Each tax season, questions about refund timing surge—especially from taxpayers who rely on refundable credits like the Earned Income Tax Credit (EITC) and the Additional Child Tax Credit (ACTC). These refunds often represent a meaningful source of financial support, and delays can cause understandable concern.

For the 2026 filing season, the IRS has set clear expectations around when EITC and ACTC refunds will be released. While the rules themselves are not new, understanding the timing—and the reasons behind it—can help taxpayers plan better and reduce frustration. Knowing the three critical IRS dates makes all the difference.

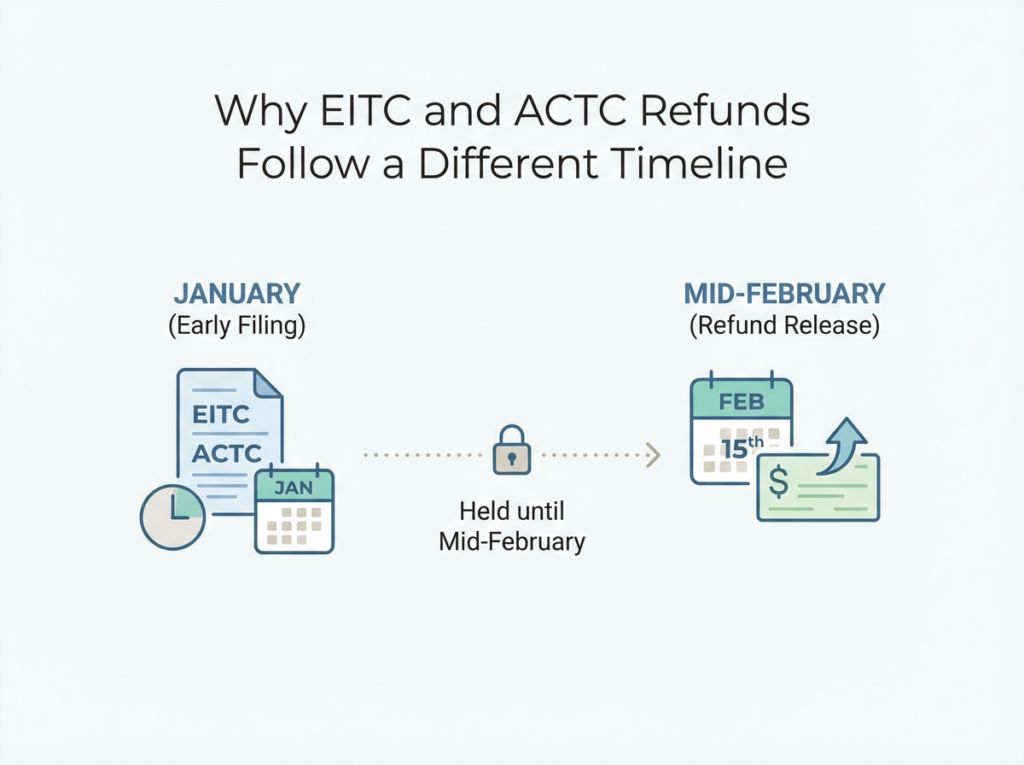

Why EITC and ACTC Refunds Follow a Different Timeline

Refunds that include the EITC or ACTC are subject to special rules under the Protecting Americans from Tax Hikes (PATH) Act. The PATH Act requires the IRS to hold these refunds until mid-February, regardless of how early the return is filed.

The goal is fraud prevention. By delaying refunds, the IRS has additional time to verify:

- Income reported on Forms W-2 and 1099

- Withholding amounts

- Dependent and qualifying child information

Although the delay can be frustrating, it has become a predictable and built-in part of the filing season.

