Receiving a lump-sum Social Security payment often brings relief, especially after months or years of waiting for approval. But that relief is frequently followed by confusion—and sometimes fear—once clients realize taxes may apply.

For the 2026 filing season, the tax rules for lump-sum Social Security benefits remain largely unchanged. However, clearer IRS reporting guidance and ongoing income pressures make understanding these rules more important than ever. With the right approach, a lump-sum payment does not have to result in a tax shock.

What Are Lump-Sum Social Security Benefits?

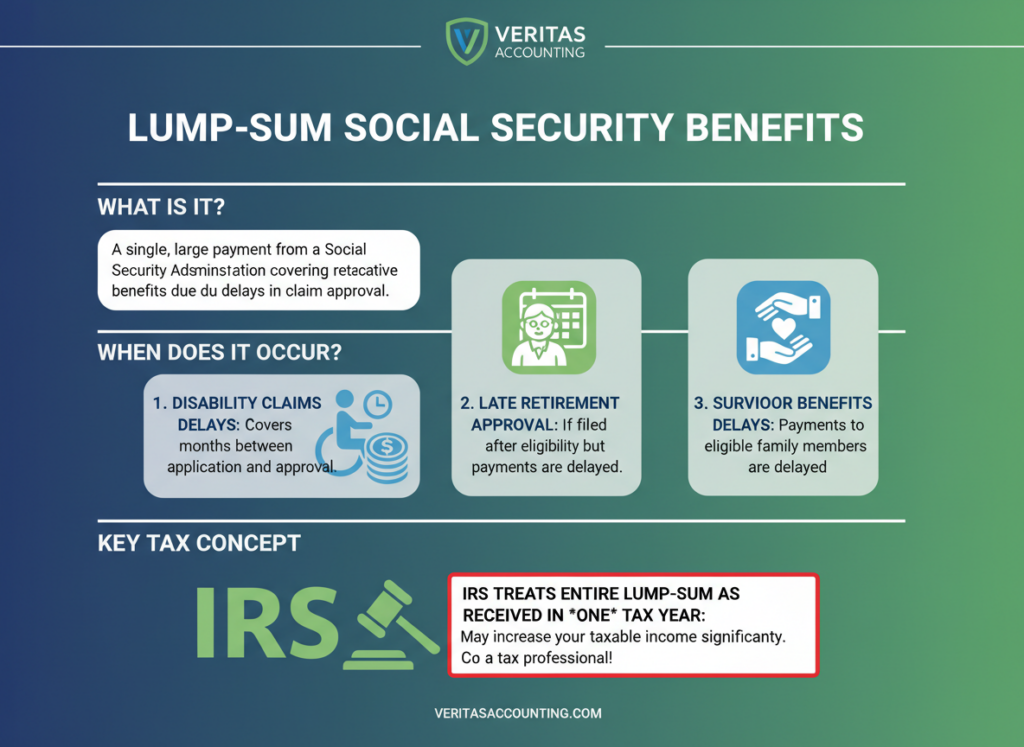

Lump-sum Social Security benefits occur when the Social Security Administration approves benefits retroactively and pays multiple months or years of missed benefits in a single check.

This most often happens with:

Disability claims delayed by appeals

Retirement benefits approved late

Survivor benefits processed after administrative delays

Although the payment covers prior periods, the IRS treats the entire amount as received in one tax year, which is where most confusion begins.

How Lump-Sum Social Security Benefits Are Taxed

The IRS requires taxpayers to report all Social Security benefits in the year they are received, even when those benefits relate to earlier years. This includes lump-sum Social Security benefits paid retroactively.

However, taxpayers are not required to amend prior-year tax returns. Instead, the tax law provides a special calculation designed to prevent unfair tax spikes.

This distinction is critical. Reporting does not automatically mean the entire payment is taxed at once.

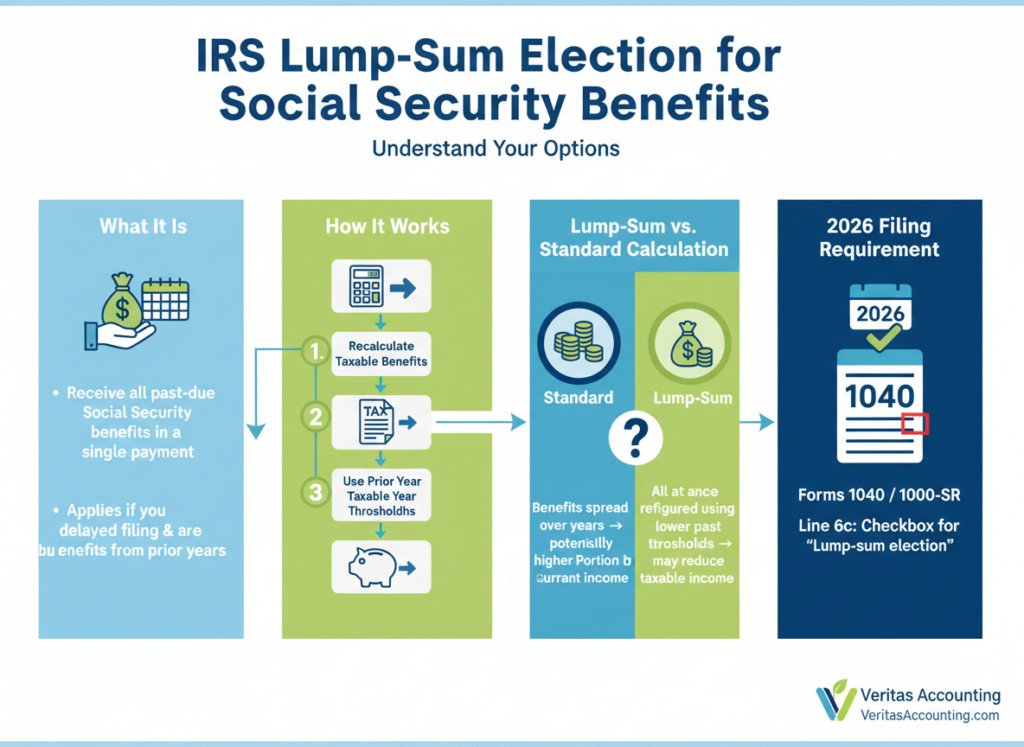

Using the Lump-Sum Election for Social Security Benefits

To address retroactive payments, the IRS allows a special calculation known as the lump-sum election for Social Security benefits.

This method allows taxpayers to:

Recalculate how much of the benefits would have been taxable in the prior year(s)

Use the income thresholds that applied in those years

Carry forward only the taxable portion into the current return

If this method produces a lower taxable amount, the taxpayer may use it. If it does not, the standard calculation applies instead.

For 2026 filings, Forms 1040 and 1040-SR now include a checkbox on Line 6c to indicate that the lump-sum election was used. While no separate form is required, this checkbox helps document the calculation and improves return clarity.

Why Lump-Sum Social Security Benefits Trigger Tax Confusion

Many clients believe Social Security taxation thresholds increase with inflation. They do not.

The thresholds remain frozen at:

$25,000 and $34,000 for single filers

$32,000 and $44,000 for married filing jointly

Once combined income exceeds these levels, up to 50% and eventually 85% of Social Security benefits may be taxable. A lump-sum Social Security payment can temporarily push income above these limits, making careful calculation essential.

Multiple Years, Multiple Lump-Sum Calculations

When lump-sum Social Security benefits cover more than one prior year, the special calculation may be applied separately to each year included in the payment.

This is common in disability cases that span multiple years. Accurate prior-year income records and careful review of Form SSA-1099 are critical to applying the rules correctly.

Tax professionals should confirm:

Which years are included

Filing status for each year

Income levels that affect benefit taxation

Special Issues With Disability Lump-Sum Social Security Benefits

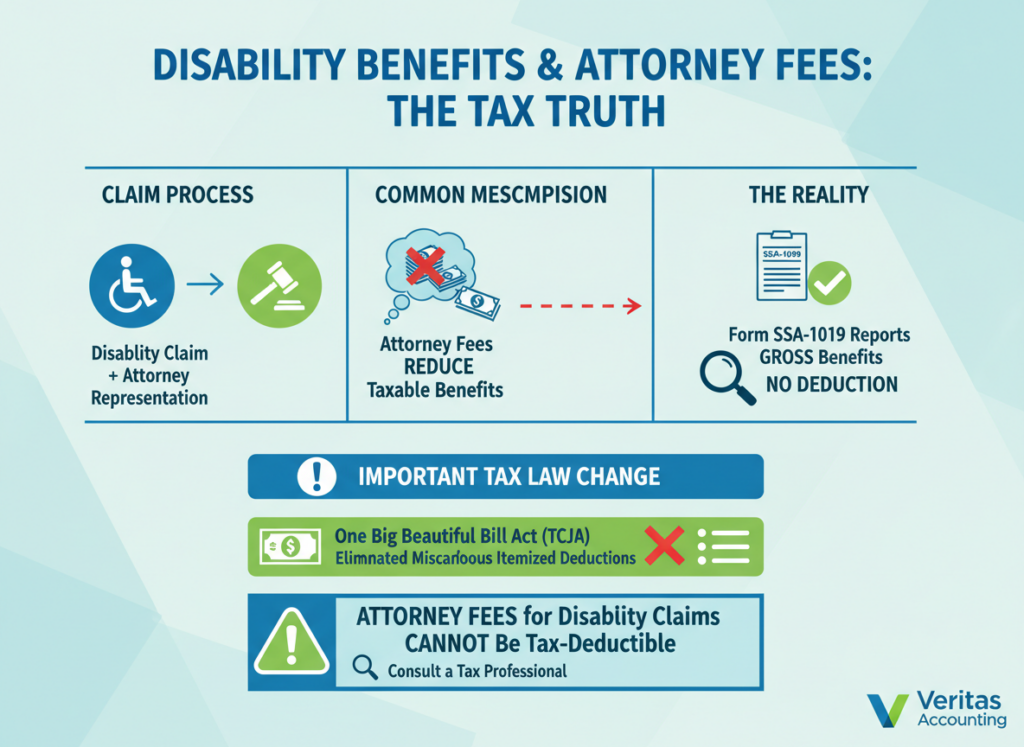

Disability claims often involve attorney representation. Clients frequently assume attorney fees reduce taxable Social Security benefits. They do not.

Social Security reports gross benefits before attorney fees on Form SSA-1099. Under the One Big Beautiful Bill Act (OBBBA), miscellaneous itemized deductions are permanently suspended, meaning attorney fees no longer reduce taxable income.

Clients should be prepared for this outcome to avoid unpleasant surprises.

What Tax Professionals Should Explain About Lump-Sum Social Security Benefits

Reassurance is essential. A lump-sum Social Security payment does not automatically mean higher taxes.

Proper reporting can significantly reduce taxable benefits

Handled correctly, lump-sum Social Security benefits become a planning opportunity rather than a problem.

Planning Beyond the Lump-Sum Payment

Discussing lump-sum Social Security benefits often leads to broader planning conversations, including:

Voluntary withholding on Social Security

Estimated tax payments

Medicare premium surcharges

Coordinating Social Security with pensions or retirement accounts

These conversations strengthen long-term client relationships and reinforce the advisor’s role as a trusted planner.

Final Takeaway

Lump-sum Social Security benefits can feel overwhelming, but the tax rules are designed to be fair. With the correct calculations, accurate reporting, and clear communication, most clients can avoid unnecessary tax stress.

For tax professionals, understanding how lump-sum Social Security benefits are taxed is a valuable way to deliver clarity, confidence, and meaningful guidance during an important financial moment.

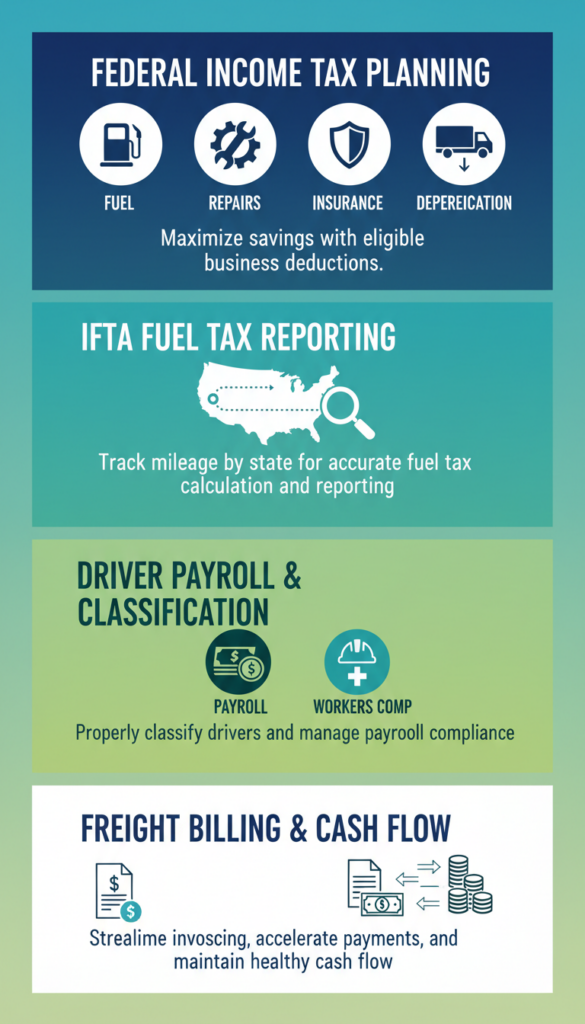

In today’s competitive freight market, smart trucking companies know that success is not driven by miles alone—it’s driven by numbers. Behind every profitable fleet is proven logistic accounting that tracks costs accurately, manages cash flow, and keeps the business compliant with US tax laws.

