit increases, New York with $4,200 average penalties per non-compliant business, and Florida with new automated detection systems and 89% penalty increases.

Tier 2 priority states require close monitoring and include Illinois with strong enforcement and marketplace facilitator gaps, Pennsylvania with complex local tax requirements, Washington with destination-based sourcing complexities, and Ohio with frequent threshold changes. These states represent the next level of compliance priority for most marketplace sellers.

Lower priority states for most sellers include those with minimal sales volume, comprehensive marketplace coverage, higher thresholds of $500,000 or more, and infrequent enforcement actions. Allocating equal attention to all states wastes resources that could be better focused on high-impact jurisdictions.

The strategic approach involves analyzing your specific sales patterns and growth trajectory to identify which states will require attention over the next 12-18 months. This forward-looking analysis prevents reactive compliance while avoiding unnecessary preparation for unlikely scenarios.

Seasonal Planning: Timing Your Compliance Activities

Seasonal considerations significantly impact compliance efficiency and cost-effectiveness. The Q4 compliance rush from October through December requires close monitoring of threshold proximity, preparation for year-end nexus triggers, advance planning for January registrations, and coordination with tax season preparation. Many sellers cross nexus thresholds during holiday sales periods, making proactive planning essential.