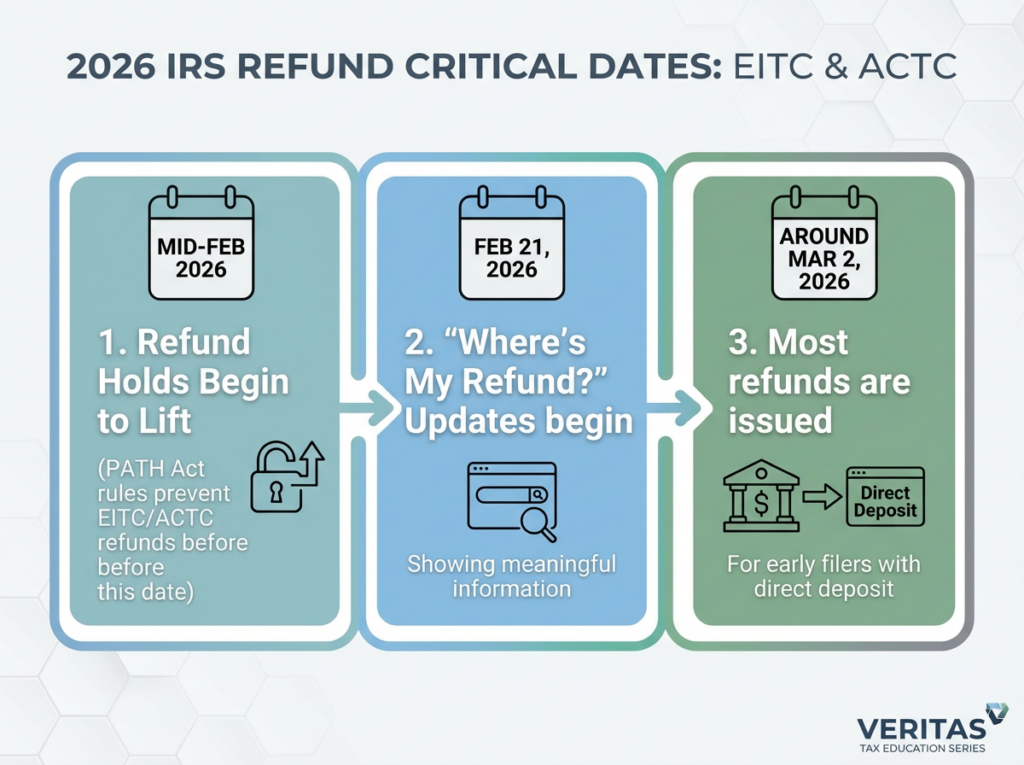

📅 The 3 Critical IRS Dates to Know for 2026

1. Mid-February 2026: Refund Holds Begin to Lift

Under the PATH Act, the IRS cannot issue refunds that include EITC or ACTC before mid-February. This rule applies even if:

- The return is filed on the first day of the season

- The return is accurate and complete

- Direct deposit is selected

This means taxpayers claiming these credits should not expect refunds in January or early February.

2. February 21, 2026: “Where’s My Refund?” Updates

By around February 21, 2026, the IRS expects its “Where’s My Refund?” tool to begin showing meaningful updates for most EITC and ACTC filers.

Once a return is approved, the tool will display a projected deposit date, which helps set realistic expectations. Tax professionals should encourage clients to rely on this tool rather than daily follow-ups.

3. Around March 2, 2026: Most Refunds Are Issued

The IRS has stated that most taxpayers who file early, claim EITC or ACTC, and choose direct deposit should receive refunds around March 2, 2026, assuming no issues with the return.

Some refunds may arrive slightly earlier or later depending on:

- Bank or debit card processing times

- Weekends or holidays

- Internal financial institution policies

Paper-filed returns and refunds issued by check will take longer.

How Refund Delivery Method Affects Timing

Choosing electronic filing with direct deposit remains the fastest and most reliable way to receive a refund. Taxpayers who opt for:

- Paper filing

- Mailed checks

should expect additional delays beyond the March 2 target window.

Even when the IRS releases funds, the final deposit timing depends on how quickly the taxpayer’s financial institution processes incoming payments.

Common Issues That Can Delay EITC or ACTC Refunds

Even with clear refund dates, some returns are delayed due to errors or mismatches. Common triggers include:

- Incorrect Social Security numbers for dependents

- Income that does not match Forms W-2 or 1099-NEC

- Errors on Schedule 8812 (Credits for Qualifying Children and Other Dependents)

- Missing or incomplete documentation

Because refundable credits are a major IRS enforcement focus, these returns receive additional scrutiny.