Rising fuel prices, multi-state operations, driver shortages, and strict IRS requirements have made financial management more complex than ever. General bookkeeping is no longer enough. Logistic accounting for trucking companies has become a critical business tool that separates struggling fleets from consistently profitable ones.

This guide explains how proven logistic accounting helps trucking businesses control costs, reduce tax risk, and build long-term financial stability.

What Is Logistic Accounting for Trucking Companies?

Logistic accounting is a specialized form of accounting focused on the financial activities involved in transporting goods. For trucking companies, it goes far beyond recording income and expenses. It tracks how money moves across every mile, load, and route.

Unlike standard accounting, logistic accounting for trucking companies focuses on:

Cost per mile and cost per load

Fuel, tolls, and maintenance tracking

Driver payroll and compliance

Fleet asset depreciation

Freight billing and collections

Multi-state tax exposure

When applied correctly, proven logistic accounting gives trucking owners real visibility into profitability instead of relying on assumptions.

Trucking operates on thin margins. A small error in fuel tracking, depreciation, or billing can quietly erase profits.

Smart trucking companies use proven logistic accounting to:

Identify unprofitable routes

Control fuel and maintenance costs

Prevent freight invoice overpayments

Improve cash flow timing

Reduce audit and penalty risk

Without structured logistic accounting, many trucking businesses underprice services, miss deductions, or discover losses too late to fix them.

The Role of Proven Logistic Accounting in Cost Control

Tracking Cost per Mile Accurately

Cost per mile is one of the most important metrics in trucking. Proven logistic accounting ensures that all variable and fixed costs—fuel, insurance, repairs, permits, driver wages—are allocated correctly.

This allows trucking companies to:

Price loads correctly

Negotiate better contracts

Decide when routes should be dropped

Fuel Cost Management

Fuel is often the largest expense. Logistic accounting reconciles:

Fuel card transactions

Mileage logs

Fuel surcharges

Accurate fuel tracking also supports IFTA fuel tax reporting, reducing errors and penalties.

Proven logistic accounting is no longer optional for trucking businesses that want to grow profitably and stay compliant. It provides the financial clarity needed to control costs, reduce tax risk, and make confident decisions.

Smart trucking companies don’t guess—they win with data, discipline, and proven logistic accounting.

If you want to turn your trucking operation into a financially strong, tax-compliant business, the right accounting strategy makes all the difference.

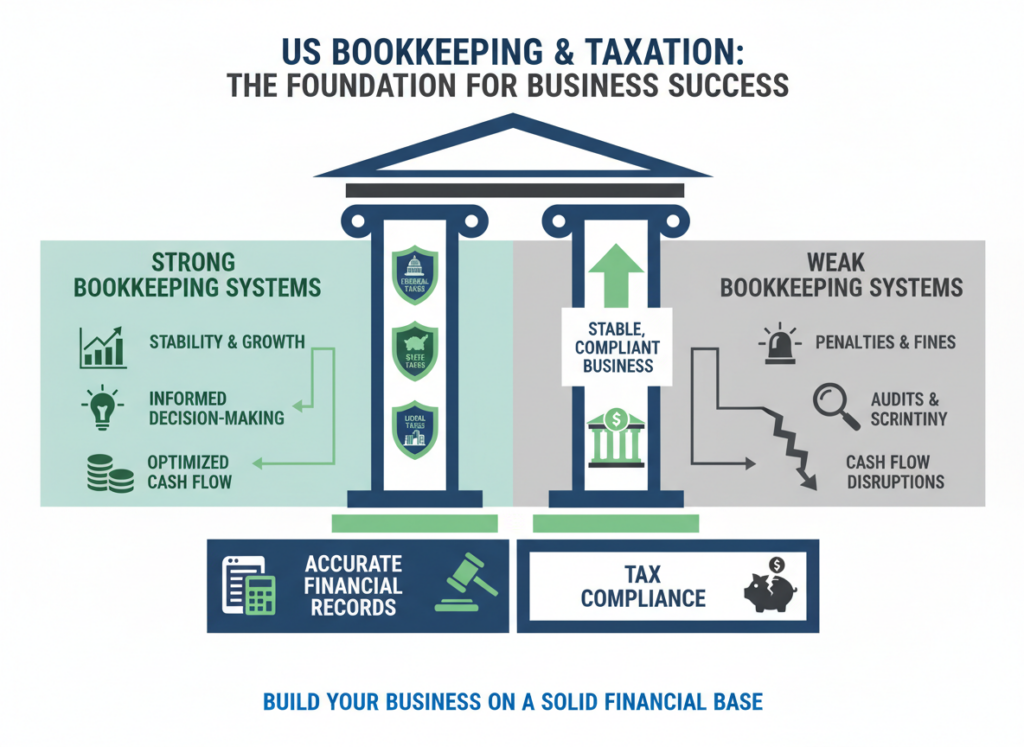

US bookkeeping and taxation are the foundation of every compliant and financially stable business operating in the United States. Regardless of size or industry, businesses are expected to maintain accurate financial records and meet federal, state, and local tax obligations on time. When bookkeeping systems are weak or tax rules are misunderstood, the consequences can include penalties, audits, cash flow disruptions, and poor financial decisions.

Understanding how US bookkeeping and taxationwork together allows business owners to stay compliant, plan effectively, and make informed decisions throughout the year—not just at tax time.

Why US Bookkeeping and Taxation Are Closely Connected

Bookkeeping and taxation are often discussed separately, but in practice they are inseparable. Every tax return filed with the IRS is built on bookkeeping data. If transactions are recorded incorrectly or not supported with documentation, tax filings will also be inaccurate.

Strong US bookkeeping and taxation practices ensure that income is reported correctly, deductions are supported, and tax liabilities are calculated accurately. Businesses that invest in clean bookkeeping experience fewer surprises and smoother interactions with tax authorities.

Core Bookkeeping Requirements for US Businesses

Accurate recordkeeping is the backbone of US bookkeeping and taxation. At a minimum, businesses must maintain:

A structured chart of accounts

Detailed records of income and expenses

Bank and credit card reconciliations

Accounts receivable and payable tracking

Supporting documents such as invoices and receipts

These records support financial statements and form the basis for all tax filings. Without disciplined bookkeeping, even well-intentioned businesses can fall out of compliance.

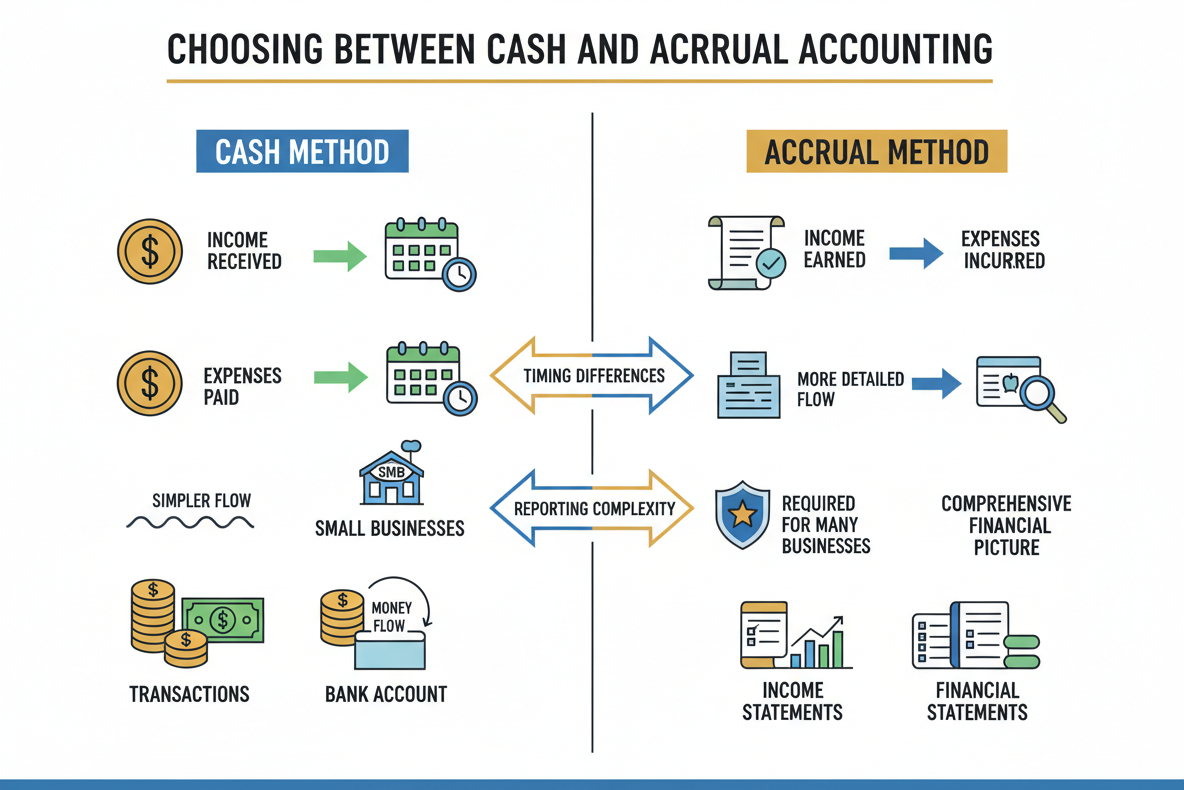

The accounting method used directly impacts US bookkeeping and taxation. Most small businesses choose between cash and accrual accounting.

Cash method: Income is recorded when received, and expenses when paid. This method is simpler and often used by small businesses.

Accrual method: Income and expenses are recorded when earned or incurred, regardless of cash movement. This method provides a more accurate financial picture and is required for many businesses.

Once selected, the accounting method must be applied consistently and may require IRS approval to change.

Federal Tax Responsibilities Businesses Must Manage

Federal tax compliance is a critical component of US bookkeeping and taxation. Depending on the business structure, obligations may include:

Income tax (corporate or pass-through)

Self-employment tax

Payroll taxes (Social Security and Medicare)

Federal unemployment tax (FUTA)

Accurate bookkeeping ensures these taxes are calculated correctly and paid on time. Missed or underpaid federal taxes can quickly lead to penalties and interest.

In addition to federal obligations, US bookkeeping and taxation include state and local requirements that vary by jurisdiction. These may involve:

State income or franchise taxes

Sales and use tax

State payroll taxes

Local business taxes or licenses

Businesses operating in multiple states must monitor nexus rules and ensure proper registration and filing in each applicable state.

Sales Tax Tracking and Reporting

Sales tax compliance has become more complex due to economic nexus rules. Businesses must track where they have sales tax obligations and accurately record taxable and exempt transactions.

Proper US bookkeeping and taxation practices include:

Separating taxable and non-taxable sales

Tracking collected sales tax separately

Reconciling sales tax payable accounts

Errors in sales tax reporting can result in assessments, penalties, and costly audits.

Payroll Bookkeeping and Tax Compliance

Payroll is one of the highest-risk areas in US bookkeeping and taxation. Employers must calculate wages accurately, withhold the correct taxes, and remit payments to federal and state agencies.

Key payroll tax obligations include:

Federal income tax withholding

Social Security and Medicare taxes

State income tax withholding

Quarterly and annual payroll filings

Worker misclassification is a common compliance issue that can trigger audits and penalties.

Expense Classification and Deductibility

Correct expense categorization plays a major role in US bookkeeping and taxation. While many business expenses are deductible, some are subject to limits or special rules.

Common areas requiring attention include:

Meals and entertainment expenses

Vehicle and travel costs

Home office deductions

Asset capitalization and depreciation

Well-maintained books allow businesses to claim legitimate deductions while avoiding aggressive positions that could raise red flags.

Record Retention and IRS Documentation Standards

The IRS requires businesses to retain financial records for several years. Strong US bookkeeping and taxation practices include maintaining:

Bank statements and reconciliations

Receipts and invoices

Payroll records

Tax returns and supporting schedules

Proper documentation supports tax positions and simplifies responses to IRS inquiries or audits.

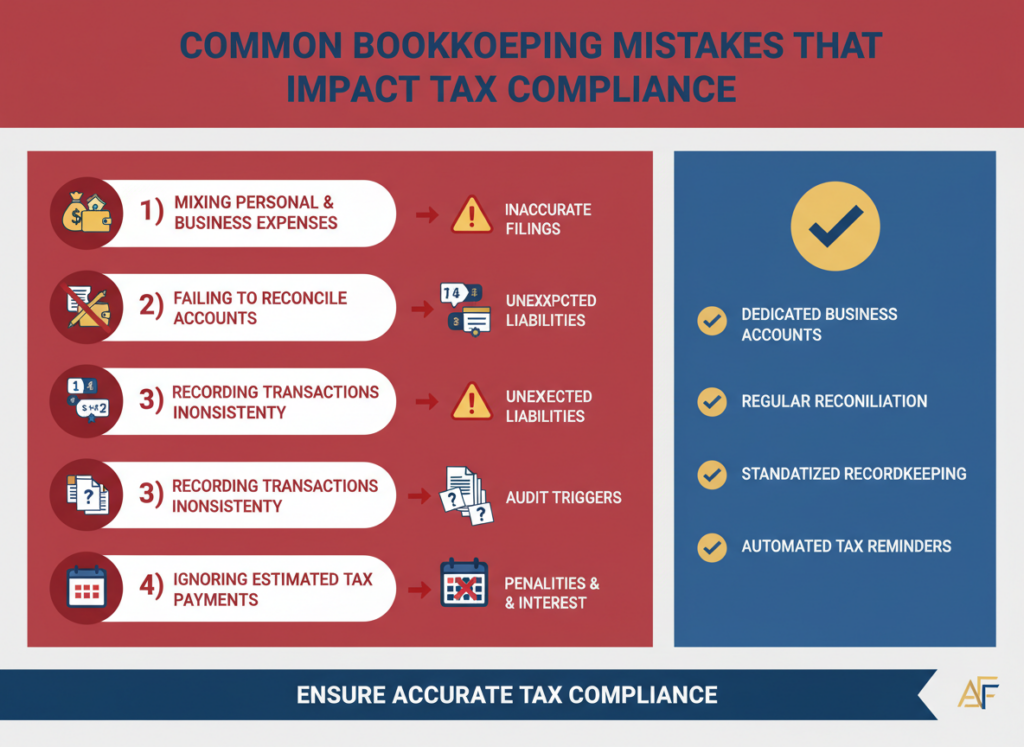

Common Bookkeeping Mistakes That Impact Tax Compliance

Several recurring errors undermine US bookkeeping and taxation, including:

Mixing personal and business expenses

Failing to reconcile accounts regularly

Recording transactions inconsistently

Ignoring estimated tax payments

These mistakes often result in inaccurate tax filings and unexpected liabilities.

The Value of Professional Bookkeeping and Tax Support

Many businesses rely on professional services to manage US bookkeeping and taxation effectively. Experienced professionals help ensure accuracy, consistency, and compliance while identifying opportunities for tax efficiency.

Outsourcing or hiring qualified support allows business owners to focus on growth while reducing compliance risks.

Year-End Bookkeeping and Tax Preparation

Year-end is a critical period for US bookkeeping and taxation. Closing the books properly ensures that financial statements are accurate before tax returns are prepared.

Key year-end tasks include:

Reconciling all accounts

Reviewing income and expense classifications

Confirming depreciation and asset records

Preparing tax-ready financial statements

Strong year-end processes reduce stress and improve tax outcomes.

Final Takeaway

US bookkeeping and taxation are not just compliance requirements—they are essential tools for financial clarity and business success. Accurate bookkeeping supports reliable tax reporting, while proactive tax planning depends on clean financial data.

Businesses that get the fundamentals right reduce risk, improve decision-making, and stay compliant with IRS and state regulations. By prioritizing strong bookkeeping systems and understanding tax obligations, companies can operate with confidence and build a solid foundation for long-term growth.

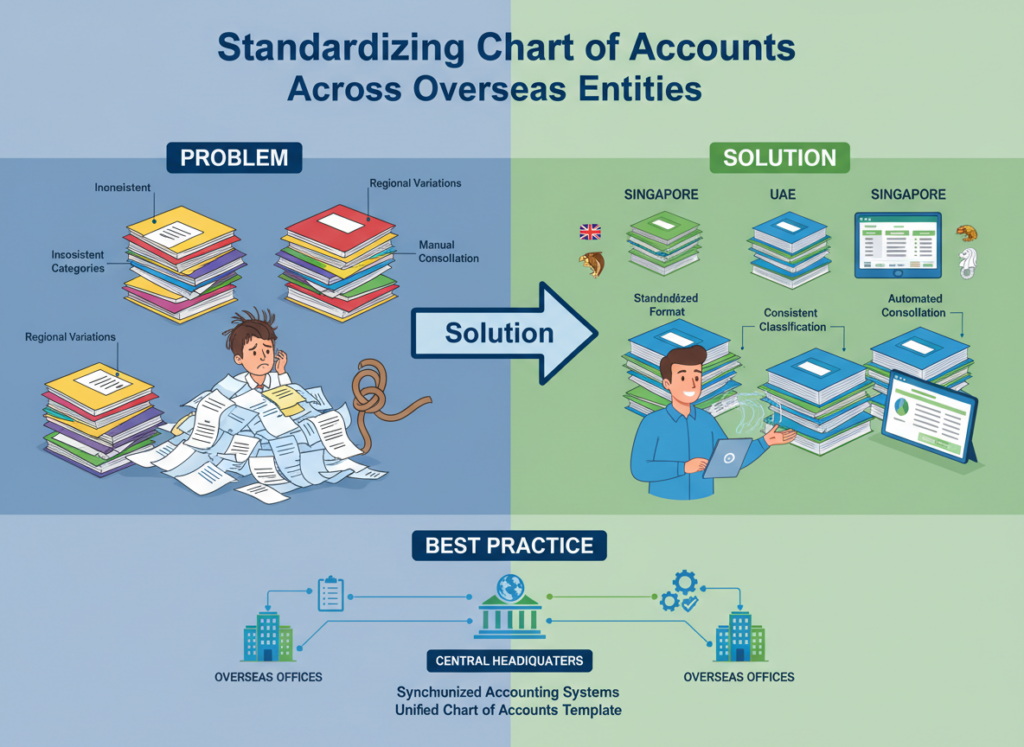

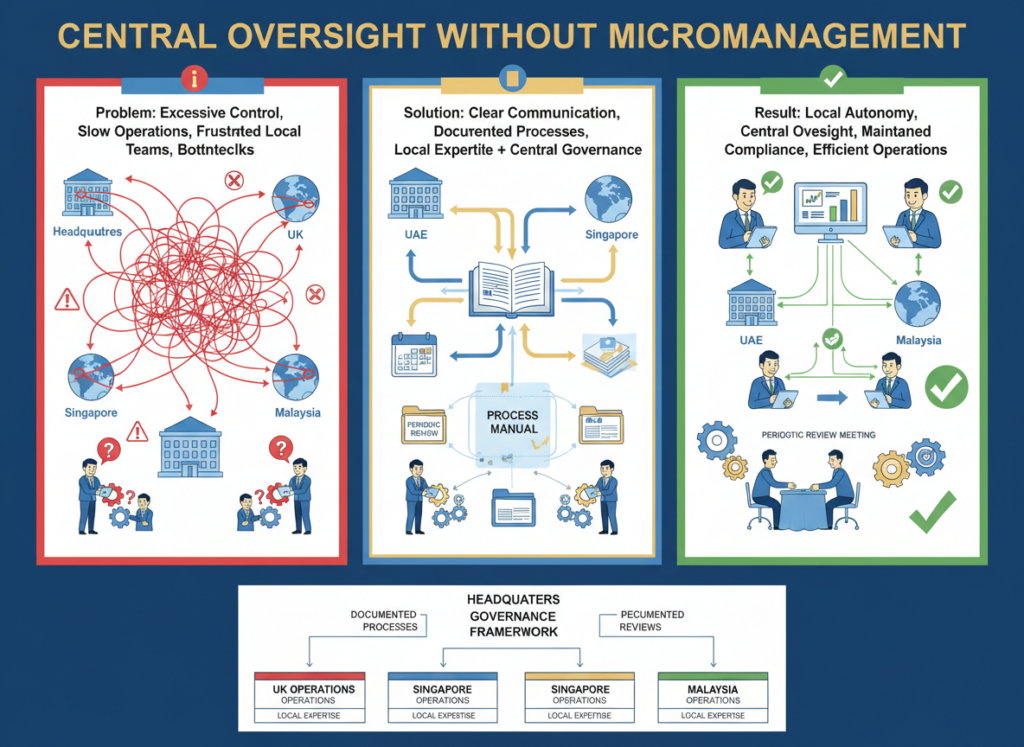

Managing overseas books of accounts has become a standard requirement for businesses operating across borders. Whether companies expand through foreign subsidiaries, offshore teams, or international branches, maintaining accurate and compliant financial records in multiple jurisdictions is no longer optional—it is critical to sustainable growth.

Unlike domestic accounting, overseas books of accounts bring added layers of complexity, including different accounting standards, currencies, tax laws, and reporting deadlines. Without strong oversight, even small bookkeeping gaps can lead to regulatory penalties, audit delays, and unreliable consolidated financial statements. Understanding where the risks lie is the first step toward managing them effectively.

Why Overseas Books of Accounts Require Stronger Oversight

Domestic bookkeeping already demands discipline, but overseas books of accounts require additional structure and monitoring. Local accounting practices may differ significantly from group-level expectations, and time zone differences often slow communication.

Many businesses assume that outsourcing overseas bookkeeping transfers compliance responsibility. In reality, accountability always rests with the parent company. Errors in overseas records can affect group financials, tax filings, and investor reporting, making proactive oversight essential.

One of the most common issues in overseas books of accounts is inconsistency in chart of accounts design. Local teams may categorize expenses and revenues based on regional norms, which may not align with head-office reporting requirements.

Without standardization, consolidating financials becomes manual and error-prone. Misclassified expenses or inconsistent balance sheet groupings can distort performance analysis.

Best practice: Implement a standardized chart of accounts across all overseas entities, allowing limited flexibility only where local statutory reporting requires it. This ensures consistency without compromising compliance.

Managing Multi-Currency Transactions Accurately

Currency management is a core challenge when handling overseas books of accounts. Improper application of exchange rates is one of the most frequent causes of financial misstatements.

Key risk areas include:

Incorrect functional currency selection

Inconsistent exchange rate usage

Improper recognition of foreign exchange gains or losses

Even small inconsistencies can materially impact profitability and balance sheet accuracy.

Best practice: Establish clear policies for exchange rate usage and ensure uniform application across all overseas bookkeeping teams.

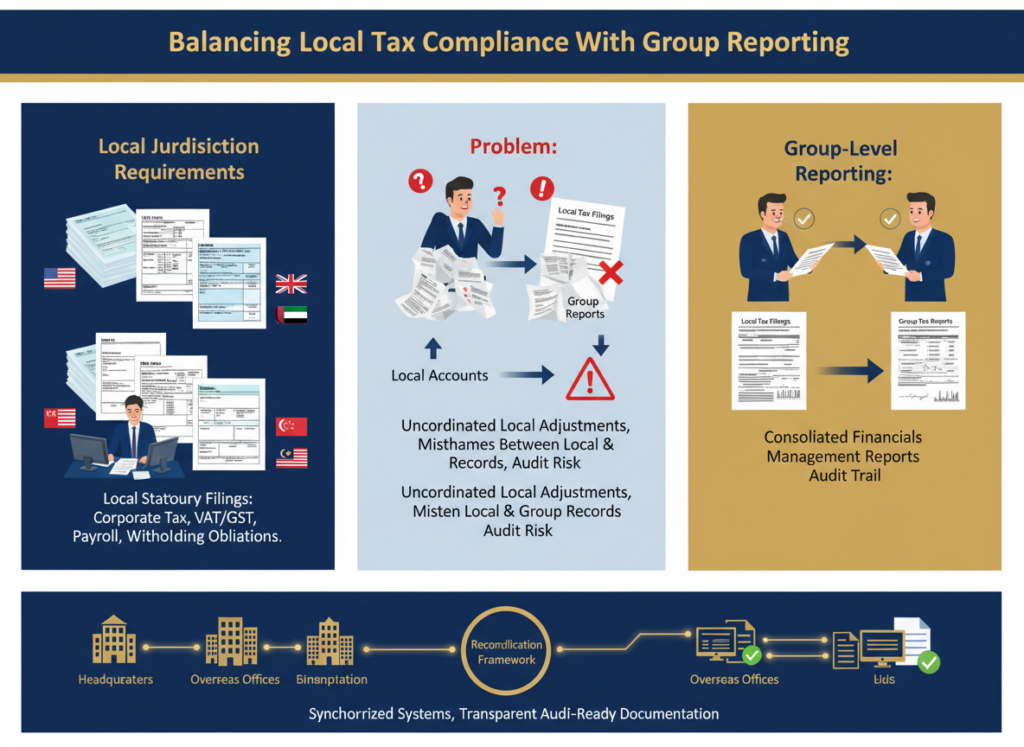

Each jurisdiction imposes its own corporate tax, VAT/GST, payroll, and withholding obligations. Overseas books of accounts must support both local statutory filings and group-level reporting.