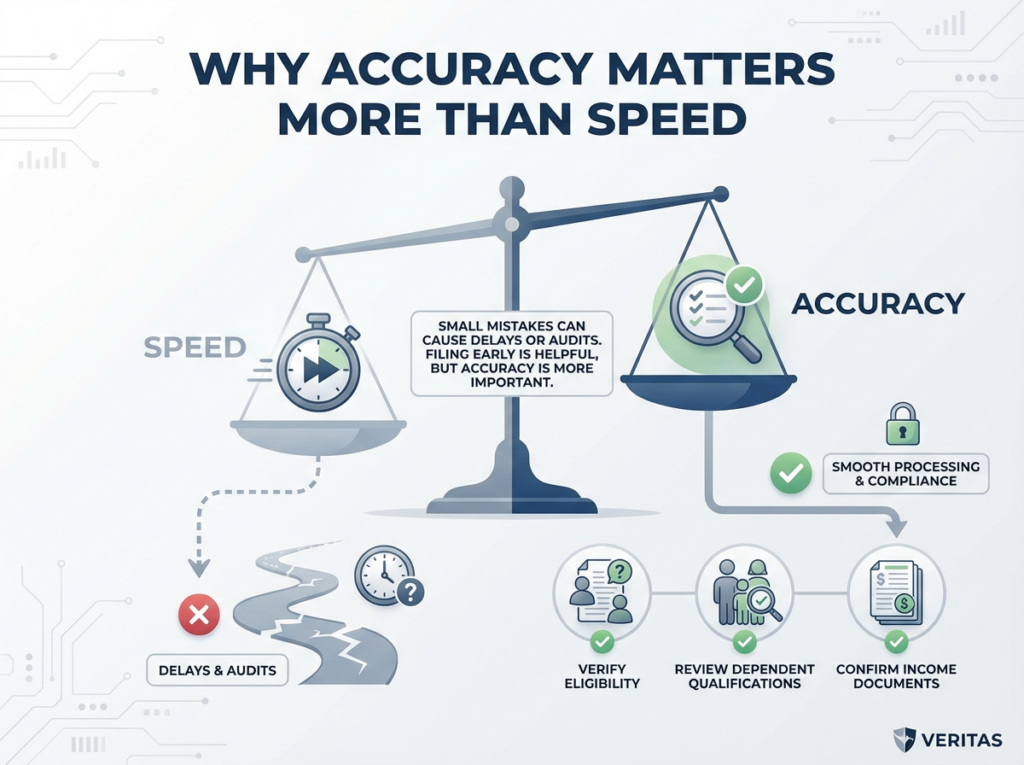

Why Accuracy Matters More Than Speed

Filing early is helpful, but accuracy matters more than speed when claiming EITC or ACTC. Tax professionals must meet strict due diligence requirements, and even small mistakes can cause processing delays or correspondence audits.

Verifying eligibility, reviewing dependent qualifications, and confirming income documents before filing helps prevent avoidable delays and protects both the taxpayer and the preparer.

Helping Clients Plan Around Refund Timing

For many families, EITC and ACTC refunds are used to:

- Pay down debt

- Catch up on household expenses

- Build emergency savings

Clear communication about refund timing helps clients plan responsibly and reduces pressure to use high-cost refund advance products.

Setting expectations early—especially explaining that March refunds are normal, not delayed—can significantly reduce anxiety during filing season.

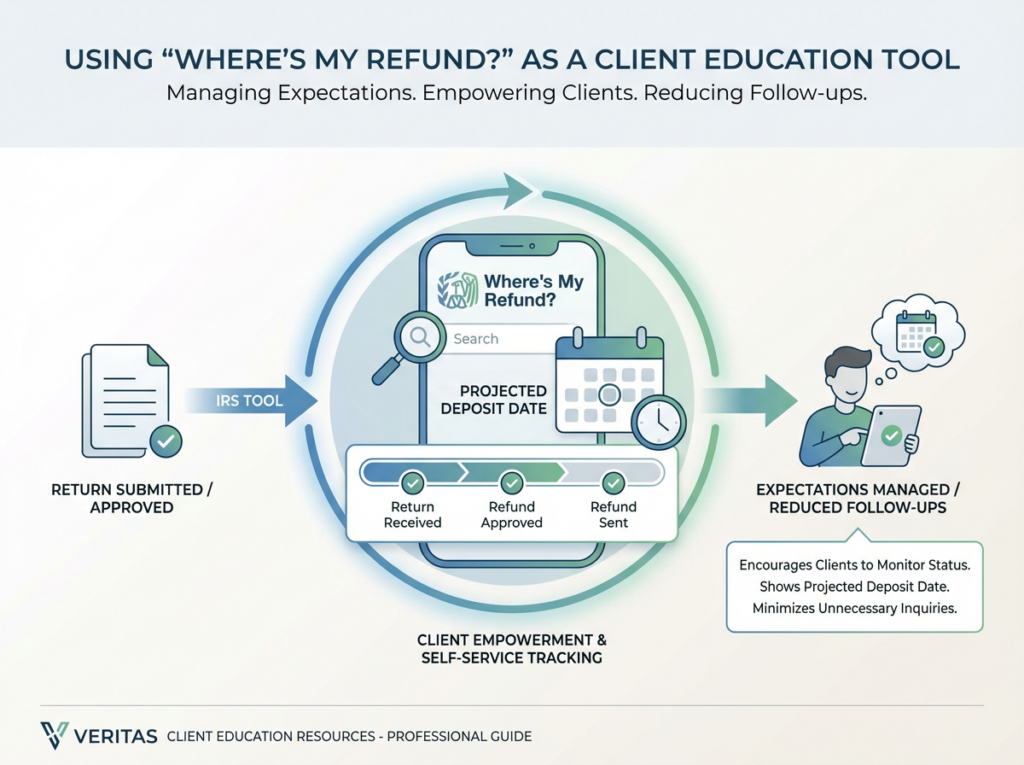

Using “Where’s My Refund?” as a Client Education Tool

The IRS “Where’s My Refund?” tool remains one of the most effective ways to manage expectations. Once a return shows as approved, the projected deposit date provides a reliable window for when funds should arrive.

Encouraging clients to use this tool empowers them and reduces unnecessary follow-ups.

A Timely Reminder for Tax Professionals

As refund-related questions increase, proactive education becomes a value-add. Explaining:

- The PATH Act delay

- The March 2 target date

- Common causes of delays

helps build trust and reinforces confidence in your practice.

For professionals looking to deepen their technical understanding, continued education on child-related credits remains essential—especially as enforcement around refundable credits continues to evolve.

Final Takeaway

Waiting for an EITC or ACTC refund can feel stressful, but the timeline for 2026 is clear and predictable. Understanding the three critical IRS dates—mid-February holds, late-February status updates, and early-March deposits—helps taxpayers plan with confidence.

With accurate filing, electronic submission, and direct deposit, most refunds will arrive right on schedule. And with the right guidance, what feels like a delay becomes simply part of a system designed to protect taxpayers and the integrity of the tax process.

GET IN TOUCH

Schedule a FREE Call

Connect on our Socials!