Problems often arise when local tax adjustments are booked without informing the parent company. This creates mismatches between local accounts, management reports, and consolidated financials.

Best practice: Require reconciliations between local tax filings and group financial records, ensuring transparency and audit readiness.

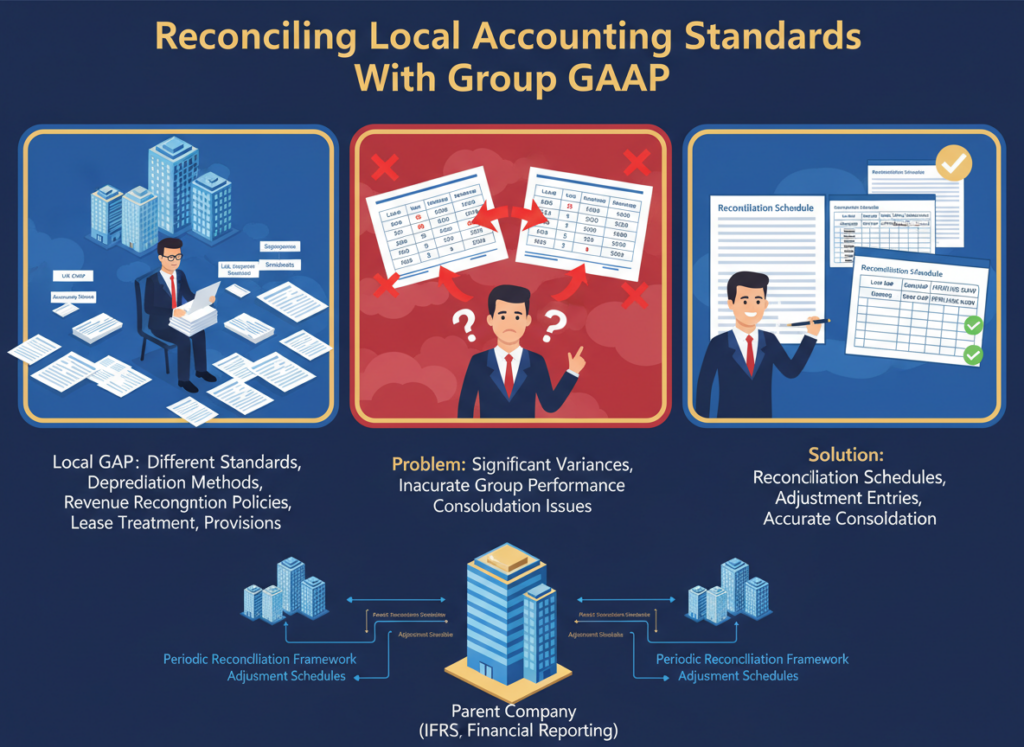

Overseas entities may prepare financials under local GAAP, while the parent company reports under IFRS or US GAAP. Differences in depreciation methods, revenue recognition, leases, or provisions can create significant variances.

If these differences are not adjusted during consolidation, overseas books of accounts may not accurately reflect group performance.

Best practice: Prepare periodic reconciliation schedules bridging local accounting standards to group reporting frameworks.

Payroll and Employment Compliance Risks

Payroll is one of the highest-risk areas in overseas books of accounts. Each country has unique labor laws, social security requirements, and payroll tax rules.

Common risks include:

Misclassification of employees and contractors

Underpayment of social contributions

Payroll records not matching accounting entries

Payroll errors often attract immediate regulatory scrutiny and penalties.

Best practice: Reconcile payroll data monthly with general ledger records and review payroll compliance centrally.

Intercompany Transactions and Transfer Pricing Controls

Intercompany transactions are unavoidable in overseas books of accounts. Management fees, royalties, cost allocations, and inventory transfers must be properly documented and priced at arm’s length.

Unreconciled intercompany balances delay month-end close and increase audit risk. Poor documentation can also trigger transfer pricing audits.

Best practice: Formalize intercompany agreements, apply consistent pricing methodologies, and reconcile balances regularly across entities.

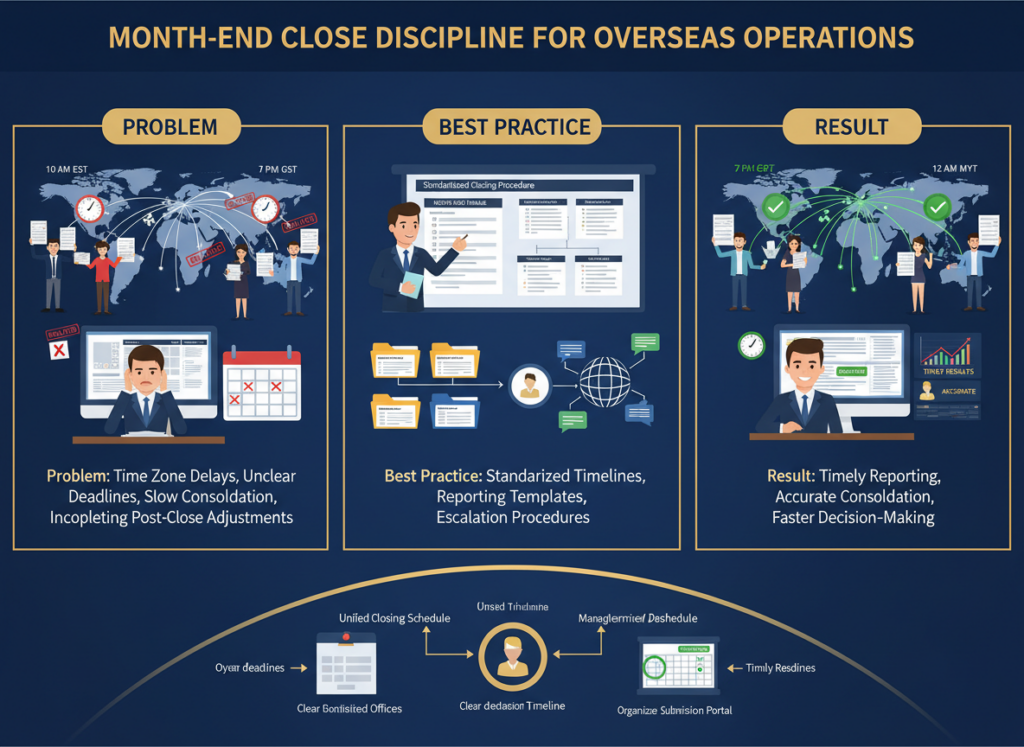

Delayed reporting from overseas teams is a common challenge. Time zone differences and unclear deadlines often slow down consolidation.

Incomplete or rushed reporting undermines decision-making and increases the risk of post-close adjustments.

Best practice: Set standardized closing timelines, reporting templates, and escalation procedures for all overseas entities.

Internal Controls and Review Frameworks

Weaker oversight increases the risk of errors or fraud in overseas books of accounts. Limited segregation of duties, poor approval processes, or unrestricted system access can compromise financial integrity.

Best practice: Implement internal control checklists, approval workflows, and periodic internal reviews to strengthen governance.

Audit Readiness and Documentation Management

Audits involving overseas books of accounts often fail due to missing documentation or inconsistent audit trails. Poor recordkeeping extends audit timelines and increases costs.

Best practice: Maintain organized digital documentation, including invoices, contracts, bank statements, and tax filings, accessible to both local and central teams.

Technology and System Integration

Using different accounting systems across countries creates silos and increases manual work. Data inconsistencies during consolidation are a common outcome.

Best practice: Adopt centralized accounting platforms where possible, or standardize data exports and validation processes.

Successful management of overseas books of accounts requires balancing local expertise with central governance. Local teams handle regulatory nuances, while head-office oversight ensures consistency and compliance.

Clear communication, documented processes, and periodic reviews help maintain control without slowing operations.

Final Takeaway

Managing overseas books of accounts is not just a bookkeeping exercise—it is a strategic compliance responsibility. Errors in overseas records can ripple across tax filings, audits, and consolidated reporting.

By focusing on standardization, strong controls, tax alignment, and proactive oversight, businesses can reduce compliance risks and build reliable global financial systems. As international operations grow, disciplined management of overseas books of accounts becomes essential to accuracy, transparency, and long-term success.

Business entity selection is one of the most impactful decisions a business owner can make, yet it is often left untouched for years. As 2025 draws to a close and the tax landscape prepares for meaningful changes in 2026, year-end planning offers a critical opportunity to reassess whether a company’s current structure still supports its financial, tax, and long-term goals.

Entity selection affects far more than tax rates. It shapes how income is taxed, how losses are used, how compensation is structured, and how a business prepares for growth, retirement, or succession. A thoughtful review before year-end allows tax professionals and business owners to align structure with strategy—before deadlines pass and options narrow.

Why Business Entity Selection Matters at Year-End

Year-end is when income levels become clear, ownership changes are finalized, and planning for the coming year begins. This timing makes business entity selection especially important. Decisions made now can influence tax outcomes not only for the current year but well into 2026 and beyond.

Expected rate adjustments, evolving compliance requirements, and shifting business goals mean that a structure that worked in prior years may no longer be optimal. Reviewing entity choice at year-end allows advisors to identify whether staying the course makes sense or whether restructuring could deliver meaningful tax or operational benefits.

Understanding Business Entity Selection Across Common Structures

Effective business entity selection requires understanding how each entity type operates under current law and how it may be affected by upcoming changes.

C Corporations

C corporations offer a flat corporate tax rate and a familiar legal framework. They are often well-suited for businesses that plan to reinvest profits, pursue outside investors, or prepare for equity-based growth. However, double taxation remains a central consideration. Profits taxed at the corporate level may be taxed again when distributed to shareholders, which can reduce overall tax efficiency for owners seeking regular distributions.

S Corporations

S corporations provide pass-through taxation while allowing flexibility in managing compensation and distributions. For many closely held businesses, this balance can be attractive. That said, eligibility rules—such as limits on shareholders, ownership restrictions, and the single-class-of-stock requirement—must be reviewed regularly. Reasonable compensation remains a key compliance issue and should be part of any year-end evaluation.

Partnerships and Multi-Member LLCs

Partnerships and multi-member LLCs offer the greatest flexibility in business entity selection. Special allocations, tiered ownership, and customized economic arrangements make them ideal for complex or evolving businesses. However, this flexibility comes with added administrative responsibility, including basis tracking, capital account maintenance, and careful handling of self-employment tax exposure.

How Business Entity Selection Impacts Tax Outcomes

Choosing the right entity structure affects how income and losses flow to owners. As income increases or business activity shifts, the tax efficiency of one entity compared to another can change significantly.

Year-end planning allows professionals to model how 2026 tax rules may affect pass-through income, corporate earnings, or owner compensation. A structure that minimizes tax under current conditions may become less favorable as thresholds, rates, or limitations change.

Year-End Planning Tools That Affect Business Entity Selection

Several planning tools can influence business entity selection, but many come with strict timing requirements. Late S elections, check-the-box classifications, or restructuring transactions may be available only if action is taken before year-end or within specific election windows.

Missing these deadlines can delay a desired strategy by an entire year, potentially resulting in higher taxes or lost planning opportunities. Reviewing entity options before year-end ensures that clients do not miss critical elections that could support their 2026 objectives.

Business Entity Selection and Long-Term Planning Goals

Entity choice does not exist in isolation. Business entity selection interacts closely with retirement planning, succession strategies, and compensation design.

A business planning for a future sale or generational transfer may benefit from the flexibility offered by partnership structures. Owners seeking to maximize retirement contributions may find different opportunities depending on whether they operate as an S corporation or C corporation. Evaluating entity choice with a long-term lens helps ensure that today’s structure does not limit tomorrow’s options.

Communicating Business Entity Selection Decisions to Clients

Many business owners find business entity selection confusing, especially when an LLC can be taxed in multiple ways. Clear communication is essential. Explaining how distributions, wages, basis, and compliance obligations differ between entities empowers clients to participate in the decision-making process.

When clients understand the trade-offs involved, they are more likely to feel confident in the chosen structure and committed to long-term planning strategies. Year-end conversations provide a natural opportunity to revisit these topics and reinforce proactive planning.

Preparing for 2026 Through Smart Business Entity Selection

As 2026 approaches, tax professionals should encourage clients to view business entity selection as an evolving strategy rather than a one-time decision. Economic conditions change, tax laws evolve, and business goals shift. Regular reviews ensure that entity choice remains aligned with both current operations and future plans.

Proactive evaluation at year-end allows businesses to enter the new tax year with clarity, confidence, and a structure designed to support growth and compliance.

Key Takeaway

Business entity selection is a foundational element of effective tax and business planning. Year-end offers the ideal moment to reassess whether a company’s current structure still supports its goals in light of upcoming 2026 changes.

By reviewing entity choice now—before deadlines pass—business owners and advisors can position the business for tax efficiency, operational flexibility, and long-term success. A well-timed evaluation today can prevent costly adjustments tomorrow and ensure the business is built for what lies ahead to support sustainable growth.

Final Thoughts

Business entity selection is not a decision that should be made once and forgotten. As tax laws evolve and business goals change, the structure that once worked well may no longer deliver the best results. Reviewing entity choice at year-end allows business owners to step into the next tax year with clarity, confidence, and a structure aligned to both current operations and future plans.

Taking time now to reassess entity selection can help avoid missed opportunities, reduce tax inefficiencies, and support long-term growth. A proactive review before year-end ensures that your business enters the new year prepared, compliant, and strategically positioned for what lies ahead.

The first-time abatement 2026 update marks a major shift in how the IRS administers penalty relief for taxpayers. For years, taxpayers struggled with penalty notices—many not knowing that the IRS offered a First-Time Abatement (FTA) program at all. The IRS required taxpayers or tax professionals to call, write, or file a request to receive the penalty waiver.

Starting in 2026, the IRS will automatically apply first-time abatement 2026 relief when a taxpayer qualifies. This is one of the most significant modernization steps in recent IRS history.

This blog breaks down what first-time abatement 2026 means, who qualifies, how the automatic waiver works, and what tax professionals must do to prepare.

⭐ What Is First-Time Abatement (FTA)?

First-Time Abatement (FTA) has existed since 2001 and is one of the most widely applicable forms of IRS penalty relief. FTA is available for taxpayers who have a good compliance history and need relief from certain penalties.

Under first-time abatement 2026, the IRS will shift from a request-based model to an automatic system—helping millions of taxpayers who previously missed out due to lack of awareness.

FTA applies only to penalties related to:

Failure to file

Failure to pay

Failure to deposit (for payroll taxes)

These penalties can be substantial, and first-time abatement 2026 may prevent financially strained taxpayers from paying unnecessary penalties.

📌 Penalties Eligible Under First-Time Abatement 2026

FTA continues to apply to only three penalty categories. Under the first-time abatement 2026 system, these penalties will be reviewed automatically:

✔ Failure to File Penalty

Assessed when a taxpayer submits a return after the due date.

✔ Failure to Pay Penalty

Applied when taxes remain unpaid by the deadline.

✔ Failure to Deposit Penalty

Relevant to employers who do not deposit payroll taxes on time.

Under first-time abatement 2026, these penalties may no longer require taxpayers to call the IRS or file Form 843 to request relief.

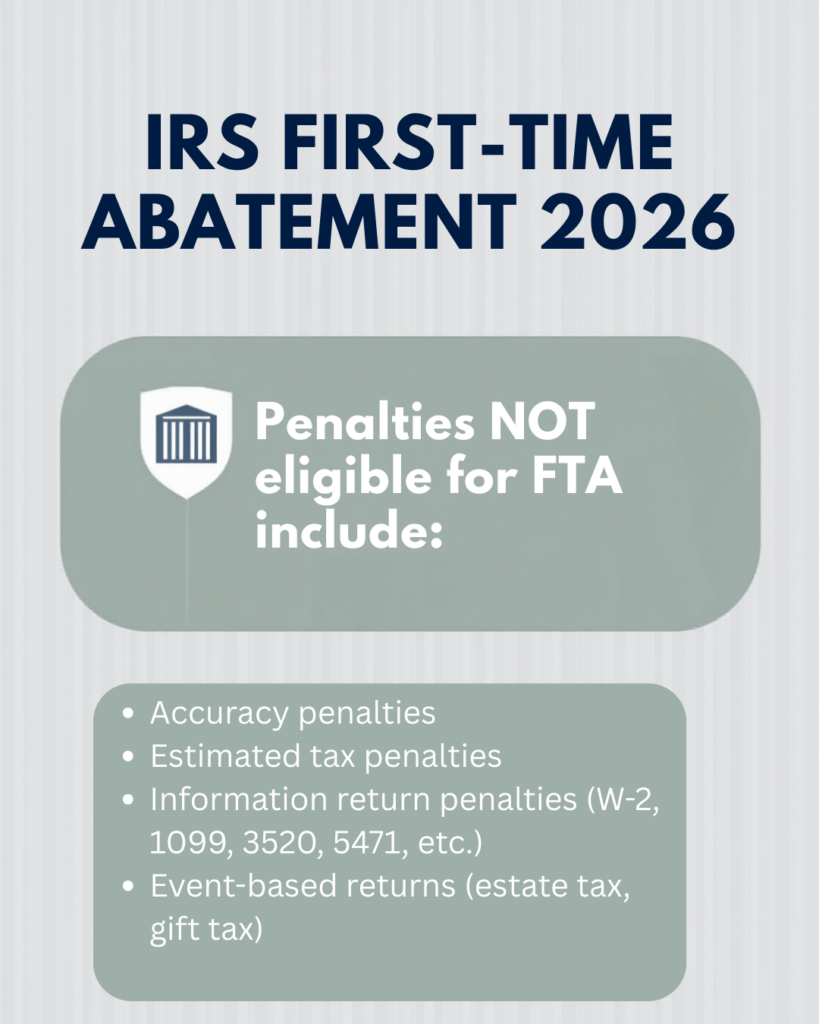

❌ Penalties NOT eligible for FTA include:

Accuracy penalties

Estimated tax penalties

Information return penalties (W-2, 1099, 3520, 5471, etc.)

Event-based returns (estate tax, gift tax)

🧾 Who Qualifies for First-Time Abatement 2026?

To qualify for first-time abatement 2026, taxpayers must meet existing FTA rules. These requirements remain unchanged.

🔹 1. Eligible Return Types

FTA applies only to:

Individual: Form 1040 series

Business: Form 1120, Form 1065

Payroll: Form 940, 941, 944, 945

Not eligible under first-time abatement 2026: Form 990 series, gift tax returns, estate tax returns, international forms.

🔹 2. Clean Compliance History

Taxpayer must have:

No disqualifying penalties in the three years prior to the penalty year

Estimated tax penalties do NOT disqualify

For joint returns: BOTH spouses must meet the criteria

For payroll taxes: must not have more than three prior Failure to Deposit waivers

Even under first-time abatement 2026, the IRS will evaluate compliance history before applying automatic relief.

🔹 3. Filing Compliance

All required tax returns for the previous three years must be filed.

This rule is unchanged under the first-time abatement 2026 automatic system.

🔹 4. Good Standing on Balances

Taxpayers must be current with IRS agreements or payment plans.

Automatic FTA in first-time abatement 2026 will be blocked if a taxpayer is not in good standing.

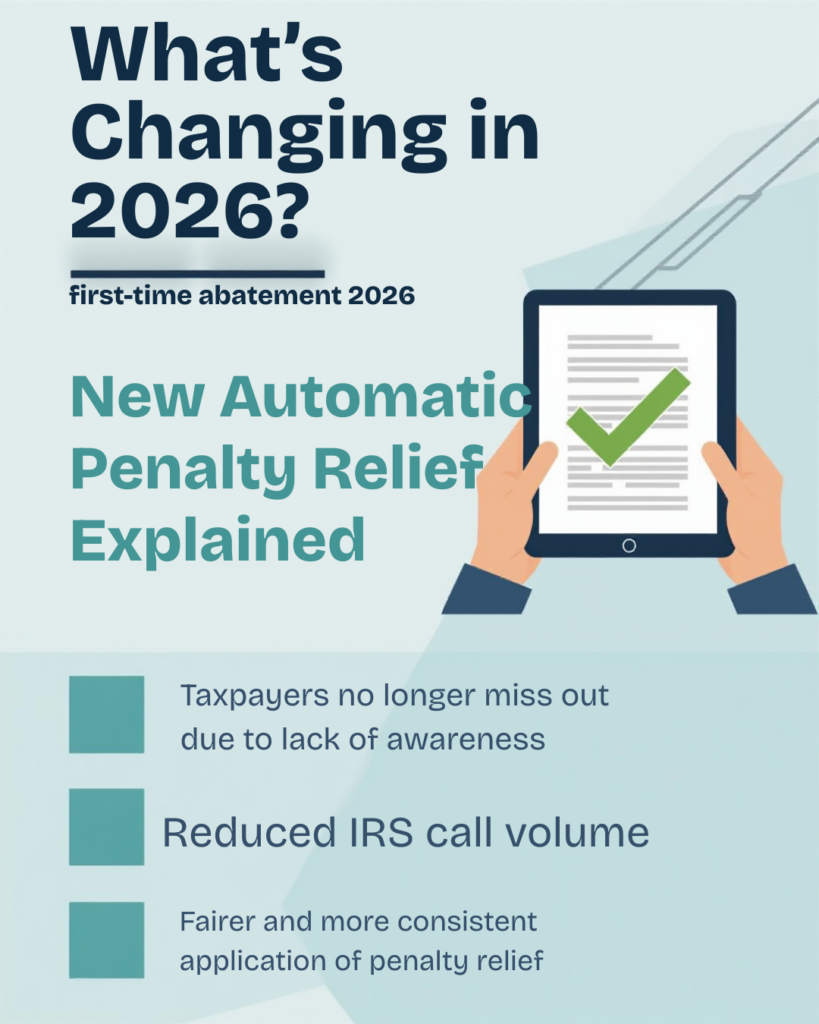

🚀 What’s Changing in 2026?

Currently, taxpayers must manually request FTA by:

Calling the IRS

Writing a letter

Filing Form 843

Beginning in first-time abatement 2026, the IRS will automatically issue the waiver when all criteria are met.

This modernization comes after years of recommendations from:

Treasury Inspector General for Tax Administration (TIGTA)

National Taxpayer Advocate (NTA)

Industry tax associations

In November 2025, Erin Collins (NTA) confirmed that the IRS will be implementing the automatic first-time abatement 2026 capability.

🌟 Benefits of Automatic FTA:

Taxpayers no longer miss out due to lack of awareness

Reduced IRS call volume

Faster processing

Fairer and more consistent application of penalty relief

🧠 Why First-Time Abatement 2026 Matters

Millions of taxpayers qualify for FTA every year, but only a small percentage receive the waiver. Reasons include:

Not knowing the program existed

Difficulty contacting the IRS

Confusion about eligibility

Filing delays that complicate penalty removal

With first-time abatement 2026, the IRS aims to eliminate these barriers.

This change especially benefits:

First-time filers

Taxpayers facing temporary financial hardship

Small businesses with payroll deposit issues

Tax professionals who handle high call volumes during tax season

🛠️ Action Steps for Tax Professionals

Even though first-time abatement 2026 becomes automatic, tax professionals must remain vigilant.

🔍 1. Review Client Accounts for Missed Past FTA Opportunities

Clients may still qualify for relief for earlier years (before 2026). Tax pros can:

Obtain Form 2848

Call the IRS Practitioner Priority Service

File Form 843 when appropriate

📅 2. Watch for IRS Implementation Guidance

Key details will be published as the IRS finalizes:

System automation rules

Exception-handling processes

How to address cases where automatic FTA is not applied

Employer deposit penalty workflows

📝 3. Ensure Clients Maintain Filing Compliance

Missing returns automatically disqualify taxpayers from first-time abatement 2026.

Encourage clients to catch up before penalties hit.

The IRS provided administrative penalty waivers for:

2019–2020 late filing

2020–2021 failure to pay

These do NOT disqualify taxpayers from first-time abatement 2026, but IRS coding inconsistencies may require manual intervention.

🔚 Final Thoughts

The introduction of first-time abatement 2026 represents a major IRS modernization that brings more fairness and access to penalty relief. Millions of taxpayers will benefit from automatic evaluations rather than needing to request relief through complex processes.

Tax professionals should stay informed, monitor IRS publications, and proactively review client accounts to ensure no qualified taxpayer misses out on penalty relief.

📞 Need Help Navigating IRS Penalties or Compliance?

Veritas Accounting Services is here to support you.

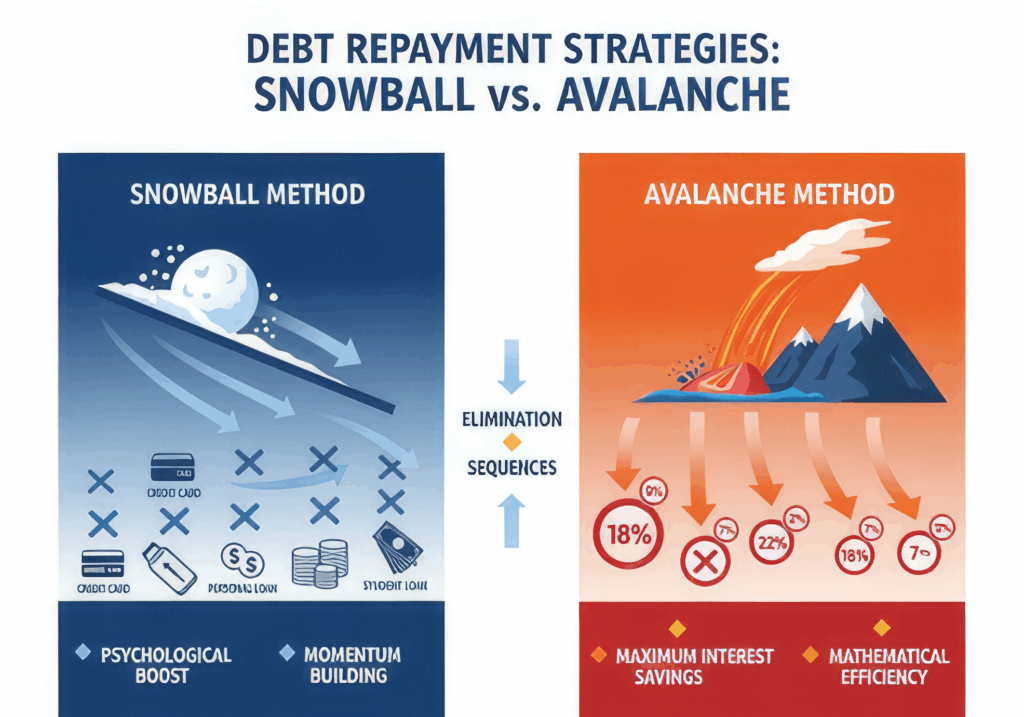

If you’re drowning in credit cards, loans, or medical bills, you’re not alone—but you can Crush Your Debt Faster with a clear plan. The problem for most people isn’t a lack of effort; it’s a lack of strategy. You pay a little here, a little there, and it feels like nothing ever changes.

Two proven methods can turn that around:

The Debt Snowball Method

The Debt Avalanche Method

Both are powerful debt repayment strategies that help you stay focused and make real progress. In this guide, you’ll learn how each method works, who they’re best for, and how to choose the one that helps you Crush Your Debt Faster without burning out.

What Is the Debt Snowball Method?

The Debt Snowball Method is built around small, fast wins. Instead of worrying about interest rates, you focus on paying off your smallest debts first and create momentum.

How the Snowball Method Works

List all your debts from smallest balance to largest.

Pay the minimum on every debt.

Put all extra money toward the smallest debt.

Once that debt is gone, “snowball” its payment into the next smallest debt.

Repeat until every debt is paid off.

Even though this method isn’t always mathematically perfect, it helps you Crush Your Debt Faster because it keeps you emotionally engaged.

Why the Snowball Method Works

You eliminate entire balances quickly.

Each win builds motivation and confidence.

The plan is simple, so you’re less likely to quit.

Best for: people who feel overwhelmed, emotional spenders, and anyone who needs quick proof that their efforts are working.

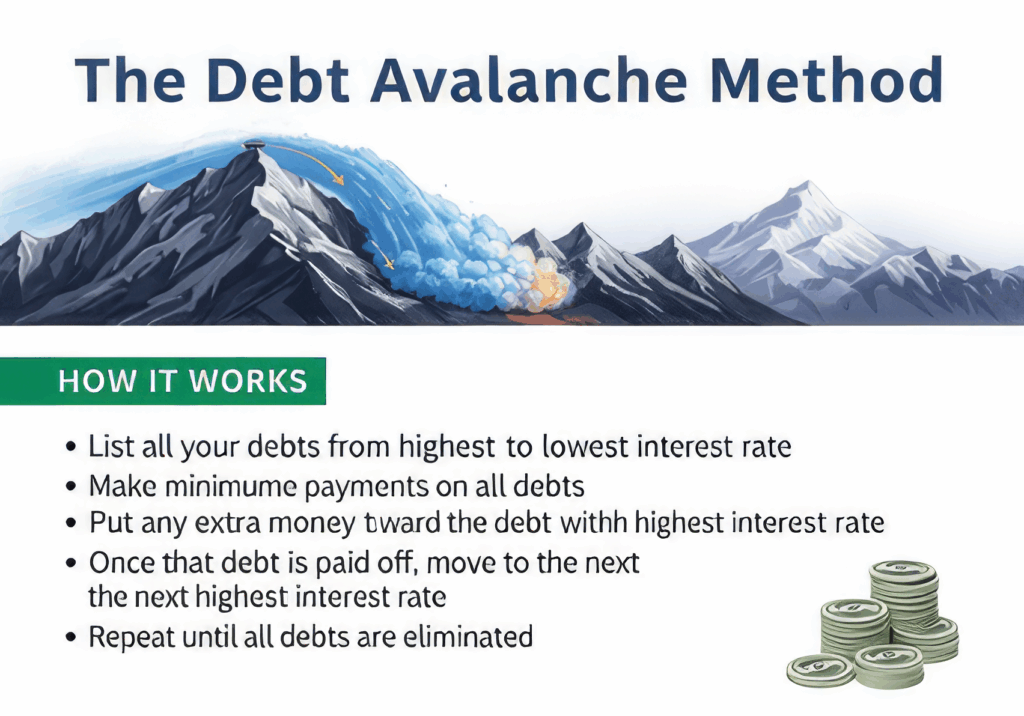

What Is the Debt Avalanche Method?

The Debt Avalanche Method is focused on saving the most money in interest and often paying off everything in less time overall. Instead of looking at balance size, you look at interest rates.

How the Avalanche Method Works

List all your debts from highest interest rate to lowest.

Pay the minimum on all debts.

Put all extra money toward the highest-interest debt.

Once it’s paid off, move to the next highest rate.

Continue until you’re completely debt-free.

This approach helps you Crush Your Debt Faster from a financial perspective, even if early progress is less visible.

Why the Avalanche Method Works

You pay less total interest.

You usually finish your debt-free journey sooner.

It’s especially powerful for high-interest credit cards.

Best for: disciplined people who like numbers, want to minimize interest, and don’t need immediate emotional wins.

Snowball vs. Avalanche: Key Differences

Use this in a Table block in WordPress:

Feature

Debt Snowball

Debt Avalanche

Main Focus

Smallest balance first

Highest interest rate first

Motivation

Fast emotional wins

Long-term savings

Interest Saved

Less

More

Speed Overall

Sometimes slower

Often faster

Complexity

Very simple

Requires tracking rates

Best For

Motivation & momentum

Efficiency & savings

In simple terms:

Snowball is emotion-first, math-second.

Avalanche is math-first, emotion-second.

To Crush Your Debt Faster, you need the one that aligns with how you think and behave.

Which Strategy Will Help You Crush Your Debt Faster?

The “best” strategy is the one you actually stick with.

Ask yourself:

Do I lose motivation when progress is slow?

Do I care more about paying less interest or feeling progress sooner?

Do I like simple, no-math plans or detailed, optimized ones?

Choose the Snowball Method If…

You’ve started and stopped debt payoff plans before.

You feel better when you see entire accounts hit zero.

You want an easy way to Crush Your Debt Faster through motivation.

Choose the Avalanche Method If…

You’re patient and disciplined.

You want to save the most money on interest.

You’re okay waiting longer for the first “big win.”

There’s no wrong answer. The real mistake is staying stuck and using no system at all.

Can You Combine Both Strategies?

Absolutely. You don’t have to pick one and stay with it forever. A hybrid approach can help you Crush Your Debt Faster while balancing emotion and efficiency.

Start with a mini Snowball: Pay off one or two tiny debts first to create quick momentum.

Switch to Avalanche: Once you feel focused and confident, reorder your remaining debts by interest rate and attack the highest one.

Reset when needed: If you feel stuck again, temporarily use the Snowball on a small balance to regain motivation.

This blended method gives you the emotional wins of Snowball and the interest savings of Avalanche.

Real-Life Example: Which Method Wins?

Meet Sam. Sam has these debts:

Debt Type

Balance

Interest Rate

Credit Card A

$1,500

22%

Credit Card B

$800

18%

Personal Loan

$3,000

10%

Medical Bill

$500

0%

Sam can put $450 per month toward debt.

With the Debt Snowball

Order from smallest balance:

Medical Bill – $500

Credit Card B – $800

Credit Card A – $1,500

Personal Loan – $3,000

Sam wipes out the medical bill in just over one month, then Credit Card B a few months later. These fast wins make Sam feel powerful and in control—and that feeling helps Sam Crush Debt Faster because the plan doesn’t get abandoned.

With the Debt Avalanche

Order by highest interest rate:

Credit Card A – 22%

Credit Card B – 18%

Personal Loan – 10%

Medical Bill – 0%

Sam needs more time before one entire account disappears, but pays much less interest overall and finishes the total payoff sooner than with Snowball.

Takeaway:

Snowball helps Sam stay emotionally committed.

Avalanche helps Sam save more and mathematically Crush Debt Faster.

You choose which “faster” matters more: faster emotionally, or faster financially.

Final Thoughts: Start Crushing Your Debt Today

You don’t need perfect timing, a big income, or a miracle. You just need a plan you’ll actually follow.

Use Debt Snowball if motivation is your biggest challenge.

Use Debt Avalanche if interest savings and efficiency matter most.

Use a hybrid strategy if you want both.

Most importantly, take action. The sooner you start, the sooner you’ll Crush Your Debt Faster and free up your income for saving, investing, and building the life you actually want.

Pick your strategy today and start your debt-free journey.

📞 Ready to Finally Crush Your Debt Faster and Take Control of Your Financial Future?

If you need expert guidance on budgeting, debt repayment planning, or complete financial management, Veritas Accounting Services is here to support you every step of the way.

Contact Veritas Accounting Services:

📧 Email:hello@veritasaccountingservices.com 📞 Phone: +1 (678) 723-6003 | +91 97255 52243 🏢 US Office: 8735 Dunwoody Place – 4549, Atlanta, GA 🏢 India Office: C-305, The Imperial Heights, 150ft Ring Road, Rajkot

We proudly serve clients across the US, UK, UAE, Singapore, Ireland, and Malaysia, offering personalized bookkeeping, debt planning, tax filing, and CFO-level financial

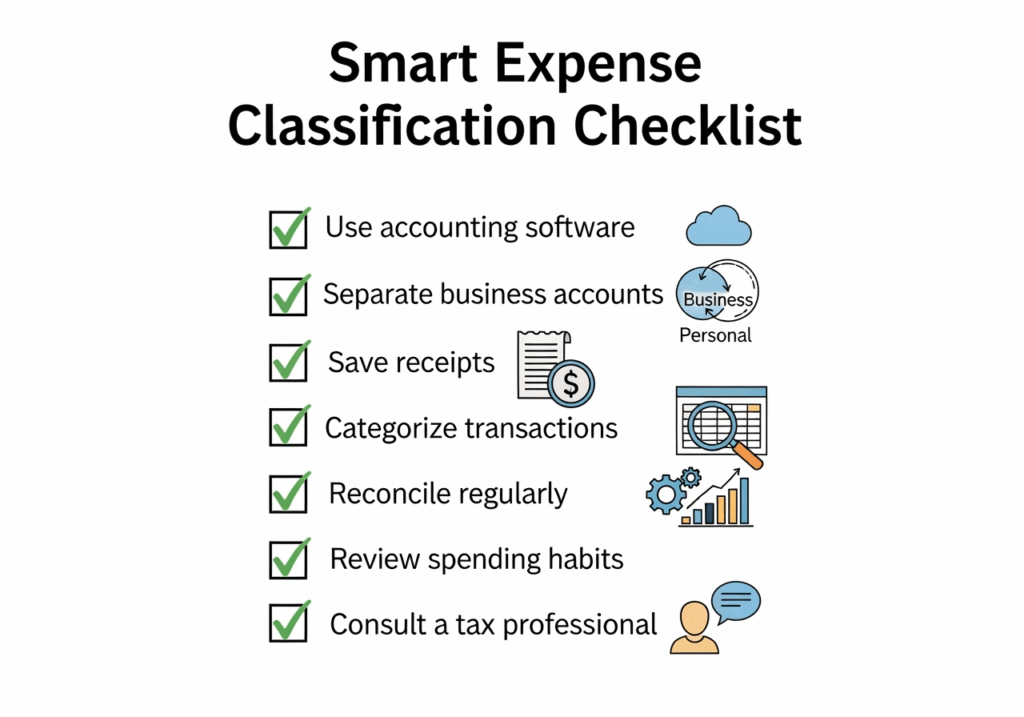

To correctly classify business expenses is foundational to solid bookkeeping and financial decision-making. Yet, many business owners and freelancers trip up in this area—leading to lost deductions, inaccurate reporting, and extra stress during tax season. Let’s change that!

In this guide, you’ll learn:

What counts as a business expense (with real examples)

Why classification matters so much

Common and costly mistakes (and how to sidestep them)

Pro tips for flawless, stress-free accounting

Answers to the most frequent questions

A printable, actionable checklist to keep you organized

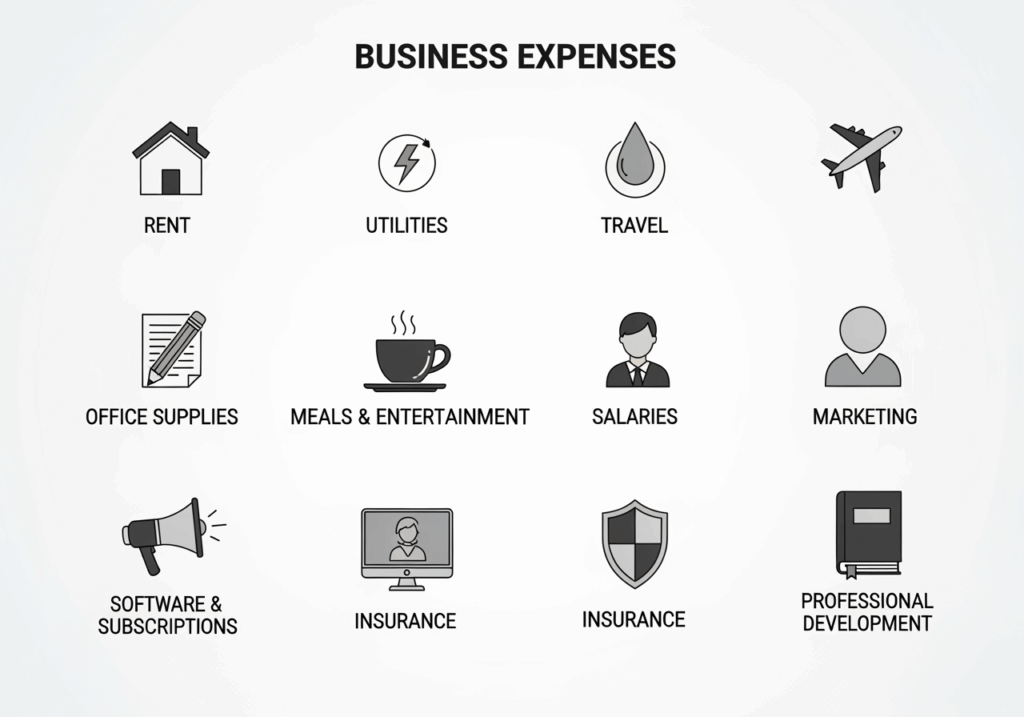

What Counts as a Business Expense? (With Real-World Examples)

Business expenses are the ordinary and necessary costs of running your company. But what does that mean in practice?

Here are popular categories and real examples for each:

Travel: Airfare, mileage, taxis/rideshares, hotels, meals on work trips

Meals and Entertainment: Taking clients out for lunch, company event catering (subject to strict limits)

Salaries and Wages: Staff pay, bonuses, payroll taxes

Professional Services: Legal, accounting, consulting fees

Insurance: Business liability, workers comp, property insurance

Marketing and Advertising: Website fees, online ads, print materials

Depreciation: Gradual cost deduction for major purchases like machinery or vehicles

Pro Tip: If you’re ever unsure if an expense qualifies, ask yourself—”Is this cost directly related to earning business income?” If the answer’s yes, it likely qualifies.

Why Correct Classification Matters

Classifying business expenses correctly doesn’t just make life easier for your accountant. Here’s why it truly matters:

Maximize Tax Deductions: Many allowable business expenses directly reduce taxable income, meaning less money owed to the government (and more in your pocket).

Financial Insights: Accurate expense tracking reveals which parts of your business are costing the most—and where you can cut back.

Audit Readiness: Clean, careful records make audits quick and painless if you ever get selected.

Credibility with Investors/Banks: Lenders or investors like to see well-organized, easy-to-explain financials.

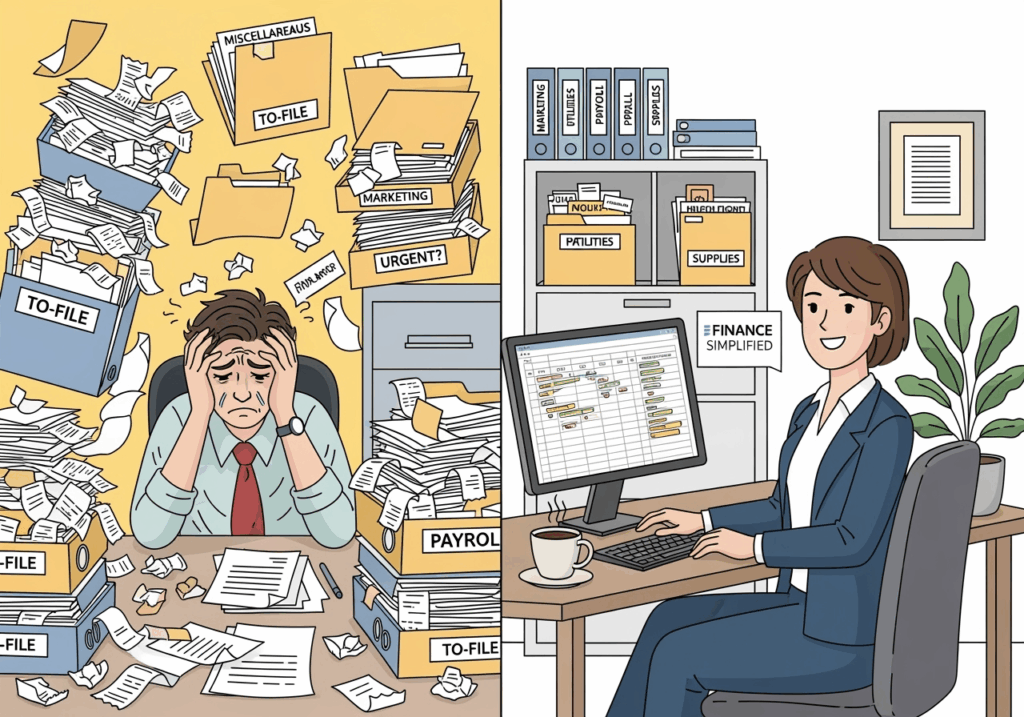

Common Expense Classification Mistakes (With Solutions)

Let’s explore mistakes in detail, with real-world fixes:

1. Mixing Personal and Business Finances

Example: You grab a coffee using your business card, but it’s not a work-related purchase.

Fix: Set up separate bank accounts and credit cards. If you make a mistake, note the transaction as an owner draw or personal reimbursement.

2. Misclassifying Expenses

Example: Coding a business lunch with a client as “Office Supplies,” or putting software under “Equipment.”

Fix: Use accounting software with preset categories. Review transactions monthly for accuracy.

3. Missing Out on Small Deductions

Example: Ignoring small subscriptions or petty cash expenses; assuming they’re “too minor.”

Fix: Track every expense, even $2 ones. Digital tools make this frictionless; use expense scanning apps or file receipts in Google Drive.

4. Lost or Incomplete Documentation

Example: Tossing receipts or not collecting itemized bills.

Fix: Go digital—scan with your phone, save PDFs, or use receipt-management platforms like Expensify or Dext.

5. Over- or Underclaiming Deductions

Example: Claiming the full cost of your personal mobile as a business expense, or not claiming your home office at all.

Fix: Claim only the business-use portion. For mixed-use items (like utilities at home), use a percentage based on actual use.

6. Not Updating Categories as Business Grows

Example: Sticking to overly simple categories (“other expenses,” “miscellaneous”) as your business expands.

Use cloud-based software like QuickBooks, Xero, Zoho, or Wave, which auto-categorizes common expenses (and syncs with your bank!).

Set up rules so recurring transactions (like your internet bill) are always coded to the right category.

Be Consistent

Define your categories clearly and always use them the same way.

If you have a team, create a simple one-pager explaining what belongs where.

Schedule a Monthly “Money Date”

Take 30 minutes at the end of each month to review your transactions, match receipts, and fix any uncategorized expenses.

Educate the Whole Team

Train employees on proper receipt submission and expense types.

Use an approval system for purchases, so random expenses don’t slip through.

Document Your Expense Policy

Put your rules in writing! This helps if you ever hire a bookkeeper or get audited.

Ask for Professional Help

An accountant or bookkeeper can review your setup, optimize your categories, and ensure you’re maximizing deductions.

FAQs: Business Expense Classification

Classify Business Expenses

Q: Can I deduct all meals with clients? A: Not always. Many tax authorities cap meal deductions at 50%, and receipts/documentation are required. Casual or non-business meals don’t qualify.

Q: What if I work from a home office—how do I classify those expenses? A: Calculate the percentage of your home used for business (by area or time) and claim that portion of rent, utilities, and insurance as a business expense.

Q: Is my car a business expense if I also use it personally? A: Only claim the percentage of car expenses related to business miles. Use a mileage log or mileage-tracking app.

Q: What if I make a mistake? A: Adjust the transaction and document the change. Most software allows easy recategorization.

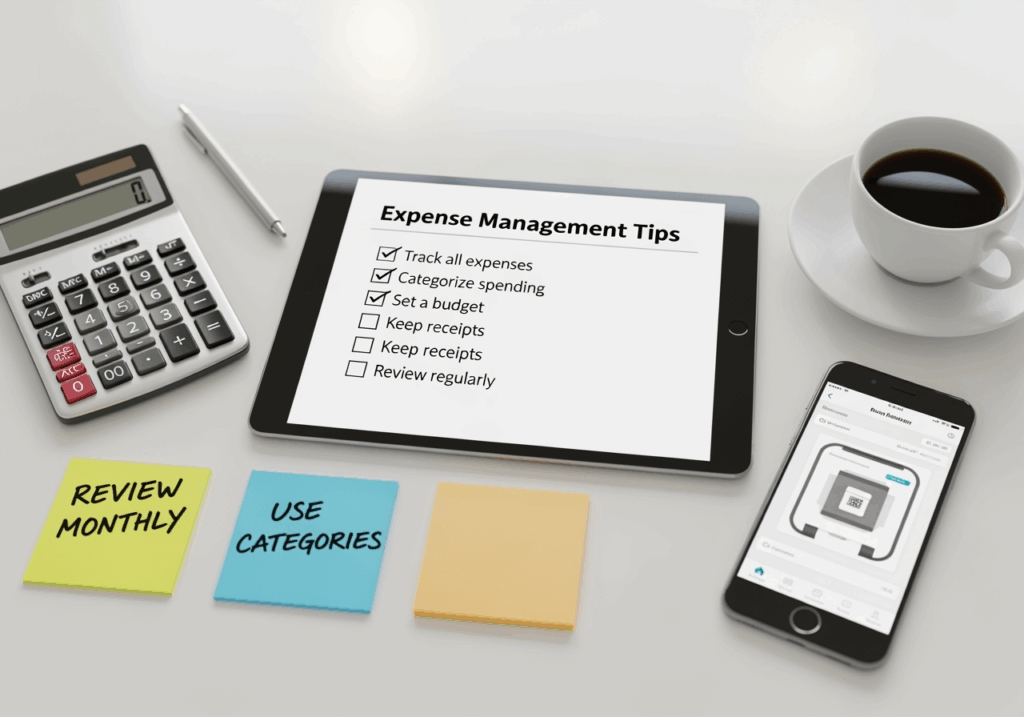

Actionable Checklist for Smarter Expense Classification

Feel free to print or bookmark this!

Setup

✅ Open designated business bank accounts ✅ Choose accounting or expense tracking software ✅ Create a clear chart of accounts (categories)

Ongoing Process

✅ Always use the business account for business purchases ✅ Save digital or physical receipts for all transactions ✅ Enter all expenses into your accounting system ✅ Review uncategorized/“miscellaneous” expenses each month ✅ Match bank and credit card transactions to entries ✅ Update categories as business grows

At Year-End

✅ Reconcile all accounts ✅ Check for missed deductions ✅ Provide clear records to your accountant ✅ Adjust categories for the new year’s goals

Final Thoughts

Getting business expense classification right isn’t just about tax season—it’s about taking charge of your business finances and making smarter decisions year-round. The more consistent (and organized) you are, the less likely you are to miss deductions, make costly errors, or panic during audits.

By using technology, documenting your process, and reviewing transactions regularly, you’ll build a system that works for you—not against you.

Need help setting up or reviewing your expense categories? Drop your questions in the comments or connect with our bookkeeping pros for a no-obligation consultation. Your future self—and your bottom line—will thank you!

classify business expenses classify business expenses classify business expenses classify business expenses classify business expenses classify business expenses classify business expenses classify business expenses classify business expenses classify business expenses classify business expenses classify business expenses classify business expenses classify business expenses classify business expenses classify business expenses classify business expenses classify business expenses

In an increasingly volatile business environment, the ability to maintain operations during unexpected disruptions has become a critical competitive advantage. With over a decade of professional excellence and 1000+ completed projects across 6+ countries, Veritas Accounting has guided businesses through numerous crises, from economic downturns to global pandemics. Our experience has shown that businesses with robust financial continuity plans are not only more likely to survive disruptions but often emerge stronger than their competitors.

Understanding Business Continuity in the Financial Context

Business continuity planning extends far beyond operational procedures—it requires comprehensive financial strategies that ensure your business can weather any storm. Financial uncertainty and compliance issues can quickly escalate during disruptions, making timely and strategic financial management absolutely critical for survival.

At Veritas, we’ve observed that businesses operating across multiple countries face unique continuity challenges. Currency fluctuations, varying regulatory responses, and different market conditions during crises require sophisticated financial planning that accounts for global complexities. Our presence in the USA, UK, Australia, and other markets provides us with firsthand experience in managing these multi-jurisdictional challenges.

The Financial Foundation of Business Continuity

Emergency Cash Flow Management The cornerstone of any business continuity plan is maintaining adequate cash flow during disruptions. This goes beyond simply having cash reserves—it requires understanding your cash conversion cycle, identifying potential cash flow bottlenecks, and creating multiple scenarios for different disruption levels.

Our Virtual CFO services help businesses develop comprehensive cash flow forecasting models that account for various disruption scenarios. Using our expertise with QuickBooks, Xero, Wave, and Zoho Books, we create real-time cash flow monitoring systems that provide early warning signals when financial stress begins to emerge.

Strategic Reserve Management While traditional advice suggests maintaining 3-6 months of operating expenses in reserves, our experience shows that businesses need more sophisticated reserve strategies. This includes diversifying reserve locations, maintaining multi-currency reserves for international operations, and establishing credit facilities before they’re needed.

We help businesses optimize their reserve strategies by analyzing historical cash flow patterns, identifying seasonal variations, and stress-testing financial models against various disruption scenarios. This approach ensures reserves are adequate without tying up excessive capital during normal operations.

Crisis-Proofing Your Financial Systems

Technology Resilience and Remote Access The shift to remote work during recent global disruptions highlighted the critical importance of cloud-based financial systems. Businesses with outdated, location-dependent accounting systems faced significant operational challenges when physical offices became inaccessible.

Our seamless integration expertise with top accounting software ensures businesses can maintain full financial operations regardless of physical location. Cloud-based solutions like QuickBooks Online and Xero provide the accessibility and security needed for continuous financial management during disruptions.

Financial Process Automation Manual financial processes become major vulnerabilities during disruptions when key personnel may be unavailable. Automation not only improves efficiency during normal operations but provides critical continuity capabilities during crises.

We help businesses identify and automate key financial processes, from invoice generation to payment processing, ensuring essential financial functions continue even when staffing is disrupted. This automation also reduces the risk of errors during high-stress periods when manual oversight may be limited.

Multi-Country Continuity Strategies

Regulatory Compliance During Disruptions Businesses operating in multiple countries must navigate varying regulatory responses during crises. Some jurisdictions may offer tax relief or compliance extensions, while others maintain strict deadlines regardless of circumstances.

Our global expertise across 6+ countries enables us to help businesses understand and leverage available regulatory relief while maintaining compliance where flexibility isn’t available. This includes managing tax obligations, employment law requirements, and financial reporting standards across different jurisdictions.

Currency Risk Management in Crisis Situations Economic disruptions often trigger significant currency volatility, which can severely impact businesses with international operations. Companies that don’t actively manage currency risk may find their financial position deteriorating rapidly during crises.

We provide comprehensive currency risk management strategies that include hedging techniques, natural hedging through operational adjustments, and scenario planning for different currency movement patterns. These strategies help businesses maintain financial stability even when currency markets become highly volatile.

Stress Testing and Scenario Planning

Financial Stress Testing Methodologies Effective business continuity planning requires understanding how your business would perform under various stress scenarios. This goes beyond simple “what if” discussions to include quantitative analysis of different disruption levels and durations.

Our ratio analysis expertise helps businesses identify key financial vulnerabilities and stress test their business models against various scenarios. This includes analyzing debt service capabilities, working capital requirements, and profitability thresholds under different operating conditions.

Dynamic Scenario Planning Static business continuity plans quickly become obsolete as conditions change. Effective continuity planning requires dynamic scenario modeling that can be updated as new information becomes available during a crisis.

We help businesses develop flexible scenario planning frameworks that can be quickly adjusted as disruptions evolve. This includes creating decision trees for different response options and establishing trigger points for implementing various contingency measures.

Financial Communication During Crises

Stakeholder Communication Strategies During disruptions, clear and timely communication with financial stakeholders becomes critical. This includes investors, lenders, suppliers, and customers who all need to understand how the business is managing through the crisis.

Our financial reporting expertise helps businesses develop crisis communication protocols that provide transparency while maintaining confidence. This includes preparing standardized reports that can be quickly updated and distributed to different stakeholder groups.

Investor Relations During Disruptions Businesses with external investors face additional communication challenges during crises. Investors need regular updates on financial performance, cash flow projections, and management actions being taken to address the disruption.

We help businesses develop investor communication frameworks that provide appropriate transparency while managing expectations. This includes preparing financial projections that account for uncertainty and clearly communicating the assumptions underlying these projections.

Post-Crisis Financial Recovery Planning Business continuity planning must extend beyond simply surviving the crisis to include strategies for recovery and growth. Businesses that plan for recovery during the crisis often emerge in stronger competitive positions.

Our strategic financial planning services help businesses identify recovery opportunities and develop financial strategies to capitalize on them. This includes assessing acquisition opportunities, planning for market share gains, and optimizing capital structure for post-crisis growth.

Building Resilience for Future Disruptions Each crisis provides valuable lessons that can be incorporated into improved continuity planning. Businesses that learn from each disruption become increasingly resilient over time.

We help businesses conduct post-crisis financial reviews that identify areas for improvement in their continuity planning. This includes analyzing what worked well, what could be improved, and how financial systems and processes can be strengthened for future disruptions.

Technology and Innovation in Continuity Planning

AI and Predictive Analytics Advanced technologies are increasingly being used to improve business continuity planning. AI-powered analytics can identify early warning signals and predict potential disruptions before they fully materialize.

We help businesses leverage technology to enhance their continuity planning capabilities. This includes implementing predictive analytics for cash flow forecasting and using AI to identify potential risk factors that might not be apparent through traditional analysis.

Blockchain and Financial Security Emerging technologies like blockchain offer new possibilities for maintaining financial security and continuity during disruptions. These technologies can provide enhanced security and transparency for financial transactions even when traditional systems are compromised.

Industry-Specific Continuity Considerations

Manufacturing and Supply Chain Finance Manufacturing businesses face unique continuity challenges related to inventory management, supplier financing, and production scheduling. Financial continuity planning must account for these operational complexities.

Professional Services Continuity Professional services firms must balance client service continuity with financial management during disruptions. This often requires flexible billing arrangements and modified service delivery models.

Technology and Software Companies Tech companies may face different continuity challenges related to subscription revenue models, development costs, and rapid scaling requirements during and after disruptions.

Measuring Continuity Plan Effectiveness

Key Performance Indicators for Continuity Effective continuity planning requires measurable objectives and regular assessment of plan effectiveness. This includes financial metrics like cash flow stability, operational metrics like service delivery continuity, and strategic metrics like market position maintenance.

Regular Plan Testing and Updates Business continuity plans must be regularly tested and updated to remain effective. This includes conducting financial stress tests, reviewing scenario assumptions, and updating response procedures based on changing business conditions.

The Veritas Advantage in Continuity Planning

Our decade of experience with 1000+ successful projects provides unique insights into what works in business continuity planning. We’ve helped businesses navigate various types of disruptions, from economic downturns to regulatory changes to global pandemics.

Our global presence across multiple countries gives us firsthand experience in managing continuity challenges across different regulatory environments and market conditions. This experience enables us to help businesses develop truly comprehensive continuity strategies that account for global complexities.

Implementation Framework

Phase 1: Risk Assessment and Gap Analysis We begin by conducting comprehensive risk assessments that identify potential disruption sources and evaluate current continuity preparedness. This includes analyzing financial vulnerabilities, operational dependencies, and regulatory requirements.

Phase 2: Strategy Development Based on the risk assessment, we develop customized continuity strategies that address identified vulnerabilities while maintaining operational efficiency during normal conditions.

Phase 3: Implementation and Testing We provide hands-on support during strategy implementation and help businesses conduct regular testing to ensure plans remain effective.

Phase 4: Ongoing Monitoring and Improvement Continuity planning is an ongoing process that requires regular review and updates. We provide continuous monitoring and improvement services to ensure plans evolve with changing business conditions.

Conclusion: Building Unshakeable Financial Resilience

In today’s uncertain business environment, robust financial continuity planning isn’t optional—it’s essential for long-term success. Businesses that invest in comprehensive continuity strategies not only survive disruptions but often emerge stronger and more competitive.

At Veritas Accounting, we combine global expertise with local market knowledge to help businesses build unshakeable financial resilience. Our comprehensive approach addresses all aspects of financial continuity, from emergency cash flow management to post-crisis recovery planning.

Don’t wait for the next disruption to test your business’s resilience. Contact Veritas Accounting today to develop a comprehensive financial continuity plan that protects your business and positions it for long-term success.

Contact Veritas Accounting:

Headquarters: C-305, The Imperial Heights, 150ft Ring Road, Rajkot

US Office: 8735 Dunwoody Place – 4549, Atlanta, GA

Wondering why some startups grow effortlessly while others stall? It’s not luck—it’s smart start up accounting. After helping over 1,000 businesses across six countries, we know what separates thriving startups from the ones that burn out. Spoiler: it’s about having a solid financial plan and automated accounting systems from day one.

Let’s walk through practical, proven steps to help your business grow sustainably, profitably—and globally.

1. Build a Rock-Solid Financial Foundation

The Key to Smart Start up Accounting in 2025

You wouldn’t build a house without a foundation—same goes for your business finances.

Must-Do Basics (Start Now!)

Separate your personal and business accounts (this clears 70% of future headaches)

Set up a business checking account with online access

Use cloud-based accounting tools (QuickBooks or Xero are ideal for small business accounting)

Implement a clean invoicing system to streamline payment collection

Starter Tech Stack:

Use automated accounting systems to save time

Set up real-time financial dashboards for instant access to key metrics

Implement growth-ready financial tools that can scale with your business

2. Master Daily & Weekly Money Habits That Drive Growth

Daily Financial Habits:

The Two-Account System: One for income, one for expenses

15-minute daily finance check-in

Use receipt scanning apps (ditch paper clutter)

Automate data entry with bank feeds to accounting software

Weekly Financial Routine:

Monday: Review pending payments and client invoices

Friday: Reconcile accounts (30 minutes tops!)

Track profit margins and update cash flow forecasts